A stablecoin yield compromise?

Plus: markets are getting rates wrong again, and fund managers are gloomy

“People can foresee the future only when it coincides with their own wishes, and the most grossly obvious facts can be ignored when they are unwelcome.” – George Orwell ||

Hi everyone! I hope you’re all doing well. Yesterday was just crazy with the war narratives and this already feels like a very long week.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

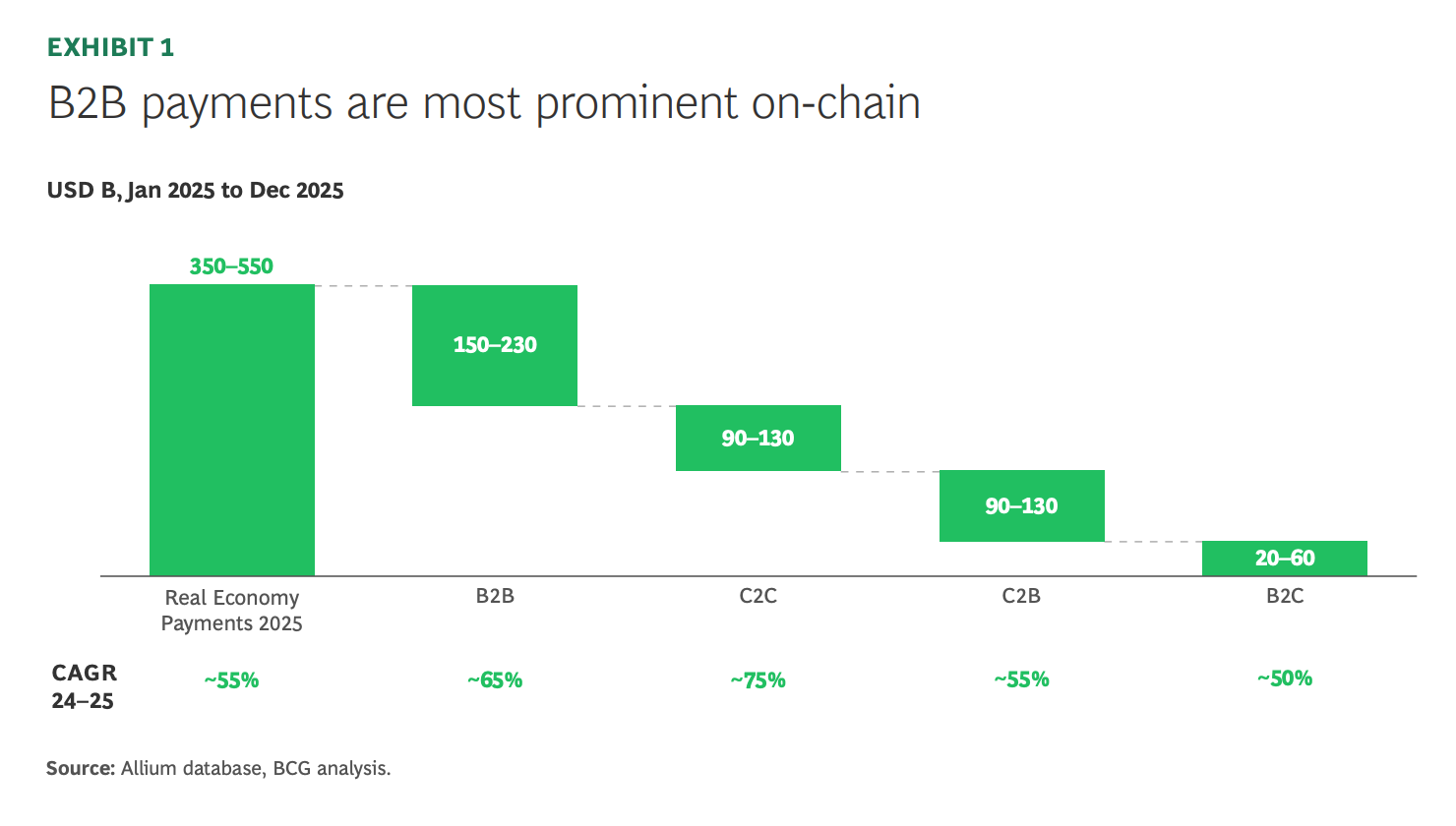

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Stablecoin yield compromise?

Macro: about those rate cuts

A new stablecoin dashboard

Global fund managers: not so cheerful anymore

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

✨ Use the discount code MACRO for 20% off!

Stablecoin yield compromise?

