Meme coins and the crypto blues

plus: what’s ahead this week, rates outlook, GDP rumblings and more

“There comes a time to join the side you’re on.” – Midge Decter ||

Hello everyone! I hope you got to disconnect this weekend. I spent part of yesterday walking around wide-eyed at an urban art festival in the Malasaña neighbourhood of my home city of Madrid – doors and walls and roller shutters and gates were brought to life in a riot of colour and creativity while we watched, just amazing.

Later today, I’m joining Scott Melker’s Macro Monday show, and I wonder if we’ll find anything to talk about 😏. We kick off at 9amEST/3pmCEST, and I think you’ll find the stream here – come join us!

And yesterday I was invited onto Asharq Business with Bloomberg to discuss crypto markets – with a live translator, of course. If any of you speak Arabic, here’s the clip.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

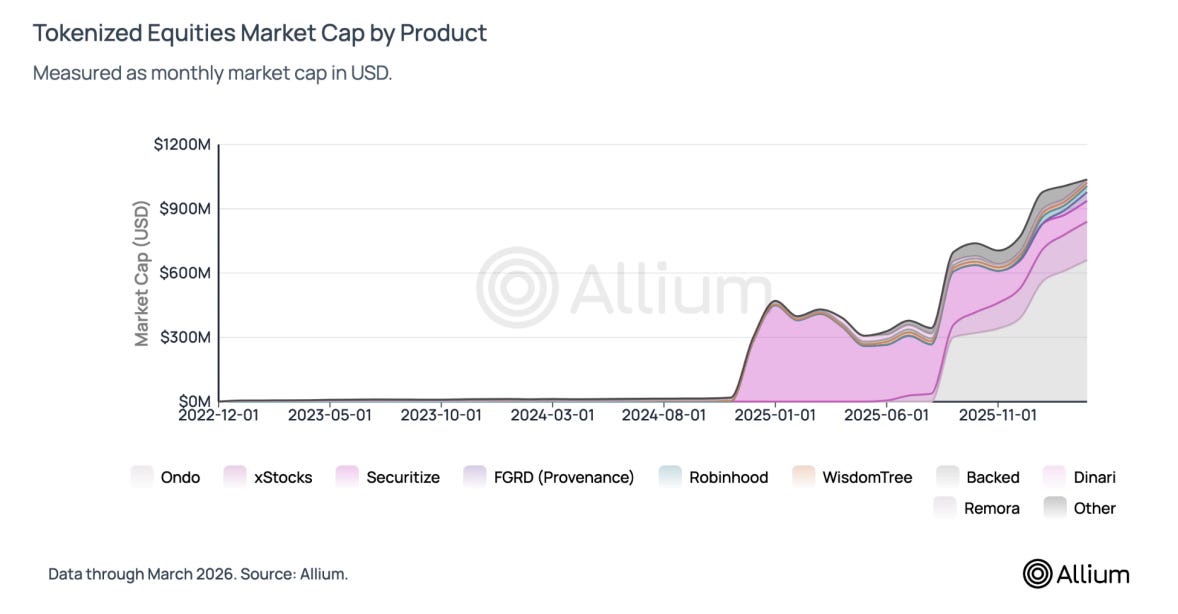

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

IN THIS NEWSLETTER

Coming up this week: central banks!

Monday mood: Meme coins and the crypto blues

Term of the day: meme coin

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

Coming up this week: central banks!

This week, all G7 central banks announce rate decisions, affecting the monetary policy of roughly half of the world’s economy. And, we get what will probably be Fed Chair Jerome Powell’s last press conference. Plus, some key economic data.

To kick off a central bank-heavy week, on Tuesday we get a decision on rates from the Bank of Japan, expected to hold steady for now.

We also get the latest report from the US Consumer Board consumer confidence survey, which is unlikely to deliver good news.

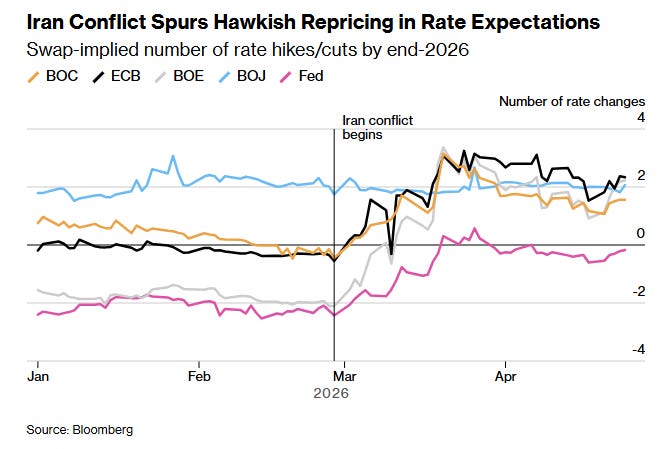

Wednesday gives us the official statement from the Federal Reserve’s rate setting committee (FOMC), also expected to hold steady given hints of inflationary pressures. Not that long ago, a rate cut at the April meeting was priced in as extremely likely – now, it looks like traders are expecting zero cuts this year.

(chart via Bloomberg)

Chair Jerome Powell’s press conference after the statement will no doubt feature some questions about the decision by the DOJ to close the investigation against him, leaving it instead to the Fed’s Office of Inspector General to get to the bottom of the refurbishment cost overruns. It would be uncharacteristic of him to say anything on this topic, but he surprised us by doing so at the last press conference, so who knows… We do want to know whether he plans to stay on as Fed governor once his term as Chair ends next month.

If the confirmation of Fed Chair nominee Kevin Warsh proceeds as expected, this will be Jerome Powell’s last appearance before the press corps in his current role. I have my frustrations with Powell, but he’s been great at the press conferences, I will miss him.

On Thursday, we get interest rate decisions from the European Central Bank and the Bank of England.

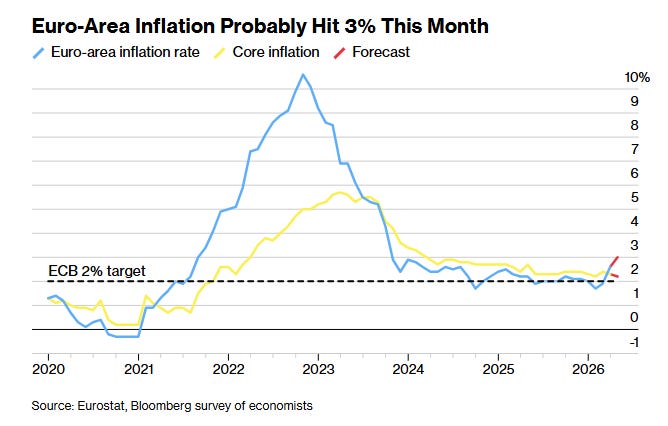

And between Wednesday and Thursday, we get a glimpse of the economic impact so far of the Iran War via the preliminary (“flash”) data for inflation and GDP from key European economies and the Eurozone as a whole. It’s not looking great.

(chart via Bloomberg)

Also on Thursday, we get the US Personal Consumption Expenditure data – the Fed’s preferred inflation gauge – with the headline index growth expected to show a year-on-year acceleration from 2.8% to 3.3%, which would be the highest since 2023. The core index ex-food and energy) is forecast to move from 3.0% to 3.1%, which would tie with January for the highest rate since early 2024. This is not in a direction the FOMC will be comfortable with.

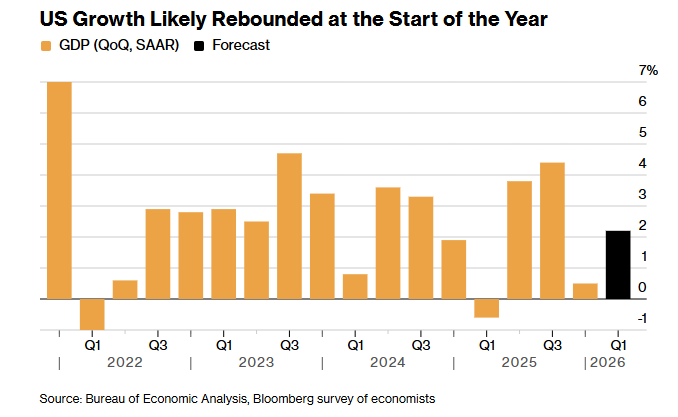

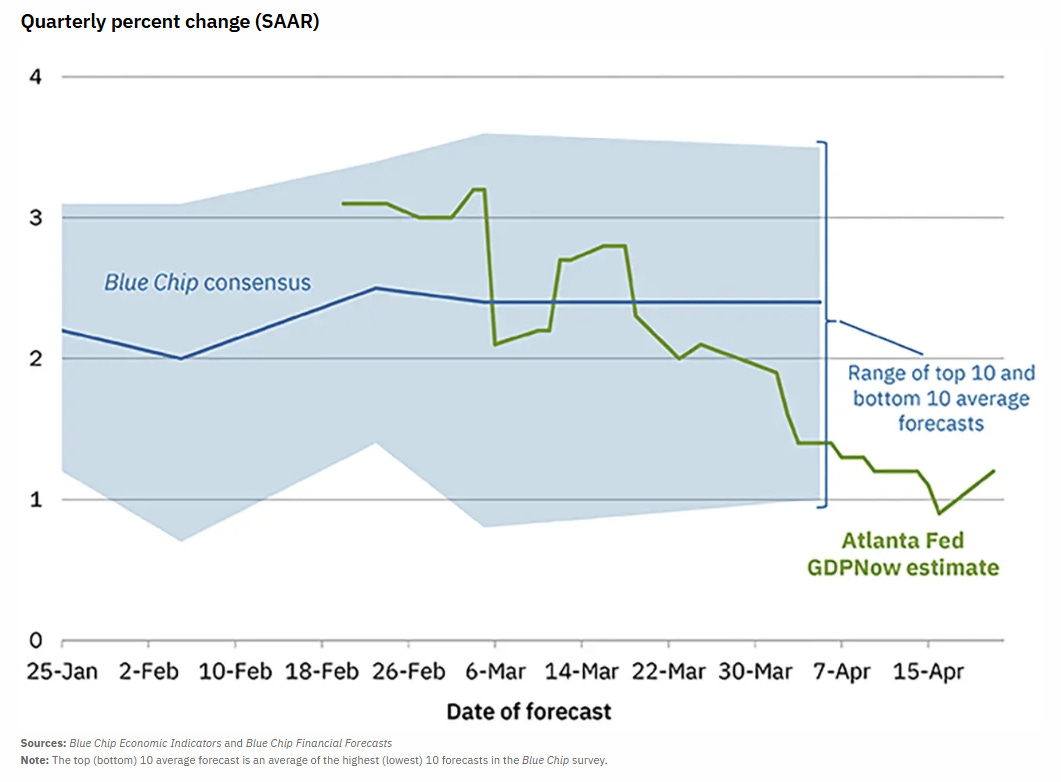

We get the preliminary read on US GDP growth. The consensus forecast according to Bloomberg has this accelerating from 0.5% quarter-on-quarter to 2.1%.

(chart via Bloomberg)

It’s worth pointing out that the Atlanta Fed’s GDPNow model points to Q1 GDP growth of only 1.2% - still above Q4 2025’s growth of 0.5%, but lower than economists predict.

(chart via Atlanta Fed)

Preliminary data on US real consumer spending for Q1 is expected to show a quarter-on-quarter acceleration from 1.9% to 2.6%.

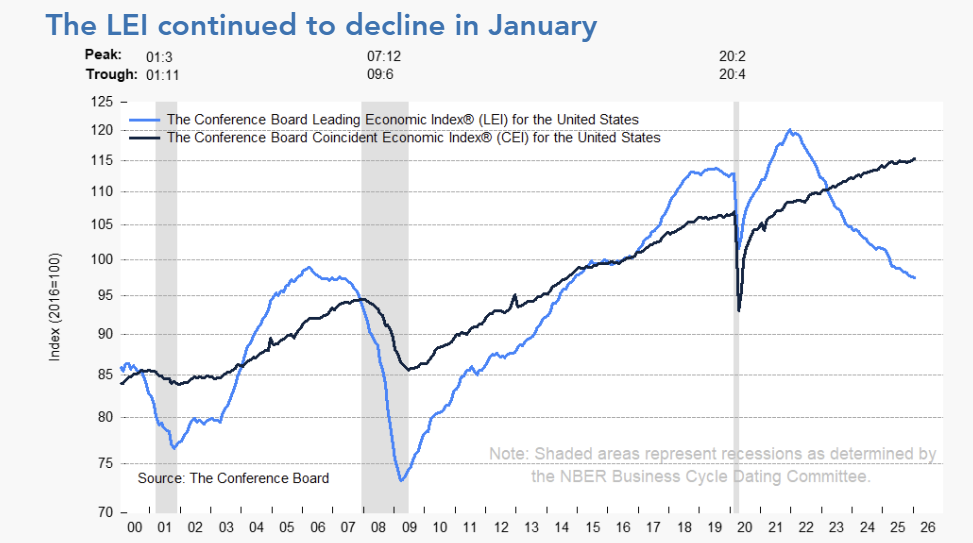

And (Thursday is quite the day!) we get the US Consumer Board’s leading index for February, which is still pre-war and therefore not affected by expectations of fuel and other commodity shortages. The level for January dropped 0.1%, while the coincident economic index continues to climb. Very strange.

(chart via the US Conference Board)

On Friday, we get the latest inflation figures from Japan, relevant for their interest rate outlook and therefore for the US bond market.

And, we get Institute of Supply Management data on US manufacturing activity. The overall Purchasing Managers Index is expected to show improvement, while the prices index is forecast to continue climbing.

Monday mood: Meme coins and the crypto blues

(what’s on my mind as we head into the week)

A high-profile event this weekend has inadvertently highlighted what I think is an overlooked explanation for the “crypto blues”, that jaded feeling of ennui that many long-time advocates have been struggling to put a finger on.

I’m not talking about the drama at the White House Correspondents’ Dinner. Rather, I want to focus on Trump’s meme coin lunch held at his Mar-a-Lago estate in Florida.

If that statement triggered an instinctive recoil, that’s part of the issue. Our distaste for meme coins is worth unpacking, as it’s not just about speculative tokens, nor is it just about blatant grift or influence abuse. There’s something else going on here.