Kraken, the Fed and the new payments landscape

plus: stablecoin payments, US jobs, inflation pressures and more

“In all affairs it’s a healthy thing now and then to hang a question mark on the things you have long taken for granted.” – Bertrand Russell ||

Hi everyone! I hope you’re all doing well. Nice to see Bitcoin rallying. If only it were under happier circumstances.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

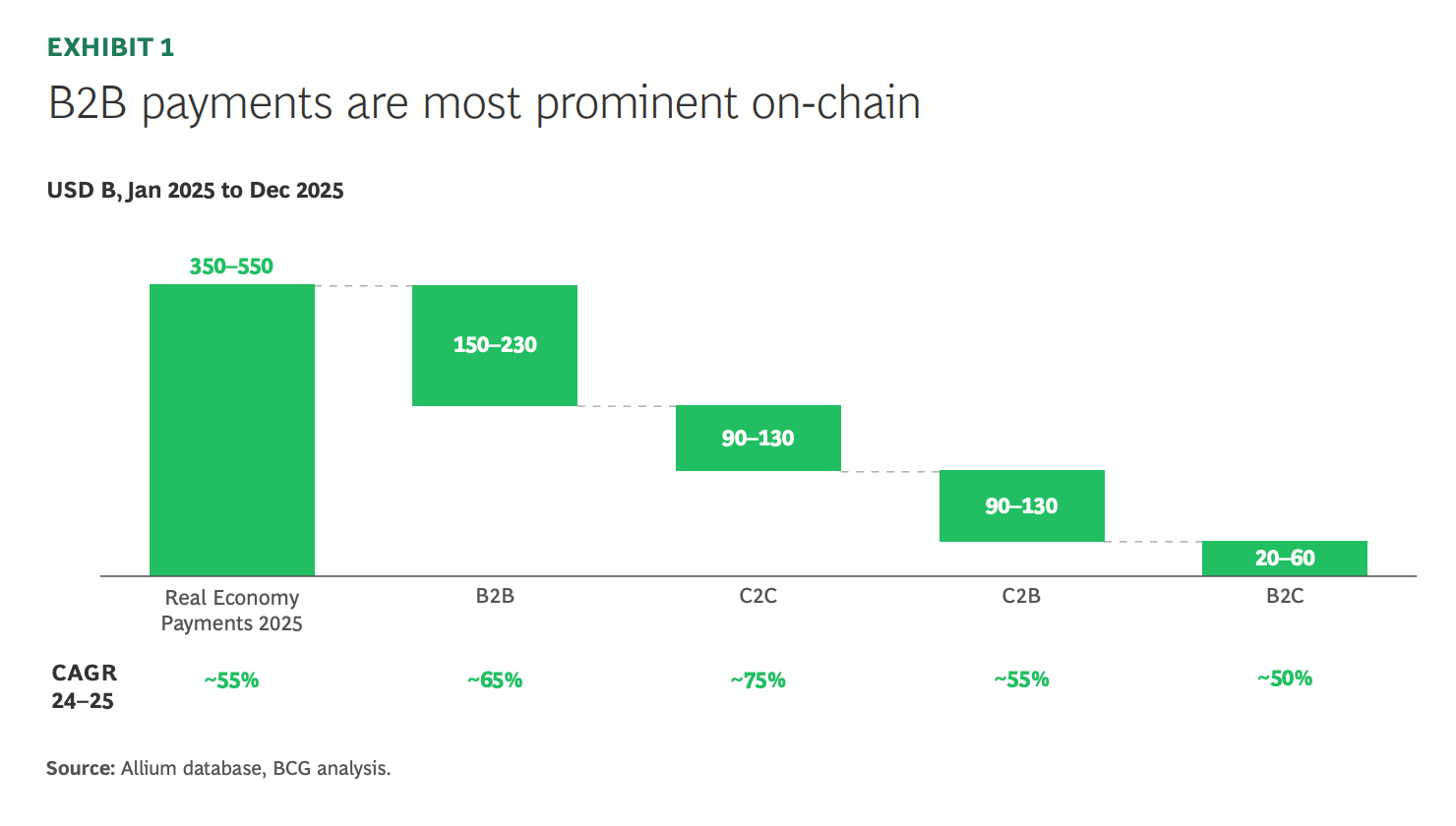

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Kraken, the Fed and the new payments landscape

Stablecoin payments: some surprising details

Macro: US jobs

Macro: US services activity

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

Kraken, the Fed and the new payments landscape

Yet another seemingly tentative regulatory move that masks a huge step towards a new financial system:

Kraken Financial, a Wyoming-chartered bank owned by crypto platform Kraken, has been granted the first Federal Reserve master account awarded to a digital asset bank.

