Iran, stablecoins and the digital yuan

plus: market confusion, US jobs, new section and more

“The greatest danger in times of turbulence is not the turbulence; it is to act with yesterday’s logic.” – Peter Drucker ||

Hello everyone! Those of you that took a short break over the weekend, I hope it gave you the chance to recharge. 😊

A couple of announcements:

1) Below I introduce a new section ideal for sticklers for detail such as myself – definitions.

2) My first Substack live series launches this Friday! It’s not about crypto nor macro (that’s coming soon!), but about newsletters. More detail further down.

A long one today, apologies, tomorrow’s will be shorter.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

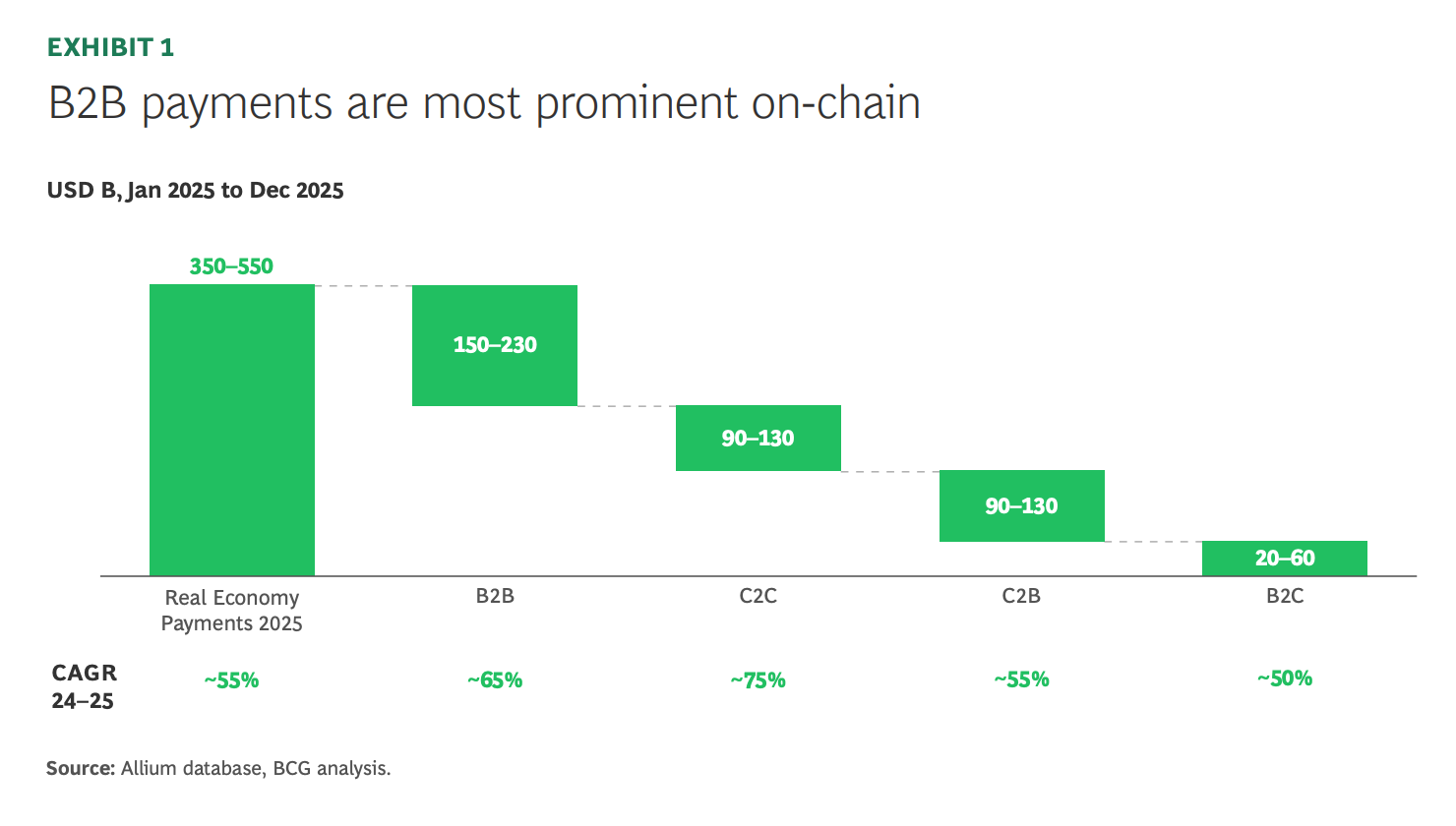

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER

Coming up this week: inflation and geopolitics

✨Introducing “Press Publish” ✨

🔦New section 🔦 Term of the day: Strait

Monday mood: Iran, stablecoins and the digital yuan

Markets: thick confusion

Macro: US jobs

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

✨ Use the discount code MACRO for 20% off!

