Conflict complications and crypto

plus: market green shoots, US inflation divergence, what's ahead for the week

“Both optimists and pessimists contribute to society. The optimist invents the aeroplane, the pessimist the parachute.” – George Bernard Shaw ||

Hi everyone! I hope you all had a good weekend! I’m glad to be back at my desk, but it was lovely seeing my father and other family in Kingston-upon-Thames over the weekend, with its beautiful weather, sparkly river, colourful boats…

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

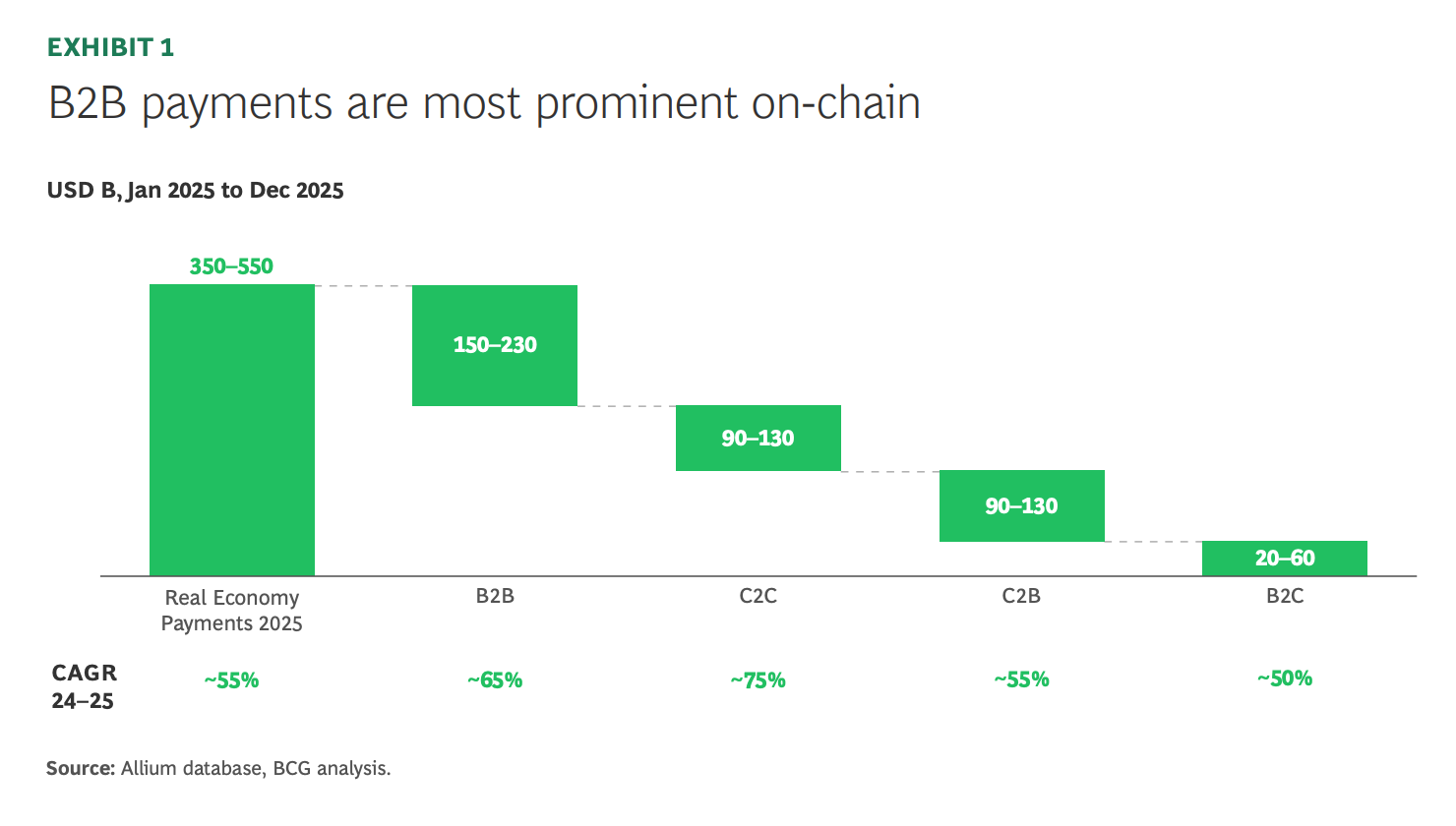

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Coming up this week: central banks

Monday mood: conflict complications and crypto

Macro: US inflation, again

Markets: green shoots, but of what?