This will enable it to hold reserves at the US central bank and connect directly to core US payment rails without relying on intermediary banks.

The move is temporary for now, granted for a period of one year, and comes with limitations: Kraken can’t earn interest on its Fed balance, nor will it get access to daylight overdraft privileges and overnight borrowing.

The big deal here is that Kraken gets access to bank-quality payment rails with the ultimate security of a central bank backstop, without being a traditional deposit-taking bank. Higher security means cheaper pools of settlement liquidity for stablecoin transfers.

Stepping back, this raises the question of why banks have monopolized top-level payment rails for so long. An obvious answer is that banks are where money is held, so it follows they would originate most payments.

Only, that’s not true anymore. Banks no longer have a monopoly on deposits – these are migrating away from the centre towards more agile fintech services, and towards stablecoin accounts. And banks have never had a monopoly on electronic payments – as far back as the late 19th century, Western Union was able to take advantage of bank’s reluctant attitude towards innovation.

Yet, until now, banks have had a monopoly on Fed access. Today’s payments landscape contains a dizzying array of non-bank digital services, in constant evolution. But virtually all electronic payments have to touch bank credit at some stage of their journey.

This may be “traditional”, but the institutional marriage between payments and credit introduces fragility.

Banks rely on intraday and overnight credit with each other for settlement. And history has shown that, at times of systemic stress due to loan defaults and collapsing credit structures, payment networks can freeze. Even outside a widespread banking crisis, issues with any one institution can create payments mayhem as network participants are reluctant to enter into even short-term settlement commitments.

Now, however, the Federal Reserve is contemplating opening the quality-payments door to institutions that don’t lend. At all.

Put differently, this is a move to separate the payments function of financial institutions from the lending function. Of course, if banks no longer control the payments system, they lose economic power – no wonder the lobbies are up in arms over this.

It’s a gutsy and insightful move from the top bank regulator, which will not only boost stablecoin liquidity and calm concerns about run risks; it will also move the US towards a financial network less reliant on bank lending and more reliant on government debt.

In case any of you are thinking that the one-year timeframe means the Fed is not serious about this move, let’s remember Governor Chris Waller has been talking about the idea of “Skinny Fed Master Accounts” for some time. And that the Bank of England has proposed something similar: allowing “systemic” stablecoin issuers central bank access. I doubt this is a coincidence.

The approval of the Kraken master account is no doubt the first of several – keep an eye out for similar recognition of Anchorage and Custodia’s applications, there are probably others out there I’ve lost track of.

Bottom line, the structure of global payments is changing, and stablecoins are a key part of the redesign. And it feels like the shift is accelerating.

See also:

Crypto: a win for liquidity (Feb 2026)

Stablecoin payments: some surprising details

Whatever you thought you understood about stablecoin payments, a new report is out that will probably change some of your assumptions. Compiled and written by Allium (sponsors of this newsletter, but that’s not why I’m highlighting it), the report breaks down stablecoin use case, geographies, networks and volumes, with several surprises.

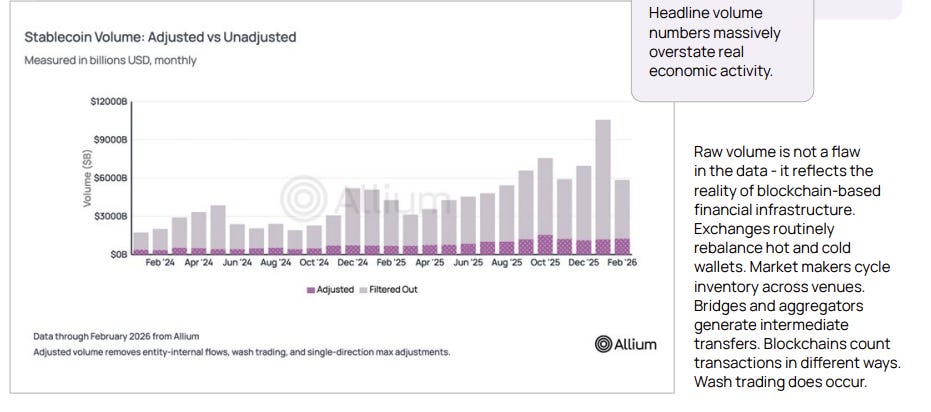

One is just how much work is needed to tidy up blockchain data. Anyone can see aggregate moves of onchain assets, but the raw data does not discriminate between useful (transfers between entities) and irrelevant (transfers between addresses held by the same entity) information. However, pattern parsing, label heuristics and rigorous filtering can extract the economically significant transactions.

