AI, crypto and democracy in the rear-view mirror

plus: what's ahead this week, some listening recommendations, and more

“This unprecedented concentration of knowledge produces an equally unprecedented concentration of power.” – Shoshana Zuboff ||

Hello everyone! I hope you had a refreshing weekend.

Come join me and Izabella Kaminska tomorrow for Episode 2 of our 📽 pilot Monetary Forces livestream series. I’ll be diving deep into the concept of moneyness and how that applies to stablecoins, and we’ll highlight a couple of “regime change” stories that caught our eye. More details below.

I know it’s a holiday for many of you this Friday, so this newsletter will also take a break. Unlike most of my European compatriots, I don’t have any big summer holiday planned, but I will be taking Fridays off here and there to refresh.

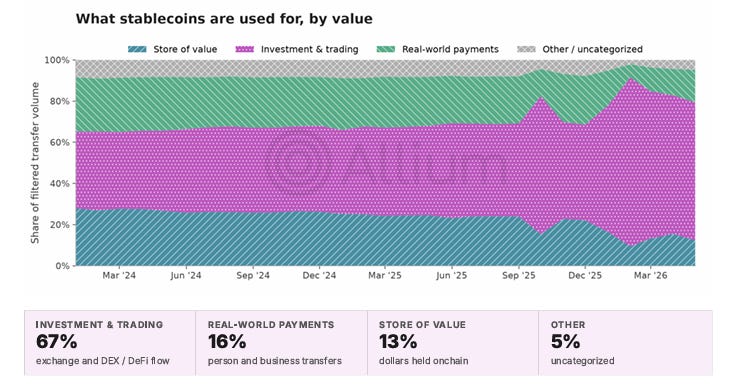

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

A large share of onchain stablecoin movement is automated or internal: market-maker rebalancing, exchange sweeps, looping through smart contracts, and wallets shuffling funds between their own addresses. Counting all of it overstates how much real sending and spending happens.

Would you like to know how much of stablecoin volume is real?

→ Book a demo: https://www.allium.so/

IN THIS NEWSLETTER

Coming up this week: central banks, US jobs

Monday mood: AI, crypto and democracy in the rear-view mirror

Podcast episode recommendations

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you so much!! ❤

WHAT I’M WATCHING:

✨Podcast: Monetary Forces

Tomorrow, Tuesday June 30th at 4pm CEST / 10am EST, Izabella Kaminska and I will be livestreaming episode 2 of our pilot seasonal Monetary Forces podcast, where we look at the impact of new technologies on the financial and economic landscape.

I’m going to dive into the “moneyness” of stablecoins, and how I’m changing my mind on that. Plus, we’ll discuss a couple of key headlines and reports from the past few days.

If you missed our first episode, you can catch up here.

Tuesday, at 4pm CEST / 10am EST – I hope to see you there! Here’s the link to the livestream: https://open.substack.com/live-stream/255145

Coming up this week: central banks, US jobs

Today sees the opening of the ECB’s annual confabulation in Sintra, Portugal, which brings together central bank governors from around the world as well as academics and policymakers. The interesting day is on Wednesday, so scroll down for more.

On Tuesday, the flurry of jobs data begins on Tuesday with the Job Openings and Labor Turnover Survey report for May, with the consensus forecast suggesting a slowdown from the previous month, but to a still strong figure.

We also get the latest Conference Board consumer confidence report which is expected to show a slight sentiment improvement.

And we get June inflation data for several key European countries including Germany, expected to show a slight softening.

Fed Chair Kevin Warsh debuts on the global stage on Wednesday when he shares a panel with the governors of the Bank of England (Bailey) and the Bank of Canada (Macklem), and the President of the ECB (Lagarde). This is part of the ECB’s annual Sintra conference, and is scheduled for 2pm Portugal time (CET-1) – you should be able to watch the livestream here.

At 9:45am on Wednesday, the ECB Sintra conference has a session on tokenization chaired by ECB Executive Board member Piero Cipollone and featuring a discussion of a paper on unified ledgers by Bank of Korea Governor Hyun Song Shin. This should also be livestreamed.

And we get the private ADP payrolls data, as well as the latest announced job cuts report from Challenger, Gray & Christmas.

There’s more (Wednesday is quite the day): we also get the June US Purchasing Managers Index reports from ISM and S&P Global – both are expected to show that manufacturing activity remained solid in June.

And the preliminary June inflation read for the Eurozone is forecast to show that the core index year-on-year growth held steady at 2.6%.

On Thursday, we can obsess over the official US jobs data for June (out a day earlier than usual because of the 4th of July market holiday on Friday). Consensus estimates point to a gain of 115,000 jobs, lower than the 172,000 jobs creation in May but still part of the best six-month stretch in almost two years. The unemployment rate is forecast to hold steady at 4.3%.

(chart via Bloomberg)

Friday is a holiday in US markets instead of the 4th of July which this year falls on a Saturday.

Monday mood: AI, crypto and democracy in the rear-view mirror

(what’s on my mind as we head into the week)

The backlash against AI seems to be getting louder.