Friday, April 26, 2024

GDP ouch, stablecoins as payment tokens, suing the SEC

“I'd take the awe of understanding over the awe of ignorance any day.” – Douglas Adams ||

Hi everyone, and happy Fridayyyyy!!!! I hope you have good things planned for the weekend.

I apologize, yet again I have to skip the audio recording, I’m not at my desk this morning.

If you find this newsletter useful, would you mind sharing it with your friends and colleagues? ❤

IN THIS NEWSLETTER:

GDP ouch

A stablecoin snapshot

Stripe and stablecoins

Suing the SEC

If you’re not a subscriber to the premium daily, I hope you’ll consider becoming one! You’ll get ~daily insight into the growing overlap between the crypto and macro landscapes, as well as some useful links, and (usually!) access to an audio read of the content. And there’s a free trial!

WHAT I’M WATCHING:

GDP ouch

Those were some really bad US GDP numbers.

Not only did the Q1 growth come in at 1.6% annualized, less than half that of Q4’s 3.4%, but it was much, much less than consensus forecasts of 2.5%.

Q1 sales growth was 2.0%, almost half that of Q4’s 3.9%.

And real consumer spending grew an anaemic 2.5%, vs 3.3% in Q4 and 2.8% expected.

Yesterday, I wrote about how the flash PMIs were suggesting that there would be some disappointment, but I didn’t think it would be this drastic.

Even more worrying is the data for prices. The Q1 core PCE index growth accelerated from 2.0% in Q4, to 3.7% – not only is that in the wrong direction, it is now almost double that of the Fed’s official target. This was entirely driven by a 5.4% annualized growth in services expenditure, up from 3.4% in Q4. Stripping out food, energy and housing (to get a measure closely followed by Fed Chair Jerome Powell), “supercore” Q1 PCE jumped 3.3%, vs 1.3% in Q4. Services inflation is most enthusiastically back, at least as far as quarterly reporting. We could get a contradictory read in today’s monthly PCE data – or, we could get a disheartening confirmation of the trend.

(chart via Bloomberg)

Slowing growth with accelerating inflation is just about the worst possible scenario, because there is no obvious fix. Faced with an economic slowdown, the Fed in theory should be cutting rates to stimulate activity – but doing so when price increases are accelerating could trigger a destructive inflationary spiral.

Strangely, the slowing economic growth is not yet reflected in employment numbers, which suggests that inflationary pressures are likely to continue. Yesterday also delivered data showing a drop in initial and continuing jobless claims, when consensus forecasts pointed to an increase for both.

The market did not like this. The yield on 10-year US treasuries spiked and stayed high, unlike with usual knee-jerk reactions.

(chart via TradingView)

Strangely, the DXY index jumped but then corrected, which suggests an emerging risk premium in US bonds.

(chart via TradingView)

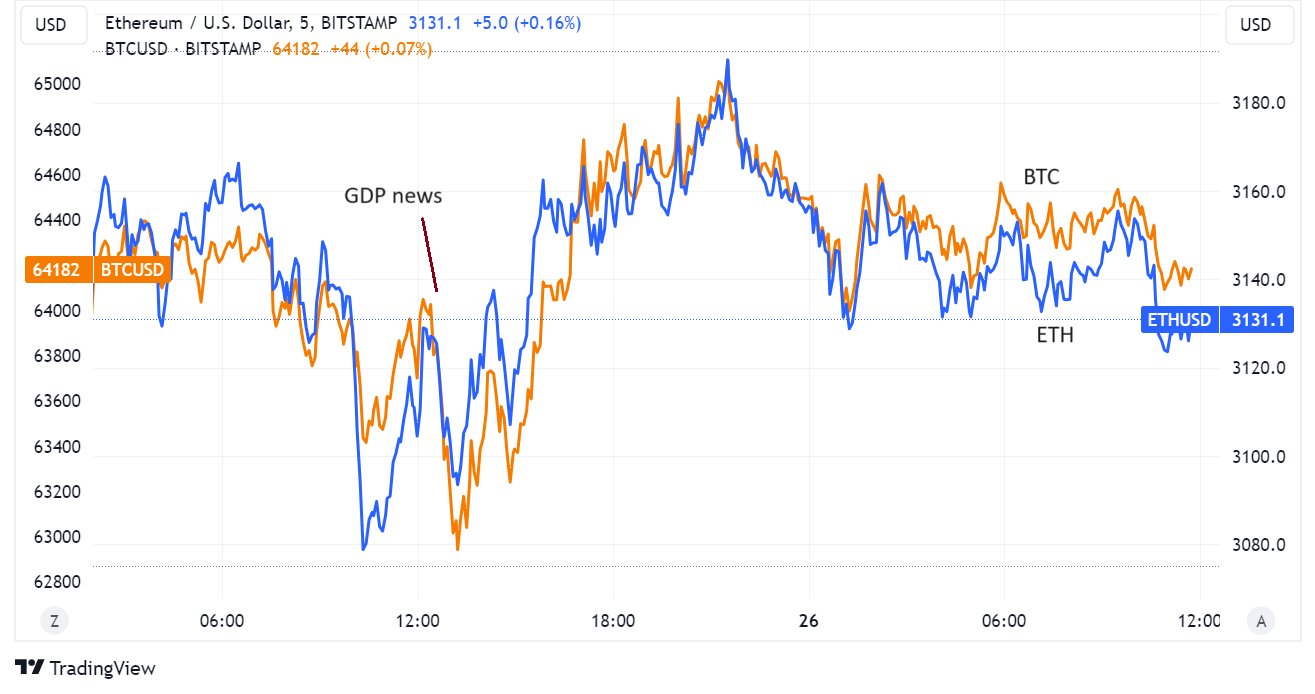

And BTC and ETH held up relatively well, falling but not by as much as you would expect given the move in US yields and the further pushback of any expectations of rate cuts.

(chart via TradingView)

But don’t worry, US Treasury Secretary Janet Yellen obviously has access to different and more reliable data, because yesterday she assured us that fundamentals were “in line with inflation continuing back down to normal levels”. Oh, and that fighting inflation remains President Biden’s top priority. I presume this means that fiscal spending will be walked back? Yeah, probably not.