A turning point

plus: the market reaction, narratives, US inflation, what's ahead this week, and more

“I prefer peace. But if trouble must come, let it come in my time, so that my children can live in peace.” – Thomas Paine ||

Hi everyone, and welcome to March, which already – one day in – looks like it will match if not exceed February and January in terms of craziness. I hope you’re all taking care of yourselves.

My second eye operation went well but the recovery has been much harder than with the first, not helped at all by coming down with the flu the day after. Foggy brain today, not great timing, I know.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Coming up this week: China’s political meetings, US jobs + activity, Merz in US

Monday mood: a turning point

Markets: the reaction

Macro: PPI

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

Coming up this week:

Let’s be honest, what matters this week for markets is the escalation in the Middle East. But here’s other stuff going on that adds to the complex outlook.

Today (Monday), German Chancellor Friedrich Merz begins a US trip that is expected to include a meeting with President Trump. I wonder what they’ll talk about…

And we get the Institute of Supply Management (ISM) report on February US manufacturing activity, expected to hold steady in a modest expansion.

Tuesday kicks off the US midterm election season, with voters in Texas, Arkansas, and North Carolina electing their party’s candidates for the November vote.

And the skies give us a total lunar eclipse, which will appear as a “blood moon” across the Americas, Asia and Oceania.

Wednesday kicks off China’s annual “Two Sessions”, the most important political gathering of the year. Day 1 warms up with the Chinese People’s Political Consultative Conference which brings together around 2,200 representatives from the Communist Party, business and academia, as well as from Hong Kong and Macau.

We also get the private ADP US payrolls report for February, with the consensus estimate pointing to an increase of 45,000, up from January’s 22,000.

The ISM drops its report on US services activity, expected to show continued yet modest expansion.

And we get the Federal Reserve’s Beige Book, which will shed anecdotal light on US business sentiment.

On Thursday, China opens its National People’s Congress, which brings together Communist Party representatives from around the country and across governmental departments. Premier Li Qiang will deliver the Government Work Report which sets economic targets and outlines priorities – the GDP target is expected to drop from 5.0% to 4.5%. Over the next 10 days or so, we should get more detailed information on the 15th Five-Year Plan which sets out longer-term goals on growth, technology, security and other economic priorities.

Continuing with the week’s US employment data, we get the Challenger job cuts for February, expected to come in under January’s 108,435.

Also, the US import and export price indices are forecast to show accelerating growth.

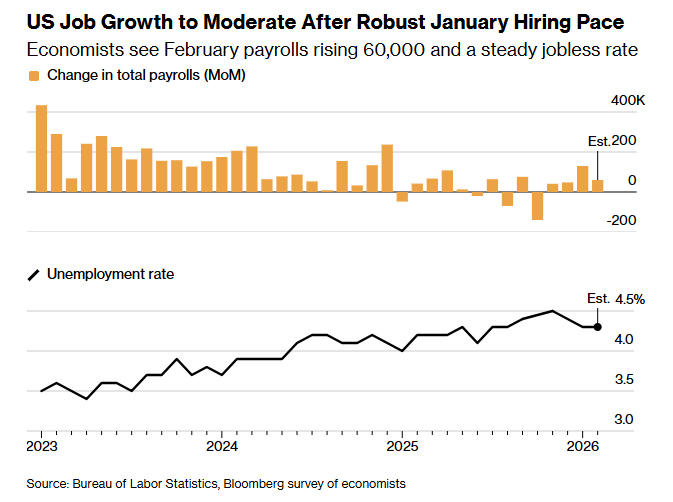

On Friday, we get the US jobs report for February, with the increase in payrolls expected to drop to 60,000 from January’s 130,000 (which will probably get revised down). The unemployment rate is forecast to hold steady at 4.3%.

(chart via Bloomberg)

We also get US retail sales data for January, with expectations pointing to a month-on-month contraction after no growth in December, but any signal from this will be obscured by the impact of winter storms.

Monday mood: a turning point

(what’s on my mind as we head into the week)

In times of fear, we all crave reassurance, and there are few more certain triggers of fear than an outbreak of war. This is especially acute when it is playing out on our screens and feeds, and when so many of us have friends or colleagues in the Middle East. I hope everyone you care about is safe.

This reassurance craving has a downside, which is an instinctive lunge towards the dopamine hit of “news”, even though we know much of it is manipulated and inaccurate – many grasp at headlines as a comforting confirmation of why we’re scared, and we unwittingly spread confusion in our search for connection (and sometimes, sadly, engagement). Even accurate reports – of tragic deaths, bombed hotels, cancelled flights – do little to paint a picture of what’s ahead.

Put differently, we have plenty of information, but most of it is not helpful.

We know more about what we don’t know than about what we do. The decapitation strikes – with 48 senior Iranian leaders reported killed, including the Supreme Leader, Ayatollah Ali Khamenei – were startling in their efficiency, but we don’t yet know who will take the leaders’ place, how much internal support they have, nor for how long they’ll survive in their positions.