Friday, Dec 30, 2022

"Be at war with your vices, at peace with your neighbors, and let every new year find you a better man." – Benjamin Franklin ||

Hello everyone, and welcome to the last daily Crypto is Macro Now email of 2022! This will be a short one, since I’m sure you have better things to do than read your 37th Year in Review and 24th Predictions for 2023. I seem to be continually making hand-wavy and hedged predictions anyway, so I don’t feel the need to go overboard today just because the calendar is tidily wrapping up the month, quarter and year. I will say that I’m excited about what’s ahead – I believe that we collectively went overboard on hopium at the end of last year, and are doing the same in the other direction now. More on this below.

You’re reading the premium daily Crypto is Macro Now email, where I look at the growing overlap between the crypto and macro landscapes. Nothing I say is investment advice! If you find this useful, I hope you’ll share with friends and colleagues.

And if this was shared with you, or if you arrived here from somewhere other than your inbox, I hope you’ll consider subscribing.

Programming note: this email will be taking a break on the 2nd of January, back in your inboxes on the 3rd. The weekly will be back on the 7th.

MARKETS

As markets limp into the last sprint of a dire month in an awful year, stock markets showed some seasonal cheer while BTC and ETH weakened further.

Continuing jobless claims in the US came in slightly higher than expected yesterday, but new jobless claims were flat and in line, suggesting that there may be some weakening in employment but it’s slight for now. The US 10-year yield drifted lower yesterday as traders celebrated the absence of further jobs market strengthening, but the renewal of inflation concerns has pushed it higher this morning.

(chart via TradingView)

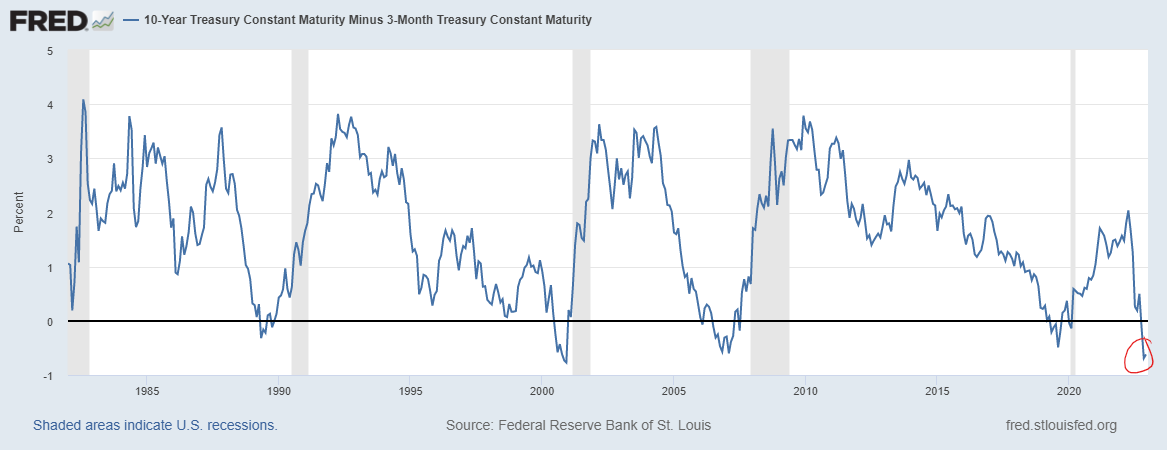

We could be nearing a top, however, as the 10y3m yield curve – a more reliable indicator of recessions than the better-known 10y2y spread, according to Federal Reserve economists – touched its lowest point since 2001 earlier this month but has since started to head up, which is typical once a recession is set in motion and the market starts to adjust.

(chart via the St. Louis Fed)

This is likely to impact the evolution of the dollar against other currencies, although the DXY has not rallied along with the recent increase in US 10-year yields. Could there be other forces at work here?

(chart via TradingView)

Dollar setup

The year closes out with a couple of hints that next year could be a bumpy one for the dollar:

China continues its campaign to enhance the role of its currency on the international stage with the extension of onshore yuan trading hours from 11:30pm local time to 3am the following day, effective January 3rd. The last time trading hours were extended was in 2016, when the yuan was admitted to the basket of currencies underpinning the IMF’s Special Drawing Rights reserve asset.

Russia continued to distance itself from western currencies with an increase in the maximum weightings of yuan and gold it can hold in the national wealth fund to 60% and 40% respectively. Its accounts in British pounds and Japanese yen at the central bank have been set at zero.

Central banks continue to accumulate gold at the fastest pace since 1967, when massive central bank purchases stoked growing doubts about the dollar’s convertibility into gold, which led to the US abandoning its exchange commitment early the following year. Reports point to China and Russia as the largest buyers.

Where we’re at

I promised above that I’m not going to review 2022 for you on the grounds that it’s been done a lot elsewhere, but I will briefly mention a few recent developments that I think highlight that, in spite of this year’s body blows, the stage is being set for a constructive 2023 in terms of investor interest and market evolution.

The CME launched a bunch of new crypto indices this year: 11 including UNI, DOT, MATIC and ALGO back in April, and AAVE, CRV and SNX in December. This does not mean futures products based on these are coming soon, but nor does it mean they’re not – the bigger signal is that the CME, which is in touch with most US investment institutions, sees a demand for a broader range of reliable crypto benchmarks.

Fidelity continued pushing forward on digital asset services, adding ETH trading and an Ethereum trust to its (limited) product suite, finally allowing retail investors to open crypto accounts, and enabling bitcoin investment in employer-approved 401k retirement plans. Retail demand is likely to be relatively low for the next few months at the very least, but when it comes back, Fidelity is likely to be a key on-ramp as a name investors already know and trust.

Several well-known investment names – including KKR, Hamilton Lane and Apollo – launched tokenized funds, broadening the experimentation with this new form of value transmission. We also had some governments and official institutions issuing and trading blockchain-based debt securities, but I feel like the tokenized funds concept will eventually trigger some amendments to US securities rules (new settlement possibilities) at a time they’re being reconsidered anyway. And the EU in March kicks off a distributed ledger trading pilot. This is how financial change happens: gradually then suddenly.

And as for “no way are the institutions coming into the market now” refrain I’ve heard so much recently, even after the FTX implosion several well-known institutional names confirmed crypto expansion plans. This not only shows that conviction continues in some pockets, it also paves the way for new qualified investors to more easily onboard when sentiment lifts:

Goldman Sachs revealed plans to expand its crypto operations by taking advantage of distressed company valuations.

Nomura launched a digital assets arm in September, and even after the FTX implosion was still expecting to expand in 2023 and reach profitability in late 2024.

Venerable US investment bank Cowen Inc. set up a digital assets arm earlier this year, and has confirmed plans to continue expansion in spite of the market contraction.

Investment manager Man Group, founded in the UK over 230 years ago, is reportedly close to launching a crypto fund.

TP ICAP, the world’s largest interdealer-broker, registered as a digital-asset provider with the U.K.’s Financial Conduct Authority.

Switzerland-based Seba Bank opened an office in Hong Kong to offer crypto services to Asia-based institutions.

Other services launched after the May/June crash but before the November drama will further help remove crypto investment barriers for institutions and retail, which could impact the speed of the eventual market upswing.

Institutional custody continued to evolve, with BNY Mellon, BNP Paribas and Nasdaq launching services while new startups working on the concept raised funds.

Société Générale, France's third-biggest bank by market cap, is now authorized to offer digital asset custody and trading.

DBS, one of Singapore’s largest and oldest banks, now offers crypto trading for accredited investors.

Blackrock, the world’s largest asset manager, now offers clients exposure to bitcoin.

Franklin Templeton set up a couple of diversified digital asset trading strategies, and is talking about expanding the range – this will make financial advisers feel much more comfortable helping clients take positions.

Also for retail investors, Robinhood activated self-custody wallets, N26 launched a cryptocurrency trading platform, robo-adviser Betterment now offers crypto asset investing.

And crypto experimentation got creative, with Japanese banking conglomerate SMBC testing soulbound identity tokens, Visa exploring Ethereum scaling solution StarkNet for automatic recurring payments and Franklin Templeton issuing service NFTs to certain clients.

These examples are far from exhaustive, and are meant to show that the outlook for institutional and retail participation in crypto markets is unlikely to be as bleak as current sentiment would have you believe. Over the coming weeks, I’ll be keeping an eye on on-chain indicators as well as derivatives signals, and of course on the headlines that go beyond promotional puff pieces to suggest actual commitment and market innovation.

Crypto is stuck between Putin, Powell and the wicked Gary Gensler is the real problem and there’s nothing we can do about it or so it seems