ECB: stablecoins bad, CBDCs good

plus: distorted markets, climbing inflation expectations, and more

“Clothes make the man. Naked people have little or no influence on society.” – Mark Twain ||

Hello everyone, and happy Friday! We have a rainy weekend ahead here in Madrid, but I hope you get blue skies where you are.

👀 You’re reading Crypto is Macro Now, where I look at why crypto matters for the macro economy. 👀

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

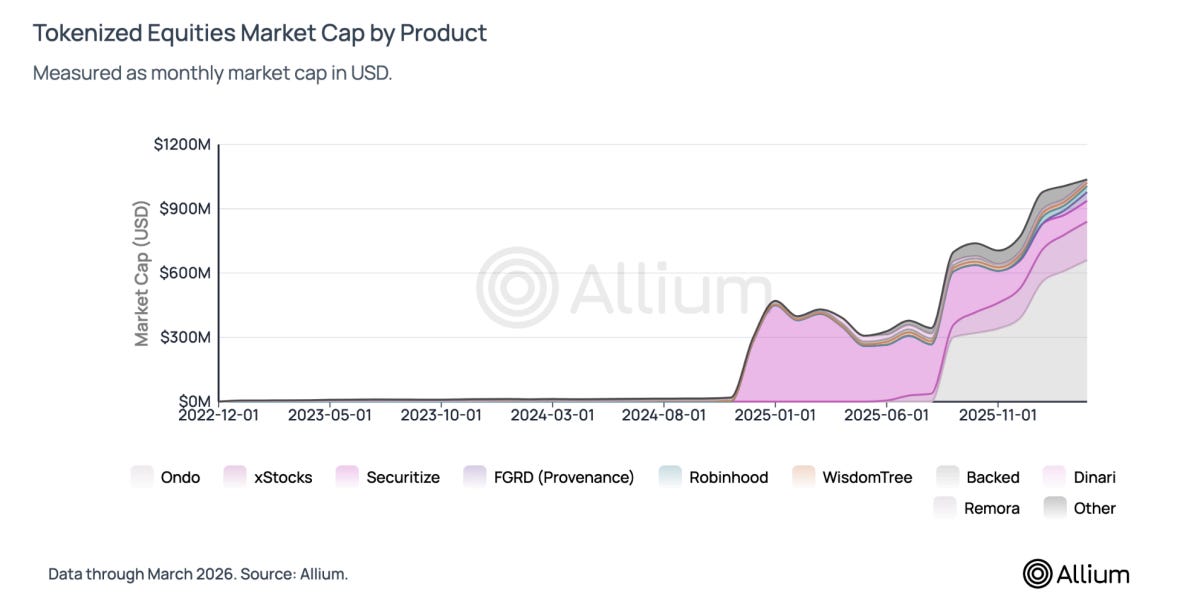

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

IN THIS NEWSLETTER

ECB: stablecoins bad, CBDCs good

Markets: distortion

Macro: inflation expectations

Term of the day: Desalination

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you so much!! ❤

WHAT I’M WATCHING:

✨Press Publish with John ‘Alyosha’ Johnston✨

Come join me later today at 11am EST/5pm CEST in a conversation with John ‘Alyosha’ Johnston, author of the Market Vibes newsletter on Substack.

If you don’t already know JJ’s work, it’s an essential read for anyone interested in markets and/or commodities, written by someone who brings decades of trading experience to your inbox and yet still treats each day as an adventure in learning and sharing. We’re not going to chat about price uncertainty or macro, though. Instead, we’re going to discuss newslettering – why JJ does what he does, how he gets so much done, what’s worked for him on Substack, what advice he’d give others starting out, and more.

Here’s the link: https://open.substack.com/live-stream/186459?utm_source=live-stream-scheduled-upsell

ECB: stablecoins bad, CBDCs good

Earlier today, ECB Chief Christine Lagarde gave a speech about stablecoins. Unsurprisingly, she painted them as much riskier for the European economy than the digital euro CBDC her institution is so enthusiastically promoting.

