Friday, August 30, 2024

why jobs data now matters more, who owns bitcoin, even more blatant examples of censorship

“I've heard there are troubles of more than one kind;

Some come from ahead, and some come from behind.

But I've brought a big bat. I'm all ready, you see;

Now my troubles are going to have troubles with me!” – Dr. Seuss 🌻

Hello everyone, and HAPPY FRIDAY!!! Anyone else feeling a bit sad that summer’s drawing to a close?

Today I look at why jobs data suddenly matters more for market attention than inflation and economic growth, at who owns bitcoin, and at signs of increasingly blatant censorship.

You’re reading the premium daily Crypto is Macro Now newsletter, in which I look at the growing overlap between the crypto and macro landscapes. If you’re not a subscriber, I hope you’ll consider becoming one?

Programming note: This newsletter will take a break for the US Labor Day on Monday (what?? Labor Day already???)

IN THIS NEWSLETTER:

It’s the jobs, stupid

Who owns bitcoin?

The drums of dissent

Brasil wants control

If you find Crypto is Macro Now in any way useful or informative, would you mind sharing it with your friends and colleagues, and maybe encouraging them to subscribe? ❤ I’d be really grateful!

WHAT I’M WATCHING:

It’s the jobs, stupid

Yesterday saw a slew of key US economic data releases that point to still-strong economic growth coupled with cooling inflation on both sides of the Atlantic. But that’s not the interesting part.

What grabbed my attention was the unusual amount of noise around an often overlooked and questionably relevant data point: the weekly initial jobless claims.

(via @YahooFinance)

It came in pretty much in line with expectations – 231,000 new unemployment claims filed last week, vs 232,000 expected and 233,000 the previous week. A 1,000 difference is no big deal, especially given how volatile this read is.

(chart via Investing.com)

For smoothing, it’s more useful to look at the four-week average of initial claims – this headed down for the third week in a row but, zooming out, is within a typical ex-pandemic range. So, not much news here, either.

(chart via Investing.com)

The fuss seemed strange, given that there was a lot of other data yesterday that is economically more significant.

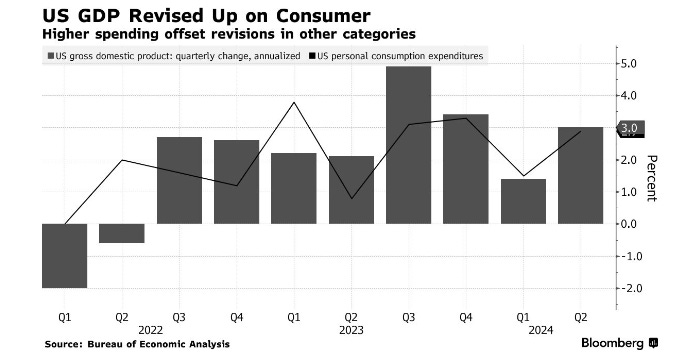

US GDP for Q2 was revised upward, to 3.0% from the initial read of 2.8% and 1.4% in Q1. Real consumer spending for Q2 was revised up by even more, from 2.3% in the first read to 2.9%, vs 1.5% in Q1. Sure, this is backward-looking, but it doesn’t feel recessionary.

(chart via Bloomberg)

What’s more, the Q2 core Personal Consumption Expenditure index – the Fed’s preferred measure of inflation – was revised down, from 2.9% in the first read to 2.8%, vs 3.7% in Q1.

Stronger growth coupled with slower inflation looks like cause for celebration, right? Inflation “vanquished” without a recession?

Turn up the noise

So why, then, the focus on an ever-so-slightly weaker jobless claims figure?

I have two theories here.