Details are leaking out regarding the stablecoin yield negotiations between banks and the crypto industry (via the always-on-point Eleanor Terrett, worth a follow), and so far it looks like a reasonable compromise.

To be clear, I think the bank lobbies are being outrageously regressive here, as well as self-defeating.

Dressing up a fear of competition as a threat to the banking system is underhand and does little to foster trust, especially among the younger generation and those eager to see a better distribution of opportunity.

And amping up the role of banks in the US economy weakens credibility by shining the spotlight of public scrutiny on their claims.

But, given the hold of the banking lobby on politics, a compromise was needed – it would be very good news if CLARITY passes. Yes, it will have much that crypto advocates hate; but it will establish a framework within which traditional and new businesses can explore the construction of tomorrow’s finance, without fear that a change in Administration three years from now might unwind progress. Agency rulings are easy to undo; laws are not.

As regular readers will know, I personally don’t see a prohibition on stablecoin interest as a problem at all. Stablecoins should move, not passively sit there. If tokenization advances through rulemaking and oppressive disclosure rules for safe assets are relaxed, the tokenized money market fund market could give stablecoin holders yield while boosting the transparency and liquidity of stable collateral.

The leaked details so far look encouraging: no yield on idle balances, but third-party distributors will be allowed to offer rewards for activity. There will of course be some leeway of interpretation on both sides, and hopefully the Act will include clarity (ha!) on what is a reward vs what is a yield – but some incentivization is fair and could boost both adoption and, if based on activity, circulation.

Macro: about those rate cuts

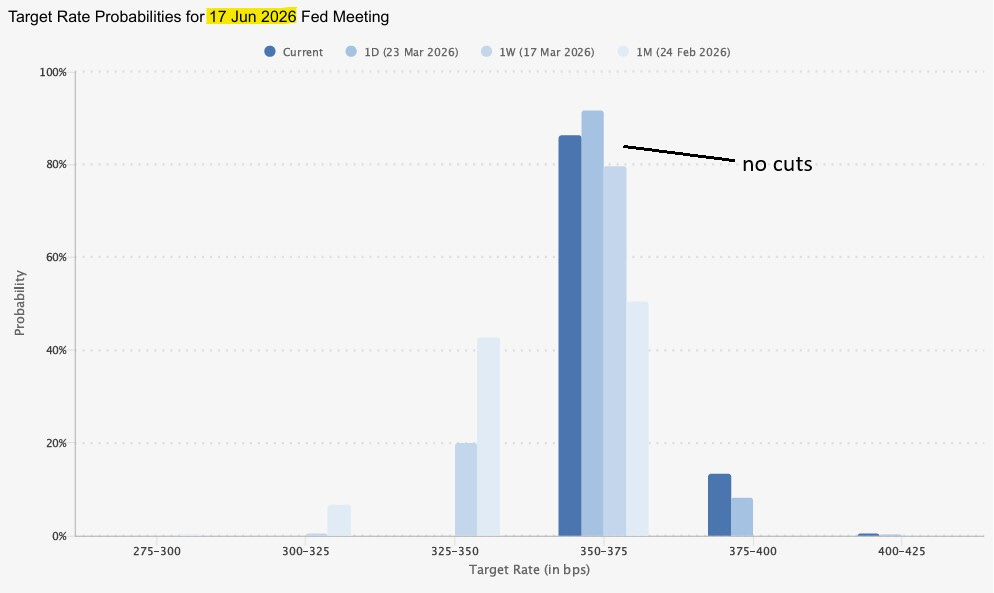

The whiplash is quite something. A month ago, CME swaps were pricing in a rate cut in June. Now, it’s October of next year.

(chart via CME FedWatch)

And the probability of a rate hike by the end of 2026 is now up to 22%.

I’m not a perennial contrarian, really I’m not – I have no problem at all agreeing with consensus when, you know, I agree with the consensus. But on rates expectations, I’m starting to feel like one.

The market has been super-confident about rate cuts ahead over the past year or even more, and I’ve been arguing that they are not necessary and potentially dangerous. Now that the market is all bearish on rate cuts, I think we’ll get them, and possibly soon.

Yes, inflation has for a while been a much stronger risk than high unemployment, and Chair Powell did stress in his press conference last week that keeping prices stable was the priority.

And the war in Iran is almost certainly going to push prices sharply higher in the short-term.

Indeed, the 1-year inflation rate suggested by market pricing of linked Treasuries has shot up to over 5%.