Coming up this week: inflation and geopolitics

Today, several European markets are closed for the Easter holiday.

The US gets the March report on the ISM services sector activity, expected to show a slowdown.

And President Trump holds a press conference “with the military” at 1pm ET – I’m guessing this will be to trumpet the rescue of two military personnel from inside Iran.

On Tuesday, the leader of Taiwan’s Kuomintang (KMT) opposition party leaves for China and a potential meeting with Xi Jinping – this is significant as it is much more likely that China waits for (and helps along) a government change on the island rather than invade with military force.

Vice President Vance visits Hungary in the run-up to its elections this weekend, presumably to help campaign for incumbent Victor Orban. The EU is not going to like this.

Also, we get the latest New York Fed report on consumer inflation expectations – these are expected to jump from 3.0% to 3.7%.

On Wednesday, we get the Eurozone PPI for March, with the year-on-year contraction expected to slow slightly from -2.1% to -1.9%.

Also on Wednesday, we get the minutes from the latest FOMC meeting, which should shed more light on the shift to a more conservative rate stance.

On Thursday, the US Bureau of Economic Analysis drops the latest report on Personal Consumption Expenditure (PCE), the Fed’s preferred inflation gauge. The month-on-month increase for the core index (ex-food and energy) in February is forecast to hold at 0.4%, while the year-on-year increase in the core index is expected to decelerate from 3.1% to 3.0%.

And the IMF Spring Meeting kicks off in Washington DC.

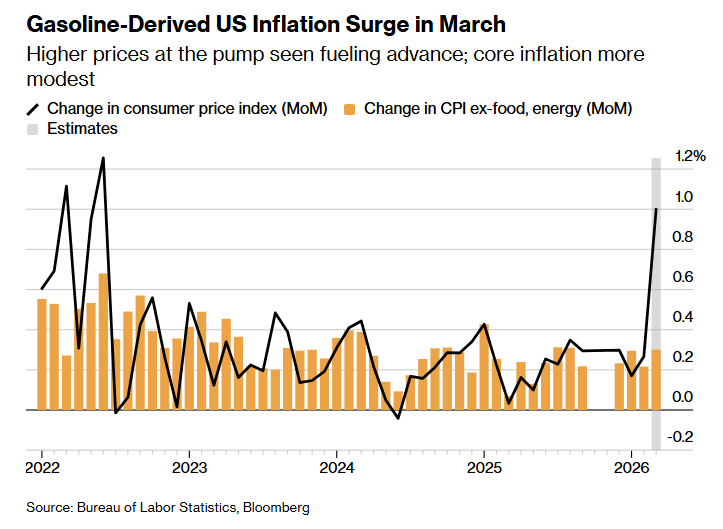

Friday brings the US Consumer Price Index (CPI) inflation read from the Bureau of Labor Statistics, with the headline index for March forecast to show an acceleration from 2.4% year-on-year to 3.4%, and from 0.3% month-on-month to 1.0%, which would be the highest read since 2022. Yikes. The core index (ex-food and energy) is expected to show an acceleration in March from 0.2% month-on-month to 0.3%, and from 2.5% year-on-year to 2.7%.

(chart via Bloomberg)

Also on Friday, we get the latest preliminary consumer survey for April from the University of Michigan – this is unlikely to be rosy.

And over the weekend, Hungary heads to the polls in an election that could unseat Victor Orban, the EU’s most Russia-friendly leader and a thorn in the EU’s political side, after 16 years in power.

✨Introducing “Press Publish”✨

This Friday, I’m launching a Substack live series – not on crypto nor macro (coming soon!), but on writing newsletters. At 11amET, I’ll be talking to fellow newsletter writers about why we do what we do, what our days are like, our frustrations, our wins, our advice, where we think media is going and a lot more.

I’ll be kicking it off with my friend and former colleague Christine Kim, one of the leading experts on the Ethereum ecosystem, now also covering Bitcoin, and the author of the ACD After Hours and BTC Before Light newsletters, host of the Ready for Merge and the Meet the Developers podcasts, and more besides. (You can see her recent publications here.)

