How tokenized deposits could compete with stablecoins

“If the English language made any sense, lackadaisical would have something to do with a shortage of flowers.” – Doug Larson ||

Hello everyone, and happy Friday! I’m going to try to keep today’s newsletter short because you’re probably even more exhausted than I am. So much going on, though…

I have glimpsed the strong jobs data and seen the eye-opening jump in US bond yields, but I’ll leave comment on that until Monday, generally can’t get much from initial reactions – but, yeah, rate hike expectations will climb further and this isn’t good for crypto.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

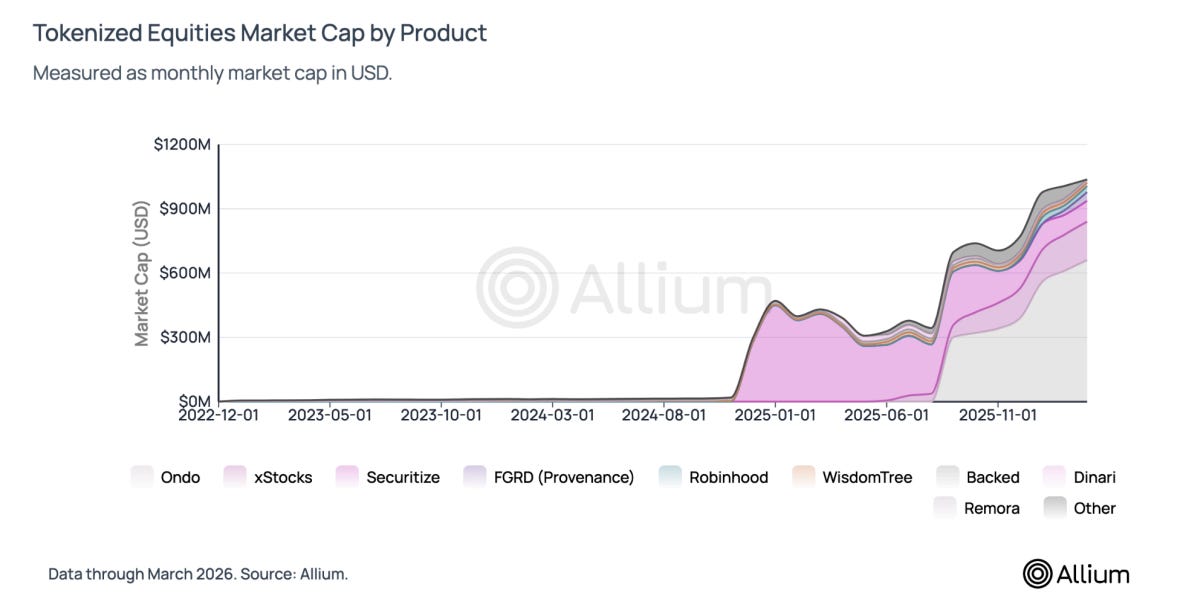

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

IN THIS NEWSLETTER

How tokenized deposits could compete with stablecoins

Term of the day: Balkanized

Recommended podcast episodes

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you so much!! ❤

WHAT I’M WATCHING:

How tokenized deposits could compete with stablecoins

This could work.

I’ve written often over the years on banks, their limited view of blockchain flexibility and how we have to remember that regulated financial institutions have a certain embedded DNA that triggers a recoil in the face of open, public networks. After all, the past few years have drummed into regulated financial institutions the need to document everything, identify everyone and always err on the side of caution.

But they are also increasingly aware of the public relations need to be seen as forward-thinking, abreast of new technologies, not stuck in the past.

So, we’ve seen many banks give lip service to stablecoins, with some even announcing they’re planning a launch. Generally, they don’t mean it. (SoFi is a shining exception, their stablecoin is live and has an interesting hybrid internal-external model, I’ll go into more detail on this next week. Custodia Bank, working with Vantage Bank, also has an innovative stablecoin solution – again, more to come on that. And there’s the Qivalis bank stablecoin consortium over here in Europe which is growing fast and has a good chance of producing something that sticks.)

Over the past year, I lost count of the times I heard a stablecoin practitioner declare “every bank will have a stablecoin!” – mercifully, that narrative is dying down as the bank preference for careful, limited innovation has become more obvious.

A handful of banks have for some time been leveraging private blockchains to move client money internally 24/7, with some launching programmability features. These tokenized deposit services are an improvement on banks’ normally clunky, slow and expensive cross-border transfer systems. But they operate in walled gardens, which limits their advantages to just a small subset of blockchain potential.

Yesterday, the tokenized deposit concept took a big step forward. According to the Wall Street Journal, The Clearing House – a real-time payments company owned by JPMorgan, Bank of America, Citigroup, Wells Fargo and other large US commercial banks – will build a tokenized deposit network for use across the banking sector. Launch is expected in the first half of 2027.