Monday, Sept 16, 2024

real rates are not that high, BTC's cycle, SEC gaslighting, Sony's blockchain momentum, safety vs freedom

“Do not fear to be eccentric in opinion, for every opinion now accepted was once eccentric.” – Bertrand Russell ||

Hi all! The week is just starting and already it feels weird… The market is now 65% convinced Wednesday’s rate cut will be a big one, yet even that isn’t instilling confidence in crypto investors. 😕

Below, I look at what I think the market is getting wrong about real interest rates and the impact of rate hikes, now that the US is about to start the descent. I also raise my eyebrows at the SEC’s regulatory strategy, point out an example of how the drive for safety suppresses free speech, and extrapolate possible BTC price targets (not predictions!!) based on where the asset is in the current cycle.

I had more on the list to cover today, but I’m always wary of making these too long out of respect for your time (and Substack’s algorithm) – today’s already got the warnings from Substack 😣, but I think you’ll find it an easy read. Tomorrow I’ll hopefully get to more on global adoption, and the regulator tokenization roundup is on the calendar for Wednesday. I’ve also been working on an overview and comparison of the EU’s big tokenization trials which I will squeeze in this week somehow. Never enough time, never enough pixels!

IN THIS NEWSLETTER:

Real rates are not high and credit has not tightened

Gaslighting, or a confused SEC?

The BTC cycle: where are we?

The Sony blockchain has momentum

Who decides what “safe” is?

If you find Crypto is Macro Now in any way useful or informative, would you mind sharing it with your friends and colleagues, and maybe encouraging them to subscribe? ❤ I’d be really grateful!

WHAT I’M WATCHING:

Real rates are not high and credit has not tightened

We can be pretty certain that this week the US finally embarks on the downward slope of interest rates. This will come as a relief not just in terms of sentiment (it’s started, we can breathe easier now) but also liquidity, as in theory lower fed funds encourages banks to lend which means the money supply gets a boost.

In theory.

Only, there’s not much evidence that the hiking of rates tightened credit. The idea makes intuitive sense, since if interest payments are higher, fewer companies and people will borrow and therefore spend and this should bring down inflation.

But credit didn’t tighten.

The growth in commercial and industrial credit has been bobbing around 0% for the past couple of years.

(chart via FRED)

Obviously, 0% loan growth is a decline relative to the economy. But this doesn’t account for the explosion in private credit over the past few years. There are no reliable numbers as to the size of this market (it is private, after all), but in February the Federal Reserve estimated that just over $1.2 trillion in private debt strategies have been deployed, roughly half of that in direct lending.

(chart via the Federal Reserve)

A more recent paper, published in July, estimated that the private credit market had reached roughly $1.5 trillion, or more than half of the total commercial and industrial credit from traditional banks. (If you don’t feel like reading the paper, the Odd Lots podcast recently interviewed the authors, worth a listen.) The IMF estimates that the total of issued private credit has reached a whopping $2.1 trillion.

So, loan growth may have stagnated, but that doesn’t mean credit did.

And the Chicago Fed’s financial conditions index has for some time been as loose as before the Fed started hiking!

(chart via the Chicago Fed)

Sure, much of that is due to a rising stock market (which boosts collateral values), but even stripping out everything except “credit”, conditions are loose.

(chart via the Chicago Fed)

Consumer credit has also expanded, registering in July its strongest growth since November 2022.

(chart via Daily Chartbook)

This could be because us humans are wired for growth and, collectively, we’ll find a way, even at high real rates.

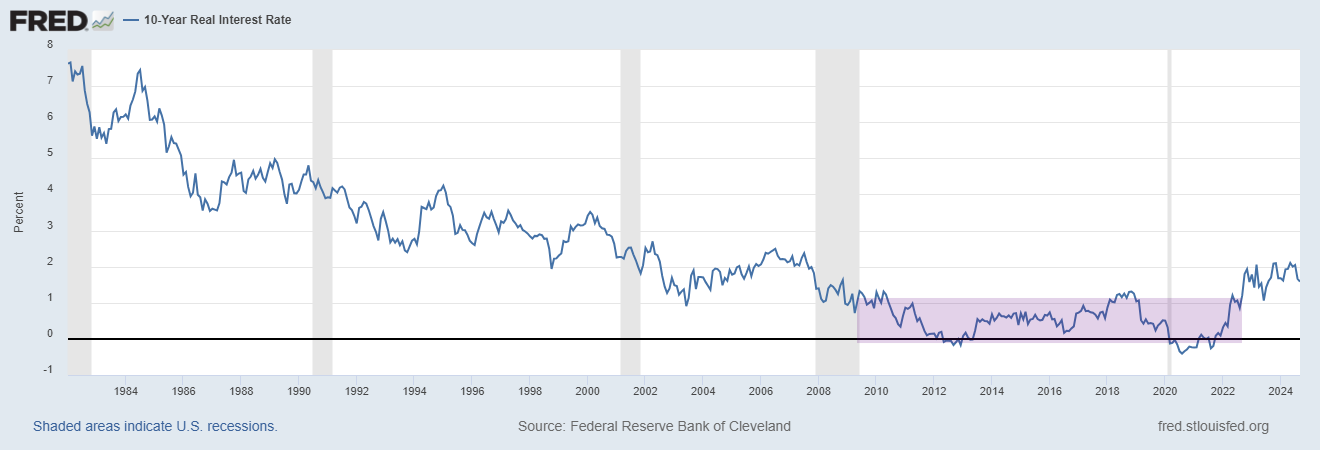

Plus, real rates are not that high.

Yes, they are much higher than during the period between the Great Financial Crisis and the pandemic. But in that period, real rates were abnormally low. It’s unlikely we’re going back to that period – there’s no monetary need to (although I acknowledge that fiscal pressures may win, but if so there’s a whole different set of problems to worry about). Extracting the inter-crisis period, real rates are currently within a normal range. They’re not high, they’re normalizing.

There are many different ways to measure real rates. One that I follow is the Cleveland Fed’s model for 10-year real rates, which is created using a bunch of inputs including economic reports, surveys and market data.

(chart via FRED)

(I know, chart crime, you can’t just ignore a long stretch of data – only, I’m arguing that assuming a recent abnormal period is the new normal leads to a foggy recency bias.)

A simpler, back-of-envelope measure of real rates is the Fed funds rate minus inflation:

(chart via TradingView)

And here’s a composite of Treasury yields adjusted for inflation, which can be taken as a benchmark for the real yield on government bonds:

(chart via FRED)

But inflation will continue to come down and therefore real yields will go up unless rates change, you say? Well, I’m not convinced inflation will come down much from here, but for the sake of argument, let’s say the Fed does achieve its target of 2% (I know, I’m conflating the Fed’s preferred measure of PCE with the easier-to-chart CPI, but this is just for illustration).

So, if 2% real yields are “normal”, per pre-GFC history, then the Fed funds (again, simplifying) should be around 4%.

But, according to CME pricing, the market is expecting rates to be at 3% or lower by next June (~80% probability!).

(chart via CME FedWatch)

The only trigger I can think of that would push rates that low is a Federal Reserve scrambling to pull the US out of a sharp recession. The stock market is not pricing that in at all.

And if you prefer to use Treasury yields as your real interest rate benchmark, this suggests that the bond market is also due for a correction as the market adjusts to the “new normal”. Unless, of course, things get really bad out there, which we should fervently hope doesn’t happen.

You’re reading the premium daily Crypto is Macro Now newsletter, in which I look at the growing overlap between the crypto and macro landscapes. If you’re not a full subscriber, I do hope you’ll consider becoming one. It’s a couple of New York coffees a month, for which you get ~daily commentary on narratives, rates, economic data, crypto adoption, tokenization, geopolitics, privacy, regulation and the likely impact of both resilient and coopted decentralization. This is not a “news” project – it’s about what I think matters for broader crypto impact, and why.