Come and join us at 11amET at the following link: https://open.substack.com/live-stream/154954?utm_source=live-stream-scheduled-upsell (I think that’s the link, I’m still getting the hang of this.)

Term of the day: strait

(🔦 Hi all! Introducing a new feature: definitions. With so much jargon floating around, I want to help clarify confusion while poking at semantics, and refresh overall understanding of relevant terms and sometimes phrases. 🔦 So, on most days I’ll define/explain a term I’m seeing that I know not everyone is familiar with, or that we all use without fully understanding. )

🔦 Strait: a narrow passage of water connecting two larger bodies of water. The term evolved from the Latin “strictus”, which means bound tight, compressed, constricted. This became estreit or estrait in Old French, and streit in Old English, referring to a narrow or confined place. Other words that emerged from this root are stringent, strain and, of course, strict.

Should it be “strait” or “straits”? When speaking about geography, either goes, even when talking about just one strip of water – for instance, you’ll see both the Strait and the Straits of Hormuz. If the term comes after the name, such as the Bering Strait (which separates Russia and Alaska), it’s singular – unless there are several water strips, such as with the Danish Straits. But if it comes before the name (such as the Strait/s of Gibraltar), it’s either. Unless, of course, you’re referring to being in a constricted, compressed and generally very uncomfortable situation, in which case it’s “dire straits”, plural.

And it’s never written with a “gh” because straits are rarely straight.

Monday mood: Iran, stablecoins and the digital yuan

(what’s on my mind as we head into the week)

Headlines and articles and posts these days increasingly remind me of that image you’ve no doubt seen of a chinaware cupboard with glass panels, in which the plates have slipped and are only prevented from crashing to the floor by the closed cupboard doors.

(via Buzzfeed)

Only now, the doors are opening a bit, the plates are slipping and it’s not clear when they’ll crash.

Of course, this metaphor can apply to so many aspects of the fragile machine that is capital globalization, from the complacency of privilege to profit-maximizing supply chains to the short-termism of polarized politics to ineffectual financial crime policing. But what started me down this train of thought was an article in Bloomberg last week reporting that Iran will be collecting Hormuz tolls in yuan and stablecoins. I didn’t dwell on it much at the time, I confess, as we know that Iran has been accepting stablecoins for oil for some time now. It was the choice of yuan that intrigued me – China has been using its currency to pay for imports from the region, but that growing trend has been quiet. Now, Iran is advertising it to the world.

What pushed me to think more about the stablecoin angle was a post on the Hegemoney newsletter (cool name, a new discovery for me and a strong recommend). Author Jess Hoversen makes two key points: one is that we should be able to apply onchain forensics to estimate the volumes being channelled via this method, whereas with yuan bank payments, we won’t.

Another is that the stablecoins in question will almost certainly be in dollars, indirectly perpetuating the US currency hegemony.

This hints at why the US so far seems ok with the plan – at least, I haven’t seen any all-caps outbursts on this particular topic. Increased use of stablecoins not only keeps the dollar front-of-mind, it also supports demand for US treasuries.

But there’s a potential twist on the horizon.

Hong Kong was supposed to grant its first stablecoin licenses by the end of March – in keeping with the region’s conservative approach, these reportedly were going to two global banks: Standard Chartered and HSBC.

The deadline came and went, which is weird. But consensus seems to be that the delay is administrative. When the licenses are issued and the banks start minting stablecoins, these will reportedly be in Hong Kong dollars. They are unlikely to make any dent in Iran’s use of US dollar stablecoins, and not only because neither Standard Chartered nor HSBC will be able to work with Iran given the current sanctions, but also because Hong Kong dollar stablecoins will at first be much less liquid than their US counterparts and therefore less easily convertible into fiat currency.

Then again, there’s the digital yuan, which is heading into territory that is stablecoin-ish – not distributed by the central bank directly, unlike most CBDC models, but via commercial banks into customer accounts. That sounds similar to what HSBC and Standard Chartered will probably end up issuing.

And maybe the sources talking to journalists say “stablecoins” when they mean “digital currency”, which does not necessarily translate into dollar demand.

It would tie in with China’s drive to both carefully internationalize the yuan and promote use of the e-CNY. It would also make sense from a trade perspective – if Iran has more yuan income, it will spend more on Chinese imports which could be considerable when the war is over and reconstruction begins.

I’m just musing here, and Iran’s use of US dollar stablecoins has precedent and makes sense, especially for shippers that don’t have yuan accounts. But perhaps the situation is even more fluid than we realize and the china cupboard door (ha!) is starting to open, to admit even greater use of the yuan in offchain and onchain format. And in the process, further drive a wedge into the global payments order, offering all traders a choice. How much further can the cupboard door open without a plate or two falling to the ground?

Markets: thick confusion

As the war enters its sixth week, missiles keep flying, drones keep attacking.

President Trump’s prime-time address on Wednesday delivered no news and no clarity on the US plans.

In his speech, Trump did reassure everyone that Iran has “no anti-aircraft equipment” and that “their radar is 100% annihilated”, so we’re left wondering how they managed to shoot down a US F-15E fighter jet over Iranian territory just over a day later. One pilot was rescued almost immediately, the second 24 hours later after what reports are calling a shoot-out between US and Iran forces.

Not long after the F-15E went down, a US A-10 Warthog – a low-altitude, low speed combat support plane – crashed in the Persian Gulf near the Strait of Hormuz, with Iran claiming credit. The pilot was safely recovered.

Another public address from Trump is scheduled for 1pm ET today. Like Wednesday’s broadcast, this will also probably offer no new information, but will be an opportunity to brag about military superiority and the daring rescue. (I’m not a military expert and am very relieved the men were found, but the story does feel weird.)

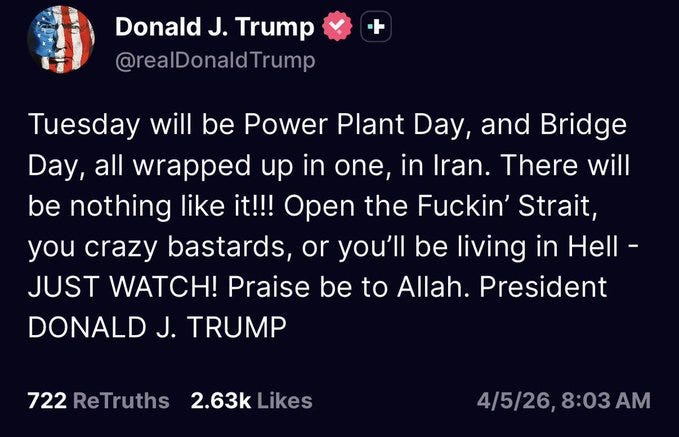

Meanwhile, the messaging confusion intensifies. On Wednesday, Trump said that Iran had asked for a ceasefire – Iran denied this. On Friday, he threatened to blow up bridges and power plants. On Saturday, he reminded the world that the deadline on his threat to blow up Iran was expiring in 48 hours. On Sunday, he posted this:

(screengrab via @LukeGromen)

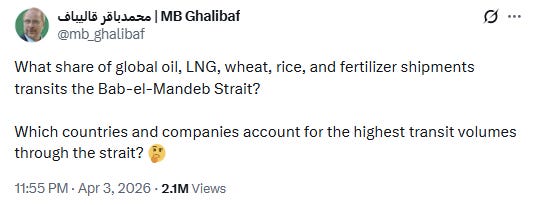

Later yesterday, he appeared to extend the deadline to Tuesday night, while Iran continues to reject the idea of a ceasefire. And the speaker of the Iranian Parliament is out there on X asking what share of global commodities flow through the Bab el-Mandeb Strait to the south, and towards which regions.

(post by @mb_ghalibaf)

Markets seem as confused as we are, with Asia posting mixed trading today, European markets all over the place, and futures pointing to a neutral US open.

