Manipulation and the Chat Control lever

plus: what's ahead this week, how the EU works, and more

“He who marvels at the beauty of the world in summer will find equal cause for wonder and admiration in winter.” – John Burroughs ||

Hello everyone! I hope you all had a great weekend and are ready for a big macro week.

✨ Monetary Forces: tomorrow, Izabella Kaminska and I pick at the key headlines that paint the picture of how technology is changing finance, and I’ll talk about how stablecoins increase the money supply. Come join us!

Tuesday, July 14 @ 10am EST / 4pm CEST / 3pm BST – livestream link: https://open.substack.com/live-stream/275514

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

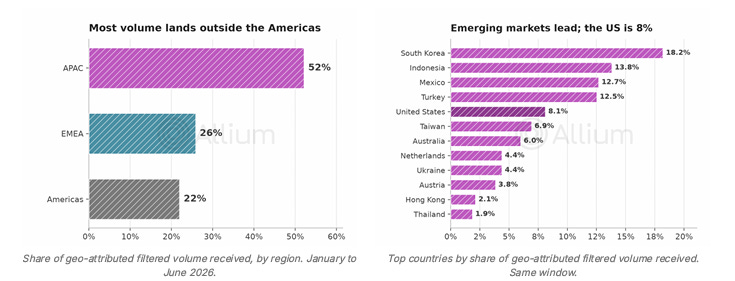

Where are stablecoins most used?

Allium filters stablecoin volumes for non-economic actions such as inter-group transfers – it turns out that most of this economic activity is outside the US, with 52% in Asia-Pacific and 26% in Europe, the Middle East and Africa.

The leading destinations are South Korea, Indonesia, Mexico and Turkey, places with currency pressure, active remittance corridors, or both.

→ For more, download Allium’s State of Onchain Finance report: https://allium.so/reports/state-of-onchain-finance-q2-26

IN THIS NEWSLETTER

Coming up this week: US macro, Fed speeches

Monday musings: manipulation and the Chat Control lever

Term of the day: Directive vs regulation

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you so much!! ❤

WHAT I’M WATCHING:

Coming up this week:

A packed week for macro data and Fed speeches – I counted 13 public appearances from US central bank officials over the next five days, including Warsh’s testimony.

Earlier, the two-day WebX 2026 blockchain event in Tokyo kicked off with an address from Japan’s Prime Minister Sanae Takaichi, and the first day closed with a keynote from Japan’s Finance Minister Satsuki Katayama. There were also keynotes from Japan’s Minister of the Economy, Trade and Industry, and the Minister for Digital Transformation and Cybersecurity as well as panel participation from high-level executives from big global and Asian banks, energy companies and market infrastructure providers. According to reports, it has attracted around 15,000 attendees, which would make it one of the largest Asian crypto events of the year.

Also today, OPEC publishes its monthly oil report.

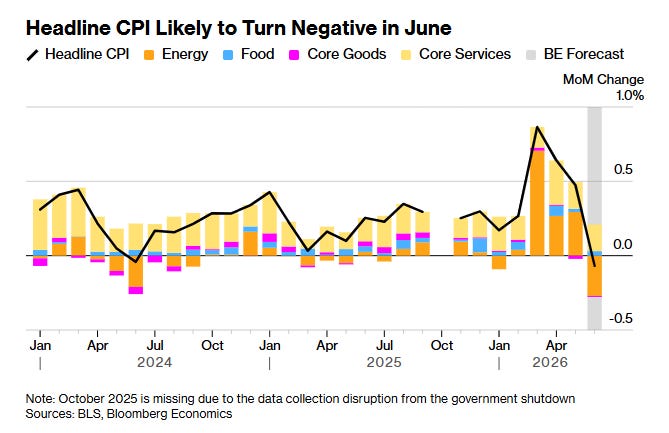

On Tuesday, we get the US CPI data for June. Consensus expectations point to the first month-on-month decline in the headline index since 2020, largely due to the drop in the oil price. The year-on-year increase is forecast to slow from 4.2% to 3.8%. The increase in the core index, ex-food and energy, is expected to hold steady for June at 0.2% month-on-month and 2.9% year-on-year.

(chart via Bloomberg)

On Tuesday at 10am EST, Kevin Warsh makes his first appearance before Congress as Federal Reserve Chair in what will be two days of gruelling testimony. First the House Financial Services Committee and then the Senate Banking, Housing, and Urban Affairs Committee) will no doubt try again and again to tease out some forward guidance, which he is unlikely to give.

We also get China trade data, with exports expected to show a slight deceleration in year-on-year growth, but to still impressive levels.

The US kicks off Q2 earnings season, with results from JPMorgan, Wells Fargo, Bank of America, Citigroup and Goldman Sachs – I have never been happier to not be a banking analyst, that sounds exhausting.

And, even more important, Spain plays France in the World Cup semifinals.

On Wednesday, we get the US Producer Price Index (PPI) data for June: as with the CPI, the drop in energy prices should drag the month-on-month growth into negative territory, while the year-on-year increase slows from 6.5% to 6.2%. Core PPI, ex-food and energy, is forecast to have decelerated slightly to 0.3%, but the year-on-year increase is expected to accelerate from 4.9% to 5.2%.

We also get some key China data: consensus forecasts suggest the annualized growth in Q2 GDP has decelerated from 5.0% to 4.5%; June industrial production year-on-year growth is expected to have accelerated slightly to 4.6%; June retail sales are forecast to have declined year-on-year by 0.1%, less than May’s 0.6% year-on-year decline.

The Federal Reserve publishes its Beige Book, which takes the business temperature through interviews with businesses in each Fed region.

And Morgan Stanley, BlackRock, BNY, ASML and others report earnings.

Thursday brings US retail sales for June, forecast to show a notable month-on-month slowdown from 0.9% to 0.2%

Netflix, State Street, US Bancorp and others report earnings.

On Friday, we get US import and export prices for June (the year-on-year growth in May was 6.7% and 11.2%, respectively), as well as industrial production, expected to show some acceleration.

And, we get the preliminary July consumer survey report from the University of Michigan.

Monday musings: manipulation and the Chat Control lever

(what’s on my mind as we head into the week)

Social media manipulation can come from unexpected directions.