Friday, March 8, 2024

inflation expectations and jobs data, SEC authoritarianism

“Let's think the unthinkable, let's do the undoable. Let us prepare to grapple with the ineffable itself, and see if we may not eff it after all.” – Douglas Adams ||

Hi everyone, and happy Friday!!!! A short one today, with no audio – I got drenched when I went for a walk last night and this morning do not feel great, so I’m going to spend today under a thick blanket with buckets of ginger tea. TGIF!

IN THIS NEWSLETTER:

Inflation expectations and the jobs outlook

Arbitrary and capricious, again

If you’re not a subscriber to the premium daily, I hope you’ll consider becoming one! You’ll get ~daily insight into the growing overlap between the crypto and macro landscapes, as well as some useful links, and (usually!) access to an audio read of the content. And there’s a free trial!

WHAT I’M WATCHING:

Inflation expectations and the jobs outlook

Today, we get the much-anticipated official Bureau of Labor Statistics US employment data for February. You may remember that January’s surprise to the upside (353,000 vs 187,000 expected at the time) was the key catalyst for the recent walk-back of market rate cut expectations, leading us to the three currently priced in today. I wouldn’t be at all surprised to see January’s data revised downward (more on this below), which could start to encourage expectations to move up again.

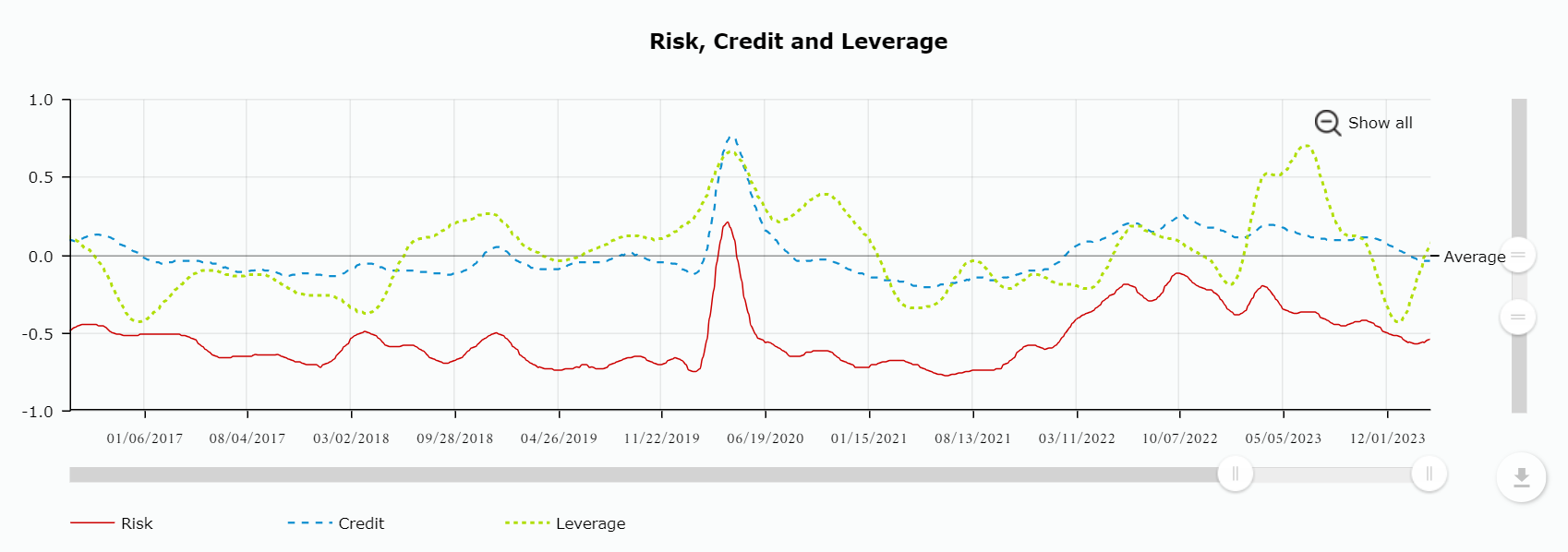

Although, as I suggested in yesterday’s newsletter, I don’t think it matters that much for risk assets anymore. Financial conditions are not exactly tight. The Chicago Fed’s risk index (red line) has been on a loosening trend for the past year, and the credit index (blue line) has just crossed into “looser than average” territory for the first time in two years.

(chart via the Chicago Fed)

The Bloomberg US Financial Conditions Index paints an even more dramatic picture:

(chart via Apollo Academy)

And, looser financial conditions tend to stoke institutional risk appetite. According to State Street, this has been climbing since the end of January.

(chart via State Street)

Looser financial conditions are not just good for markets, they also should – in theory – keep people employed. And US high yield credit spreads, a gauge of corporate health, are at their lowest since the beginning of 2022.

(chart via the Federal Reserve of St. Louis)

There are some signs that the jobs market is softening – for instance, recurring jobless claims have been trending higher over the past six months, which suggests that it is no longer as easy for the newly unemployed to find a new job. And the employment indices from the latest ISM PMI data for both manufacturing and non-manufacturing showed a small drop.

But, on the whole, indicators point to another strong read. Yesterday we saw that weekly jobless claims are, at 217,000, still well below the pre-pandemic 10-year average of 300,000.

Average economist forecasts are for 198,000 jobs added in February, well below January’s data, but not out of line with recent months. What’s more, over the past two years, the actual figure has come in under expectations only six times.

(chart via Investing.com)

As well as how employment is doing relative to expectations, another significant detail from today’s data drop will be the growth in average hourly earnings, since this is arguably a stronger influence on the trajectory of consumer spending and therefore prices. In January, it came in higher than expected at an annual rate of 4.5%, well above the inflation target. The consensus forecast for February is slightly lower, at 4.4%, but still too high to feel confident about inflation coming down.