Friday, Jan 5, 2024

inflationary pressures, BDRs, more education needed, newsletter changes

“For a moment, nothing happened. Then, after a second or so, nothing continued to happen.” – Douglas Adams ||

Hello everyone, and happy Friday!!! I hope you’re able to rest this coming weekend, next week looks like it’s going to be quite hectic…

You’re reading the daily premium Crypto is Macro Now newsletter, where I look at the growing overlap between the crypto and macro landscapes. There’s also usually some market commentary, but NOTHING I say is investment advice. For full disclosure, I have held the same long positions in BTC and ETH for years, and have no intention to either buy more or sell in the near future.

If you’re not a subscriber, I do hope you’ll consider becoming one! It would help enable me to continue to share what I learn as I work on figuring out where we’re going. It’s only $8/month ($90/year) for the next couple of days, going up to $12/month ($108/year) on January 7. More on the newsletter plans below.

If you find this newsletter useful, would you mind hitting the ❤ button at the bottom? I’m told it boosts the distribution algorithm.

IN THIS NEWSLETTER:

Some changes to the newsletter

Yet more signs that rate cuts are a way off yet

The opportunities hidden in the Bitwise survey

What I don’t understand about Bitcoin Depositary Receipts

WHAT I’M WATCHING:

Some changes to the newsletter

This is a repeat of what I wrote in the December 28 newsletter, to explain some of the upcoming changes to Crypto is Macro Now. Since I hope many of you disconnected over the holiday season, and since the price increase is coming up this weekend, I’m bringing it up again in case you missed it.

I took the decision at the end of last year to spend more time in 2024 focusing on the big changes happening at the crypto and macro intersection. This involved stepping back from hosting the CoinDesk Markets Daily podcast. It also involves raising the price of the subscription. I wish I didn’t need to, and I understand that for some of you it might be a hefty cost jump, for which I apologize (given the range of great premium newsletters out there, I know this all adds up) – I’m deepening the discount on the annual subscription, so the increase there is less. As of January 7, the premium subscription will be $12/month or $108/year. Current subscriptions won’t be affected until renewal.

In exchange, you get:

A daily (Monday-Friday) email with trends, narratives and news items that illustrate where we’re heading, plus some useful links. (I will probably have to miss 2-3 days each month because of reasons, and I will every now and then take some days off to recharge, I will flag these well in advance.)

Regularly updated snapshots of where we are with tokenization and CBDCs (starting mid-January).

The occasional essay and deep dive (at least one every two weeks, my goal is to get to weekly).

The occasional interview, starting in February.

I really hope that you stick around! Things are about to get very interesting in both crypto markets and the broader economic landscape, not just in terms of indices and prices, but also in terms of use case. There’s much to talk about – and it matters. 😊

Yet more signs that rate cuts are a way off yet

Strong economic activity:

Yesterday we got the S&P Global Services PMI for December for the US. Not only did it come in slightly higher than expected (at 51.4 vs 51.3 forecast), but it delivered the sharpest jump since June. Services employment growth was the joint-fastest in six months.

A strong jobs market:

We’re seeing the employment pickup in other data points as well. Yesterday’s ADP report on private employment in the US came in much hotter than expected, with a gain in December of 164,000 jobs vs 115,000 expected and a 101,000 increase in November.

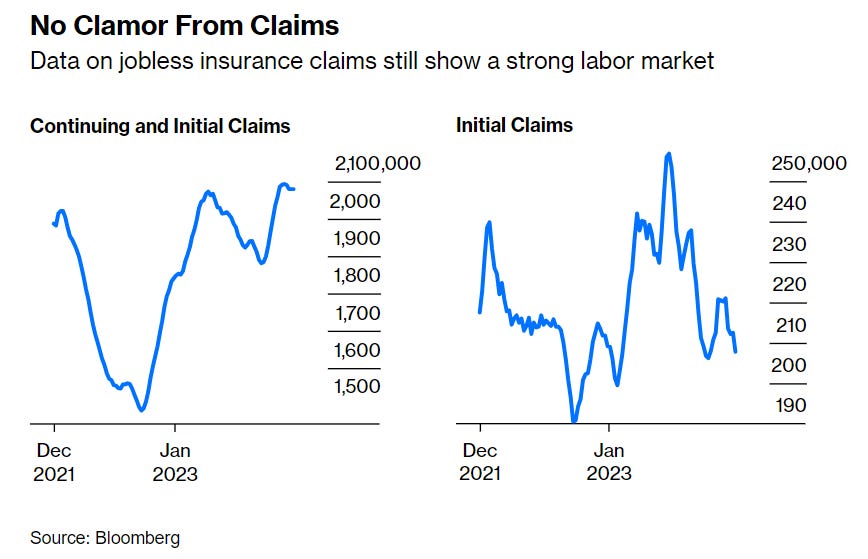

Initial jobless claims of 202,000 were notably lower than both the forecast (216,000) and previous reading (220,000), and the number of continuing claims also dropped (1,855,000 vs 1,886,000 the previous week). The smoothed four-week average of jobless claims is now the lowest since last October. Where is that job market weakening we’ve been worrying about?

(chart via Bloomberg)

Today’s official Bureau of Labor Statistics data on the US job market is expected to show a slight uptick in unemployment to 3.8%, and a slower creation of new jobs. However, recent jobs market indicators, such as those mentioned above, suggest that we could get a surprise to the upside. Given the bond market’s conviction that six rate cuts are coming to the US this year (although this is weakening), we could see some volatile moves in yields and stock indices.

European inflation:

Yesterday I mentioned that German and French CPI increases had accelerated. This morning, we saw the Eurozone CPI increase for December, which – no surprise – also accelerated, for the first time since last April, from 2.2% year-on-year to 2.9%. This is not moving in the right direction, and reinforces the idea – repeated by both European and US central bankers – that getting inflation down to target is not going to be easy.

Core CPI, which excludes the more volatile components of food and energy, increased by 3.4%, slightly less than the 3.5% average forecast, and less than November’s 3.6%. But it’s still notably higher than target, and anyway, consumers tend to focus on the headline figure when shaping their expectations.

What’s more, while Eurozone industrial producer prices fell for December (a drop of 8.8% year-on-year, slightly more than the 8.7% consensus forecast), the drop was less than November’s 9.4% slide. Down is certainly better than up for the inflation battle, but a slowdown of the drop suggests that it may be running out of steam too soon to continue helping with the top-line numbers.

Realigning expectations?

Add all this to the insistence from Fed officials, backed up by the FOMC minutes released on Wednesday, that rates are likely to remain steady for now, throw in an oil price that is pretty much back up to where it was a year ago, and you get a market that is starting to wonder if maybe, just maybe, it isn’t being just a tad too optimistic.

(chart via TradingView)

Meanwhile, the DXY index has been heading up for much of this year so far… as has BTC, even though it typically moves in the opposite direction to the US dollar. True, macro matters are not the driver of bitcoin narratives at the moment. Will that change?

(chart via TradingView)

Perhaps, especially if we see a “sell-the-news” correction after the BTC spot ETFs are approved. Bitcoin is and probably always will be influenced by monetary liquidity and overall investor sentiment. Medium-term, however, other non-macro narratives are getting stronger: