Just how “digital” is Bitcoin?

plus: market whiplash, US CPI, Mythos, what's ahead this week and more

“Every solution of a problem raises new unsolved problems.” – Karl Popper ||

Hello everyone! I hope you all had a good weekend and stayed away from screens as much as possible.

🎥 Later today, I’m chatting with Maggie Lake on her The Market House show – we kick off at 4pm ET, come join us! You can tune in on Substack, or via her YouTube channel. 🎥

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

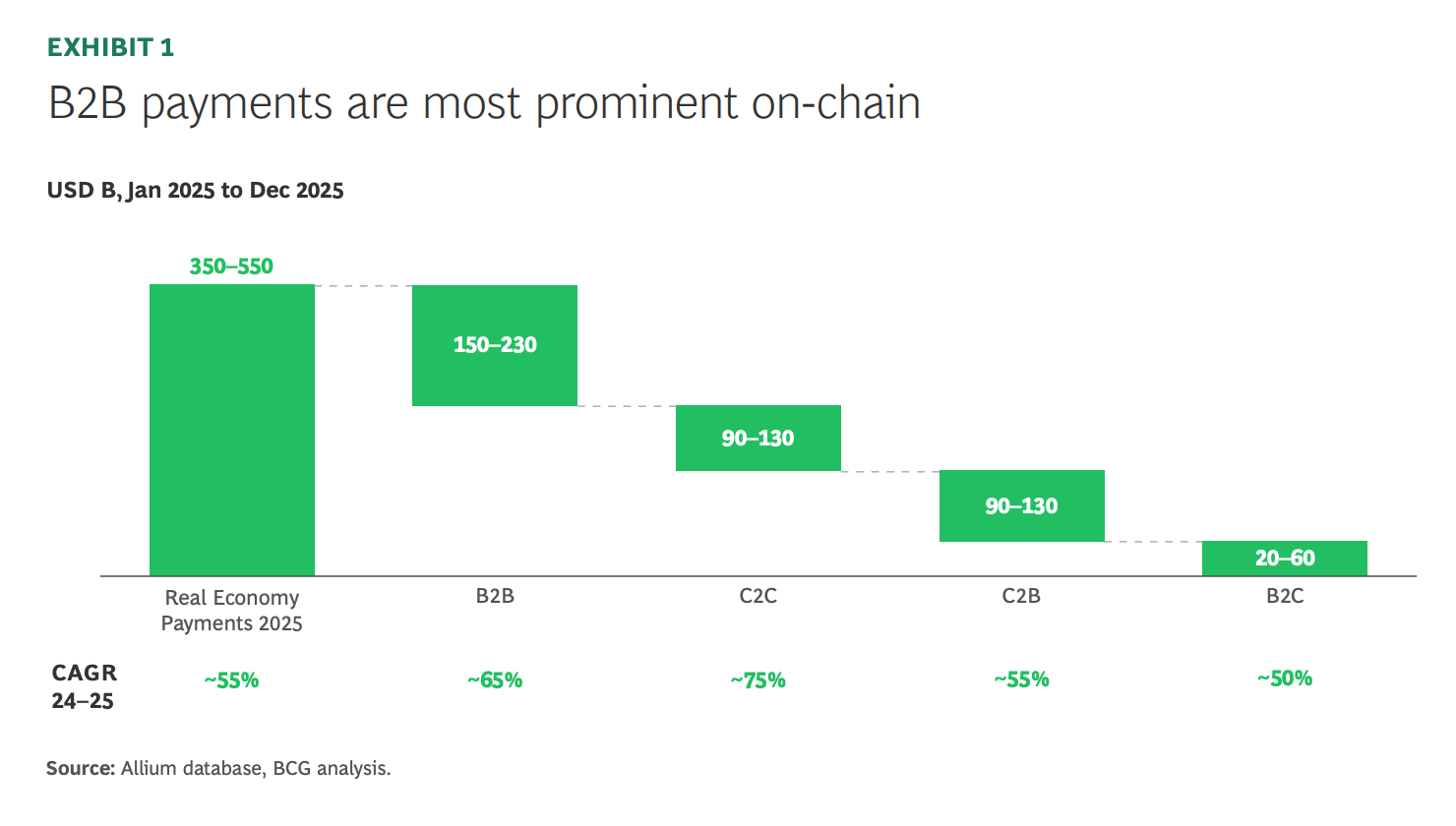

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

Coming up this week: inflation, forecasts, earnings

Definitions: Mythos

Monday mood: Just how “digital” is Bitcoin?

Markets: a whiplash of a weekend

Macro: US CPI

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

✨ Press Publish with Christine Kim

So, I did it! On Friday I launched a Substack live series 🎥 – not on crypto nor macro (coming soon!), but on writing newsletters.

There’s no-one I’d rather have kicked this off with than my friend and former colleague Christine Kim, one of the leading experts on the Ethereum ecosystem, now also covering Bitcoin (you can check out her prolific output here).

If you missed the livestream, you can still learn from Christine’s experience and courage here:

✨NEXT UP: 🎥

Come join me next Friday, April 17th, at 11am ET when I talk to Brady Dale, who recently left a high-profile newsletter writing gig at Axios to branch out on his own – we’ll dive into why, how self-production is different, what advice he’d give anyone thinking of doing the same, where media is going, and more.

(Some of you may have gotten an invite when I scheduled the session earlier today, and I got the date wrong, sorry – still getting the hang of this – 🎥 it’s on the 17th 🎥, not the 18th.)

Coming up this week: inflation, forecasts, earnings

On Monday, the 2026 Spring Meetings of the International Monetary Fund and World Bank kick off in Washington DC, with global policymakers and economists gathering until Saturday.

This will be the second one in a row in which attendees and policymakers grapple with the familiar geoeconomic pieces up in the air – last year it was tariffs and their impact on global trade, this year it’s the impact on global trade supply issues stemming from the conflict in the Middle East.

Also on Monday, Goldman Sachs kicks off Q1 earnings season. This week will be heavy on numbers from the big banks – I’ll be paying more attention to what the CEOs are saying in the earnings calls, as banks tend to have a unique insight into business activity.

On Tuesday, we get the IMF’s updated economic forecasts along with a report on global financial stability.

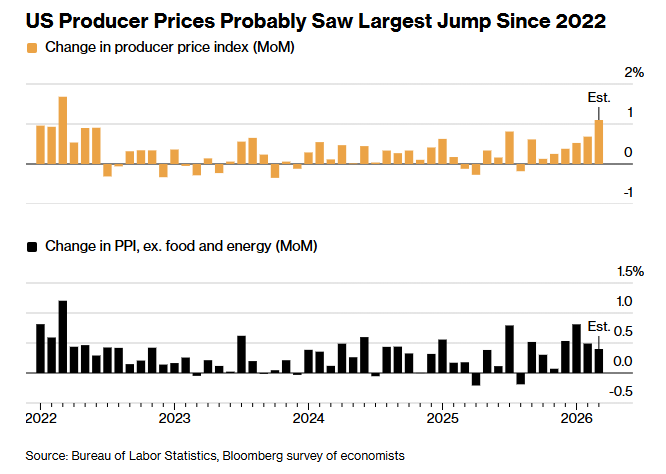

Also on Tuesday, we get the US Producer Price Index (PPI) for March, the first post-Iran war read on wholesale inflation. The headline index is expected to show a whopping month-on-month increase of 1.1%, the highest since March 2022 – back then, the fed funds rate was around 0.3% (vs today’s 3.6%). The core index is expected to increase by 0.4%, a deceleration relative to last month’s 0.5%, but still notably higher than the 12-month average.

(chart via Bloomberg)

On Wednesday, it’s the turn of March US import and export price indices, with both expected to show a sharp acceleration on a year-on-year basis.

And we get the Fed’s Beige Book, with anecdotal accounts of what the regional central banks are hearing from local businesses.

Also, Wednesday is the US tax filing deadline, which often comes with portfolio changes and possible market volatility as investors sell assets to meet capital gains liabilities.

On Thursday, China releases its Q1 GDP report, forecast to show annual growth accelerating from 4.5% to 4.8%. Growth in Chinese retail sales for March is expected to decelerate from 2.8% to 2.3%. And China’s unemployment rate is forecast to drop from 5.3% to 5.2%.

Also on Thursday, we get US industrial production for March, forecast to accelerate from 1.4% year-on-year to 1.8%. Manufacturing output is expected to accelerate from 1.3% year-on-year to 2.0%.

Term of the day: Mythos

Mythos is the name given to Anthropic’s latest AI model, the first to trigger emergency meetings at the highest levels of financial oversight – over the weekend, both US Treasury Secretary Scott Bessent and Federal Reserve Chair Jerome Powell met with the heads of large US banks to discuss the Mythos threat. It turns out that the latest model can detect and autonomously exploit vulnerabilities in the operating systems that support most corporations and financial institutions. Unusually but sensibly, Anthropic has decided to not release Mythos to the public – but that doesn’t mean similar models won’t emerge elsewhere.

Monday mood: Just how “digital” is Bitcoin?

(what’s on my mind as we head into the week)

Many pixels have been spilled about the performance of BTC since the war began, some of them in this newsletter: the surprising resilience, the lack of volatility, the quiet derivatives market, the vulnerability to a sharp stock market adjustment. But, to be honest, I’m not giving much thought to where the price goes in the short-term – there’s no point as war tends to mask fundamental trends with decibels of noise.

I’m much more interested in what’s next, and how that will shape and be shaped by our understanding of networks. This is changing more than most realize. While we’re distracted by explosions and commodity prices and global choke points and off-the-rails social media diplomacy, our collective perception of the digital and physical planes of the global economy has been shifting.

For most of this century, we’ve assumed the world was going digital. Finance, money, entertainment, even relationships => digital, “flat”, connected.

Those of us that rearchitected our careers and lives around this felt like we were ahead of the curve, creating the future, more forward-thinking than those stuck in analog ways.

We could argue about when the cracks in this worldview started to show. It could have been COVID, when we realized we didn’t want everything to be digital, remote, isolated. It could be the Russian invasion of Ukraine, giving most of us in the West our first bitter taste of kinetic war on our doorstep. I think the hostility of the previous Administration to a new emerging form of digital finance played a part, lifting the veil on the imperative and the cost of centralized control. The election of Donald Trump as President of the US, both times, can be seen as a big middle finger to the “connected” layer. And now, we have the mother of all supply shocks in energy and its derivatives headed our way.

Plus, we sent people into space, and they came back safely. That’s a triumph of atoms over bits if ever I saw one, and there’s something about seeing our planet through the eyes of people floating hundreds of thousands of kilometres above it that drives home the perfect geometry of where we live.

It feels like there’s a subtle shift in the overall vibe away from digital and towards physical, away from a conviction that atoms will matter less and less, and towards a realization that they’ll matter more.

We’re seeing it in markets as well. Indices of semiconductor manufacturers have significantly outperformed those of internet services over pretty much any recent time period. Meta went all-in on the metaverse but is now scaling back. The once-hot NFT market has been quiet for years. Mythos (see above) is driving home how software is vulnerable. Now, when I hear the term “tech company”, I think of robotics before platforms.

And those who have been insisting AI will bring “abundance” are sounding less confident today as datacentre buildout runs into the wall of energy and hardware scarcity.

So, if indeed we are moving into a rediscovered appreciation for “stuff”, where does that leave the long-term outlook for Bitcoin, which is undeniably and exclusively digital?

A caveat before I sketch out why Bitcoin both is and isn’t: this is not a well-thought-out thesis yet, this is just my off-the-cuff Monday musing where I riff on what I’m thinking about. Feedback and pushback are welcome.

With that out of the way, here goes:

I think this is where Bitcoin starts to break away from the “digital finance” pack. For decades, electronic networks have fed the financialization of the global economy as new investment and leveraged products emerge faster and faster to keep up with the speed of database dollars. The need to maintain these networks led to greater centralization of control, which in turn facilitated compliance-mandated gating, exclusion and more control.

Along comes Bitcoin, a new type of network that breaks the paradigm of centralized control and offers up a new type of asset that defies categorization.

But habit dies hard, especially when there are economic incentives to keep it going. And so Bitcoin became a “risk asset” or “digital gold” or whatever term helps traditional investors put it into a familiar bucket while “digital finance” gets to work doing its packaging thing.

Even those who chose to focus on Bitcoin’s unique properties stressed how it brought direct ownership and property rights (physical!) into the digital realm. The “digital” was always the dominant layer.

But what if we started to look at Bitcoin the other way around? Less as provable scarcity on a digital network, and more as digital convenience layered onto a scarce asset?

These two approaches may sound exactly the same, but they’re not: the emphasis is different in each.

If I’m right and the zeitgeist is changing, “digital” will become less dominant as a narrative, more a powerful layer of convenience than a reason for being unto itself. Here is where Bitcoin can shine relative to other “digital-first” assets that exist because of their convenience and the networked service they provide. Not only is Bitcoin the only provably scarce asset with hard property rights and no centralized control that can move on digital networks. It’s also one of the very few digital assets that does not need permission to exist but that does anyway – by “digital asset”, I mean any asset that exists digitally, on any electronic network, not just in crypto.

Most digital assets were created to do something. Bitcoin just is. It exists in that limbo between physical and digital, bringing properties of each to the other.

And in a world moving towards appreciating scarcity and protection over convenience and speed, this will come to matter more.