She recognizes that stablecoins have efficiency benefits, but stresses that there are tradeoffs:

There’s the financial stability risk via a failure cascade – should problems at one bank, for instance, weaken confidence in a stablecoin’s backing, a wave of redemptions could accelerate destabilization.

(I’ll add that this is a key weakness in the MiCA regulation, which insists that stablecoin reserves be at least partly held as bank deposits – banks are not as “safe” as government debt, but the EU does not yet have a deep and liquid government debt market. I’ll also suggest that stablecoins could end up smoothing any banking crisis as an alternative transaction mechanism when everything else is freezing up.)

There’s also the inevitable weakening of monetary policy and therefore the ECB’s ability to maintain price stability. If funds migrate to stablecoins, banks will lend less and the passthrough from official interest rates to the economy weakens.

(Lagarde paints as a given an outcome based on the flimsy assumption that stablecoin reserves won’t find their way back into banks, either directly as part of reserves or indirectly as deposits from those selling the reserve securities.)

These tradeoffs, she argues, are not compensated by the short-term gain of better payments and a potentially broader euro reach. Put differently, the risks outweigh the benefits:

“If we want to strengthen the international appeal of the euro, stablecoins are not an efficient way of doing so.”

The problem, she suggests, isn’t the underlying technology – that is “genuinely transformative”. No, the problem is the involvement of the private sector.

Put simply, only central bank money can be trusted – and therefore, the digital euro checks all the benefit boxes of private stablecoins, without the risk. (Actually, no it doesn’t – stablecoins come with network effects that the digital euro won’t necessarily have, such as participation in DeFi and other yield generating applications.)

The ECB chief’s remarks come as the European stablecoin consortium Qivalis grows to 25 members and continues to make progress towards launch later this year (for more on this, see this excellent report in Blockstories.)

Now these banks are told by their key regulator “I don’t like what you’re doing”, as the regulator sets up a direct competitor to the banks it is tasked with overseeing. It’s not just the push for a CBDC as an alternative to stablecoin digital money; it’s also the issuance of ECB wallets to the retail sector, with no thoughtful debate on whether a central bank should be directly interacting with individuals. And there’s the uncontested assumption that public institutions are better stewards of financial innovation than private entities, so the latter should be discouraged.

This is especially jarring given signs that Lagarde does not understand stablecoins.

Early on in the speech, she falls into a tempting misconception laced with condescension. She says:

“To make a specific type of crypto-asset usable for settlement, the creators of stablecoins anchored them mainly to fiat money, the very system they had originally sought to bypass.”

Here she is lumping all crypto entrepreneurs into the Satoshi Nakamoto bucket, which either displays a wilful ignorance, or a deliberate use of language to imply failure and compromise. Stablecoin creators never “sought to bypass” fiat, their objective was to link the fiat and crypto worlds, and arguably they have succeeded. Obviously, Lagarde is unhappy about that.

Lagarde’s depressing conclusion distils down to this closing remark:

“Our task is not to replicate instruments developed elsewhere, but to build the foundations and the infrastructure that serve our own objectives, so that we can harness the benefits of innovation without importing the fragilities.”

It continues to astonish me that report after report, statistic after statistic conclude that Europe is too conservative when it comes to innovation and development, and yet these loud signals continue to be ignored even as the bloc’s economy loses more talent and funding.

It begs the alarming question of what would stem the trend? What would weaken the bloc’s collective conviction that only increasingly centralized power can ward off risk?

Unfortunately, the usual trigger for a radical change in mindset is a crisis. No one wants that. But until the mindset changes, Europe is increasingly likely to get one.

See more:

EU tokenization and wholesale CBDC (March 2026)

Digital euro politics (Feb 2026)

Digital euro deadlines (Jan 2026)

From Blockstories - Exclusive: Qivalis Gains Momentum with 25 Additional Banks Set to Join (yesterday)

Speech by Christine Lagarde: Stablecoins and the future of money: separating functions from instruments (today)