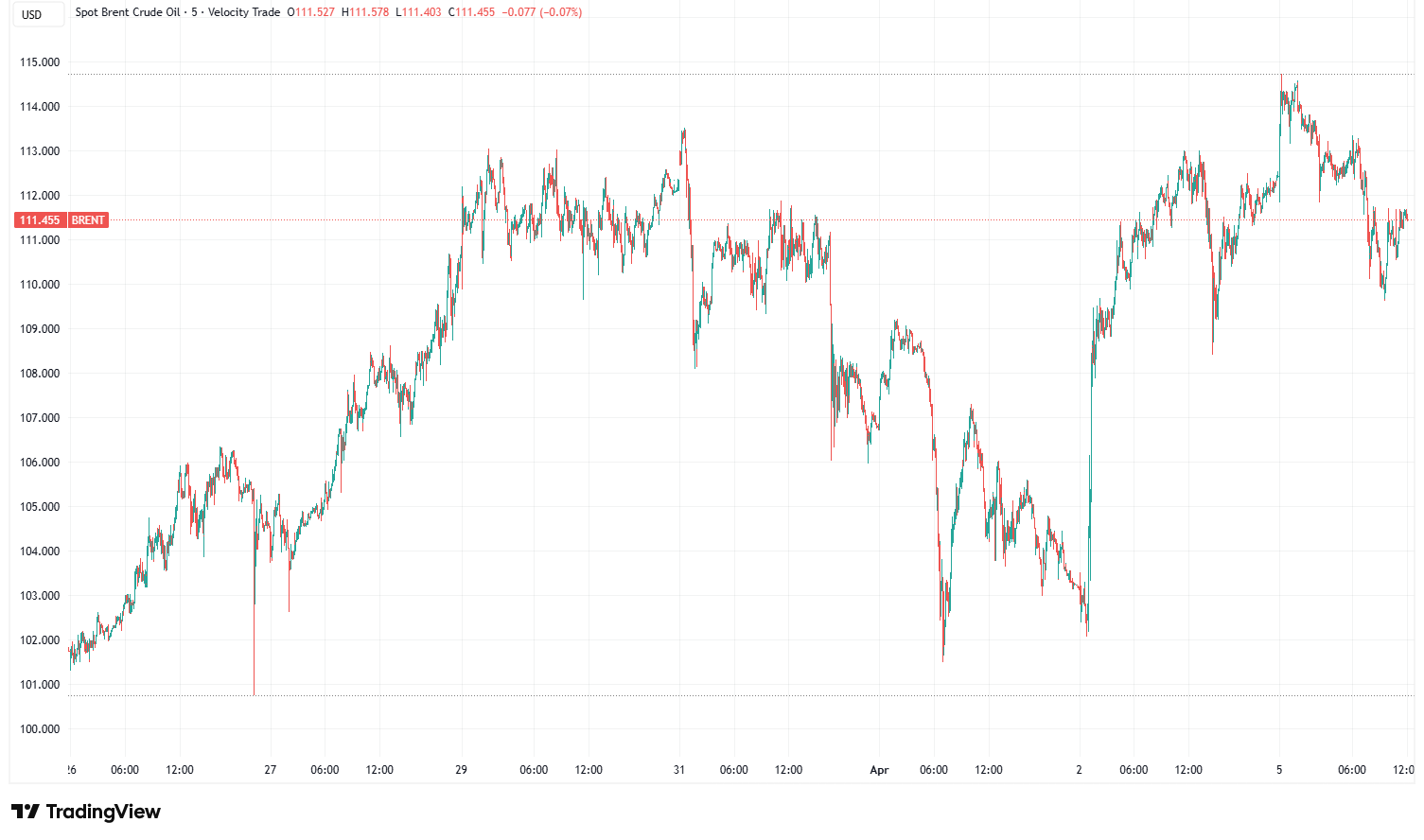

After the disappointment of Trump’s Wednesday speech, the price of Brent spot crude jumped from $102 to $108 and continued higher on the disappointment. It doesn’t feel like the market will be so ready to trust talk of ceasefires going forward.

(chart via TradingView)

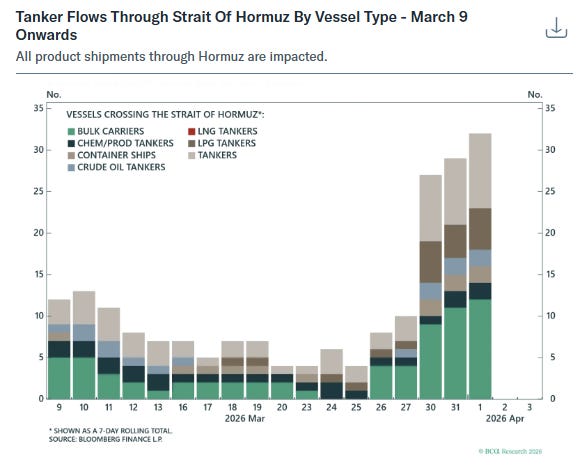

More ships are getting through the Strait of Hormuz, at Iran’s discretion. This is encouraging, but doesn’t do much to change the short-term shortage scenario as the number is still barely a blip compared to traffic a couple of months ago.

(chart via BCA Research)

The EU’s energy commissioner is warning of a long crisis, and that the bloc is assessing fuel rationing and strategic reserve releases. And Italy is introducing jet fuel restrictions in some secondary airports.