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

✨ Use the discount code MACRO for 20% off!

Coming up this week:

Fed week! Rate decisions are due this week from all the G7 central banks and a few more, with each expected to signal caution. If there was any doubt that the global easing cycle is over, markets are pricing in rate **hikes** for 2026 in the UK, Eurozone, Japan, Australia, Canada, Switzerland and Sweden.

Attention will, as usual, focus on the signals coming out of the US Federal Reserve, which will wind up its two-day meeting and present an interest statement as well as updated economic projections on Wednesday. These are expected to keep interest rates steady, and will probably reflect deepening caution by hiking the median inflation, unemployment and end-of-year fed funds forecasts from Fed officials.

The market reaction could be compounded by Wednesday’s release of the February Producer Price Index (PPI), a measure of wholesale inflation – this is expected to accelerate to 3.2% year-on-year from January’s 2.9%, with the core PPI (ex-food and energy) accelerating to 3.7% from 3.6%. It’s worth remembering that this data is from before the conflict in the Middle East sent oil prices soaring.

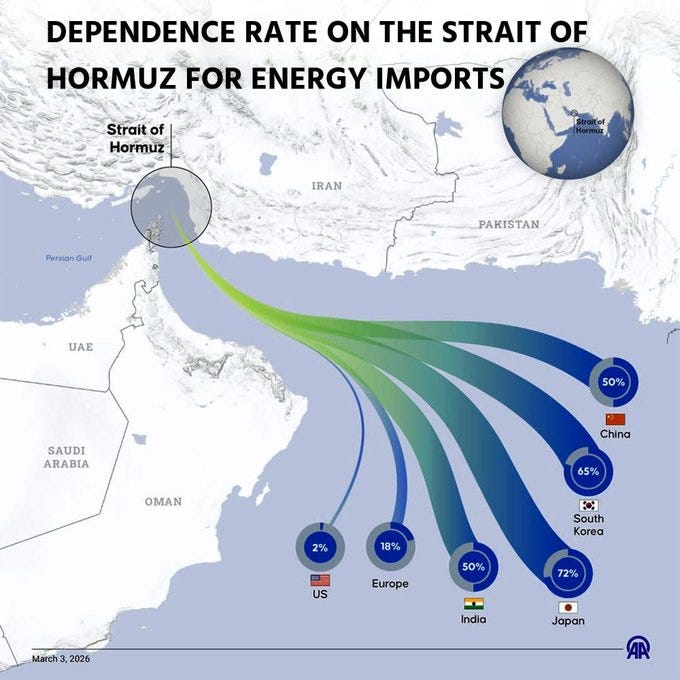

On Thursday, the Bank of Japan delivers the results of its policy deliberations, and while a rate hike is expected in coming months, it probably won’t be just yet. Then again, Japan is reliant on oil imports from the Middle East and is particularly affected by the closure of the Straits of Hormuz, and will have to balance the threat to inflation with the hit to the economy.

(map via @AzizSapphire)

This will be happening while Japan’s Prime Minister Sanae Takaichi is in Washington D.C. meeting President Trump.

Also on Thursday, the Bank of England is expected to pivot from a priced-in cut to a hold as the authorities keep an eye on the oil price impact on inflation despite signs of weakening economic growth.

Friday is a “quadruple witching” day in US markets, with futures and options on stock indices as well as single-name stocks all expiring.

Monday mood: conflict complications and crypto

(what’s on my mind as we head into the week)