(chart via @joebrusuelas)

But inflation triggered by a supply shock is very different from inflation triggered by increasing demand. And the coming increase is going to be from a supply shock, with prices of energy and other key commodities surging. Higher energy prices tend to seep through to pretty much everything – but spending more at the pump and on other essentials such as food is going to hit overall demand, keeping increases muted.

Food and energy prices are tragically going to climb and remain high for a while, at least until the utter mess of Middle East shipping is sorted out and production and refineries are running again at full capacity – even if a peace deal were to be agreed tomorrow (unlikely), that would take months at best.

However, what matters for monetary policy is core inflation, which strips out food and energy. Given the hit to demand, we’re likely to see that slow down. Unfortunately, that won’t be cause for any celebration.

The US economy as a whole will, of course, benefit from higher energy prices as it is a net exporter. And military spending will shoot up to replenish hardware, adding further stimulus. Both sectors should help keep GDP from dropping sharply – but the gains will be relatively concentrated, not necessarily spreading evenly throughout the economy. More income, even if initially just in a few sectors, will help keep the overall consumption motor going – but the jobs boost may end up being less than many expect, as a significant percentage of the needed roles are instead filled by AI agents or machines? And if they’re not, then where are the AI-related bottom line gains that are supposed to justify the exorbitant capex?

Meanwhile, there’s no way US exporters won’t feel the pinch from a drop in global demand – we’re already seeing governments and airlines announce suspended flights, reduced workweeks, fuel rationing and other measures to slow down activity. This is even before we take into account the hit to economic activity from a stock market correction.

That in turn will tighten financial conditions – which the Fed may well need to offset via easing.

So, while we may not quite get deflation, we are likely to see demand-driven disinflation in coming months, and uneven economic growth as some sectors get hit hard by a combination of lower demand and tariff-driven margin squeezes. Not the recipe for interest rate hikes. Yet again, I think the market is getting it wrong.

A new stablecoin dashboard

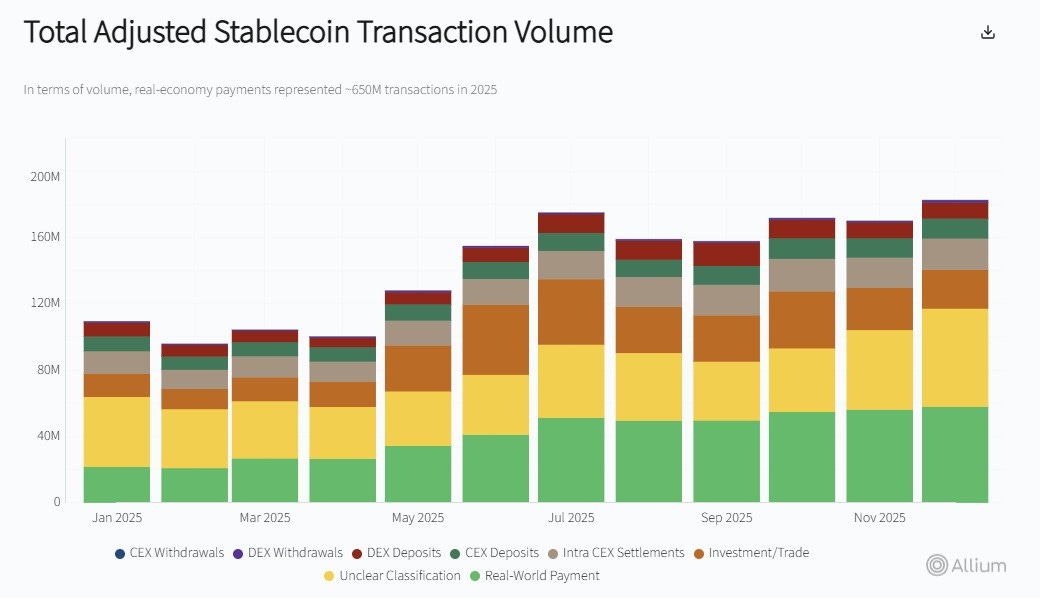

For those of you who like easy-to-understand charts on stablecoin growth broken down by use case, you’ll like the new Allium dashboard created for BCG.

For instance, the below chart – stripped of “noise” – shows that the monthly number of real-world payment transactions using stablecoins more than doubled from January to December last year.

(chart by Allium via BCG)

I haven’t checked the downloadable data, but that looks like easily the fastest growing use case. So, brace for more M&A and investment in stablecoin payments infrastructure.

Note: Allium are sponsors of this newsletter, but they didn’t ask me to share this dashboard, am doing so because I think it’s useful.