It’s possible that spreading acceptance of the looming supply crisis is buoying Bitcoin sentiment, in the hopes that market intervention will re-ignite risk sentiment. Last night, just before the Asian open, the BTC price started climbing and earlier this morning briefly pushed above $70,000. This still feels speculative, however, and there are few signs of longer-term buyers accumulating in size just yet.

(chart via TradingView)

Macro: US jobs

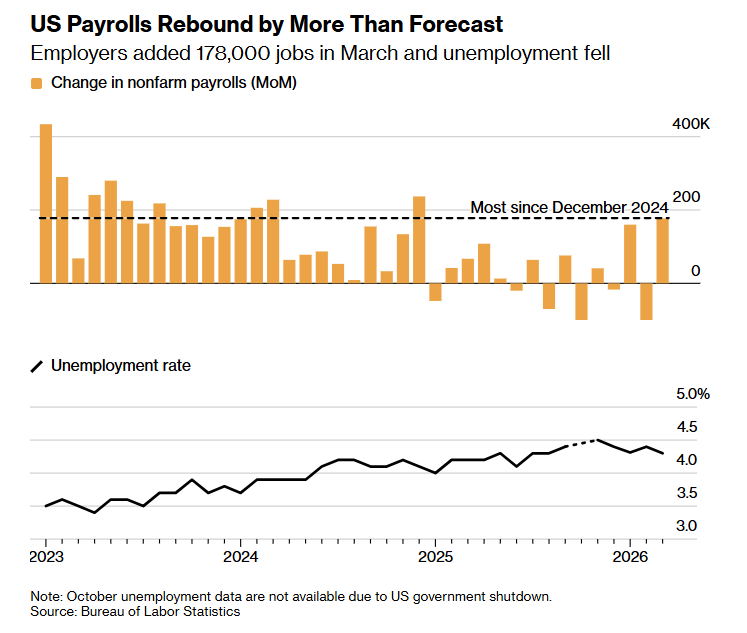

Friday’s US payrolls report pretty much put any lingering rate cut expectations in the back of the cupboard as the gain for March came in at 178,000, much higher than the consensus forecast of 60,000, and than February’s 133,000 contraction (revised down from a contraction of 92,000). This was the highest increase since the end of 2024.

The unemployment rate also did better than expected, dropping from 4.4% to below 4.3%, the lowest since last June.

(chart via Bloomberg)

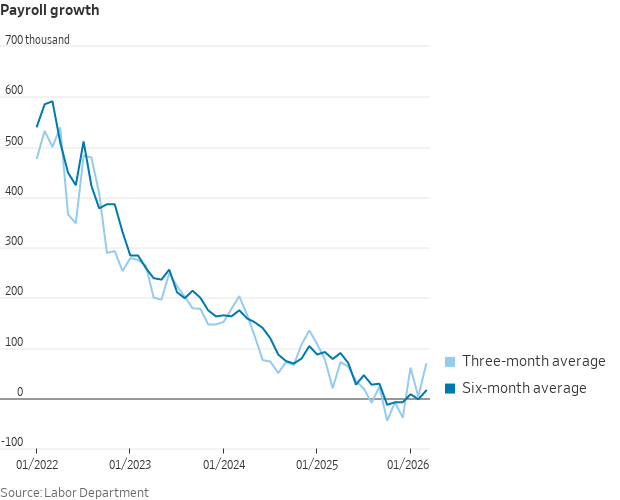

Good news. But, check out the volatility in the payroll numbers over the past year – it’s weird to see them swing positive and negative like that. We’re left with the feeling that either we’re in a volatile economy (not a good feeling), or that something is very wrong with the data collection.

Still, even smoothing with averages shows an uptrend.

(chart via @NickTimiraos)

US markets were closed on Friday, so we can’t glean anything from their reaction – and anyway, there’s so much going on at the moment, it would be challenging to discern any cause-and-effect.

🎶 WHAT I’M LISTENING TO: This one is impossible to describe – orchestral, soaring, original, moving, poetic, catchy – Click Clack Symphony, by RAYE and Hans Zimmer 🎶

If you find Crypto is Macro Now useful, would you mind hitting the like button? ❤ I’m told it feeds the almighty algorithm.

And if your friends and colleagues sign up via your referral link, you get a free month!

BE CAREFUL OUT THERE!

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google (always double-checking facts), but never for writing.