How stablecoins create money

plus: CPI cooling, and more

“Never follow anyone else’s path. Unless you’re in the woods and you’re lost and you see a path. Then by all means follow that path.” – Ellen DeGeneres ||

Hello everyone! I hope you’re all having a good summer so far.

Apologies for the late send today – a fuzzy day, because WE WON ⚽ 🎉, Spain is in the World Cup finals and last night the racket on the street below my bedroom window went on until the early morning hours. Epic. Happy to be sleep-deprived.

If you missed yesterday’s Monetary Forces livestream with Izabella Kaminska, you can catch it here. I talked about how stablecoins can create money – I’ll expand on that below.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

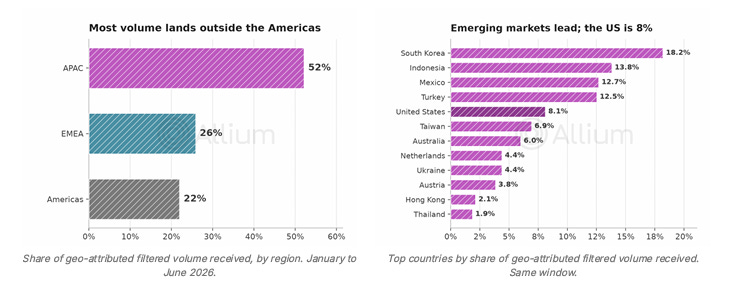

Where are stablecoins most used?

Allium filters stablecoin volumes for non-economic actions such as inter-group transfers – it turns out that most is outside the US, with 52% in Asia-Pacific and 26% in Europe, the Middle East and Africa.

The leading destinations are South Korea, Indonesia, Mexico and Turkey, places with currency pressure, active remittance corridors, or both.

→ For more, download Allium’s State of Onchain Finance report: https://allium.so/reports/state-of-onchain-finance-q2-26

IN THIS NEWSLETTER

How stablecoins create money

Macro: CPI cooling

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you so much!! ❤

WHAT I’M WATCHING:

How stablecoins create money

In yesterday’s Monetary Forces livestream with Izabella Kaminska, I tackled the issue of how stablecoins create money.

I’m going to give myself some points for being brave here, as I am not a monetary expert and knew I’d be presenting to people who understand this field much better than I do (Izabella herself is definitely one of them). Indeed, I was feeling particularly stupid over the weekend as I stared at a confusing mosaic of T-charts with assets on one side and liabilities on the other (I even tried turning them upside down, it didn’t help…).

But I think I eventually got the gist of the moving pieces. And I’m going to trust in the expertise of Claudio Borio, former Head of the Monetary and Economic Department at the Bank for International Settlements (BIS) – we can assume he knows a thing or two about monetary plumbing.

In a paper co-authored with Piti Disyatat and Nikola Tarashev called “Stablecoins and the exorbitant privilege of money creation” and published by European think tank the Centre for Economic Policy Research, or CEPR, Borio lays out how stablecoins add to the money supply.

Below, I’ll summarize the mechanism by which they do so.

First, though, it’s worth underscoring why this matters: most seem to assume that stablecoins are money-neutral. They’re 1:1 backed, no lending involved, therefore the logical conclusion is there’s no new money creation. Borio et. al. explain why this is incorrect. I’m perplexed as to why the banks are not up in arms about this – we know they’re energetically protesting the potential deposit flight towards yield-bearing stablecoins, but they’re fighting in totally the wrong arena.