(all charts in this section by Allium)

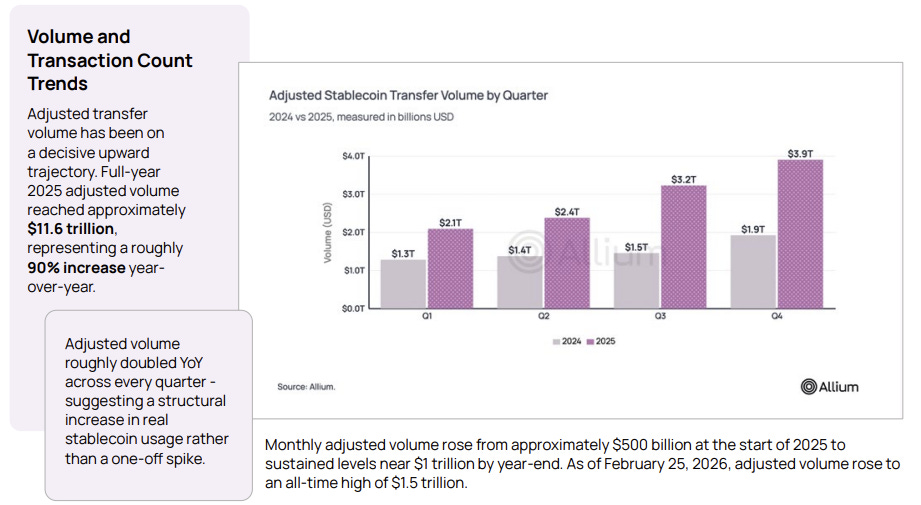

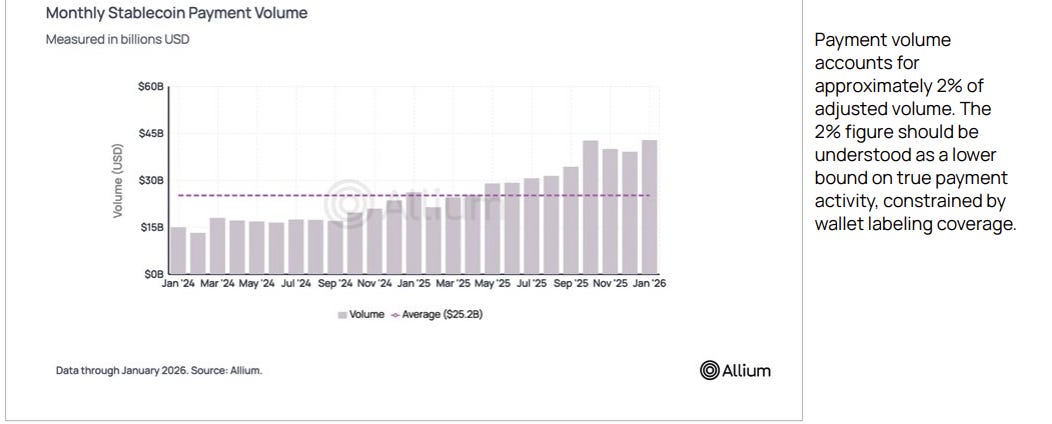

This filtering shows almost 90% growth in “real” stablecoin activity (adjusted monthly transfer volume) over the past year

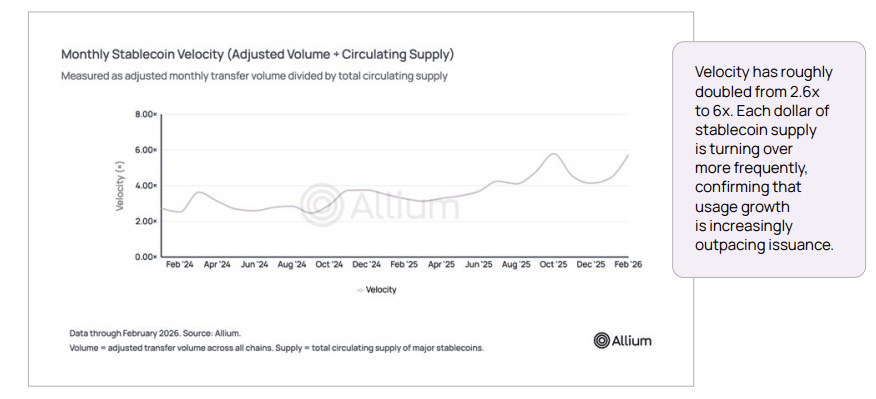

Comparing the growth in adjusted transfer volume growth to that of circulating supply, we see that velocity (the number of times each stablecoin moves in a given month) is increasing, suggesting a deepening utility.

Further filtering shows that the volume of stablecoin transfers for payments is around 2% of the total, with the rest presumably for crypto trading settlement. What’s more, this segment has shown persistent growth over the past couple of years, reinforcing the deepening utility.

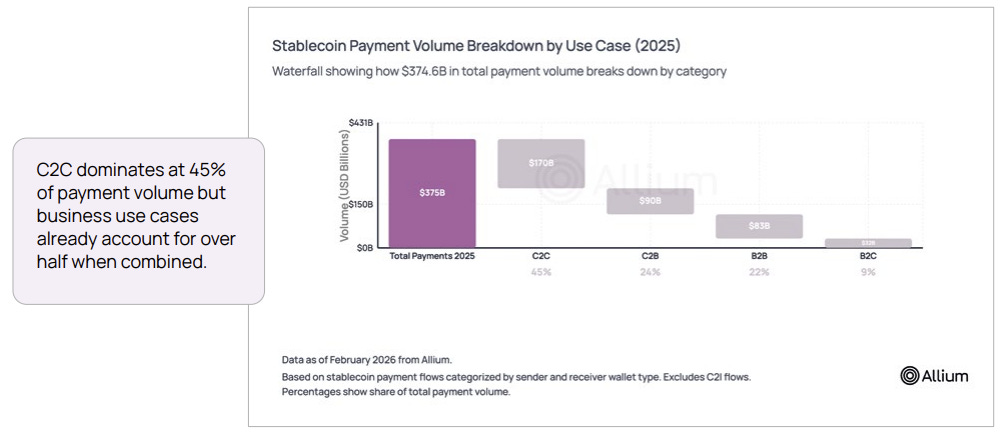

This data can be further filtered into payment categories: surprisingly, consumer-to-consumer (C2C) transfers account for the largest channel, up 53% last year – I would have thought it would be business-to-business (B2B) for cross-border commerce. That category came in third, but still up 87% in 2025. Interesting to see that consumer-to-business (C2B) stablecoin payments jumped over 130% last year.

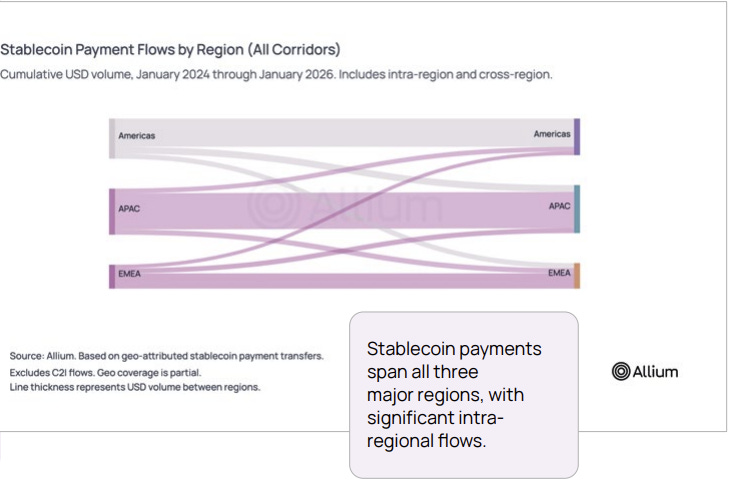

Another big surprise: stablecoin payments are not mainly for cross-border activity. There’s some of that, but most transfers (over 80%) stay local, with the APAC region accounting for the most volume. What’s more, cross-border flows have declined as a percentage of the total, from 44% at the start of 2024 to just over 25% at the end of 2025. This further confirms a deepening of utility.

The report contains many, many more insights than I can share here – it’s worth a read. My big takeaway is the profile of those using stablecoins for payments is more complex than most realize: it’s not just about cross-border, and it’s not just about B2B. What’s more, different users will have different reasons for preferring stablecoins over traditional payment rails, and we will see these reasons continue to evolve as services mature and diversify.