Stablecoin liquidity: the risk to banks

Plus: Bitcoin adoption, market momentum and more

“The history of the world is none other than the progress of the consciousness of freedom.” – GW Hegel ||

Hi everyone! I hope you’re all doing well and remembering to step away from your screens as often as you can.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

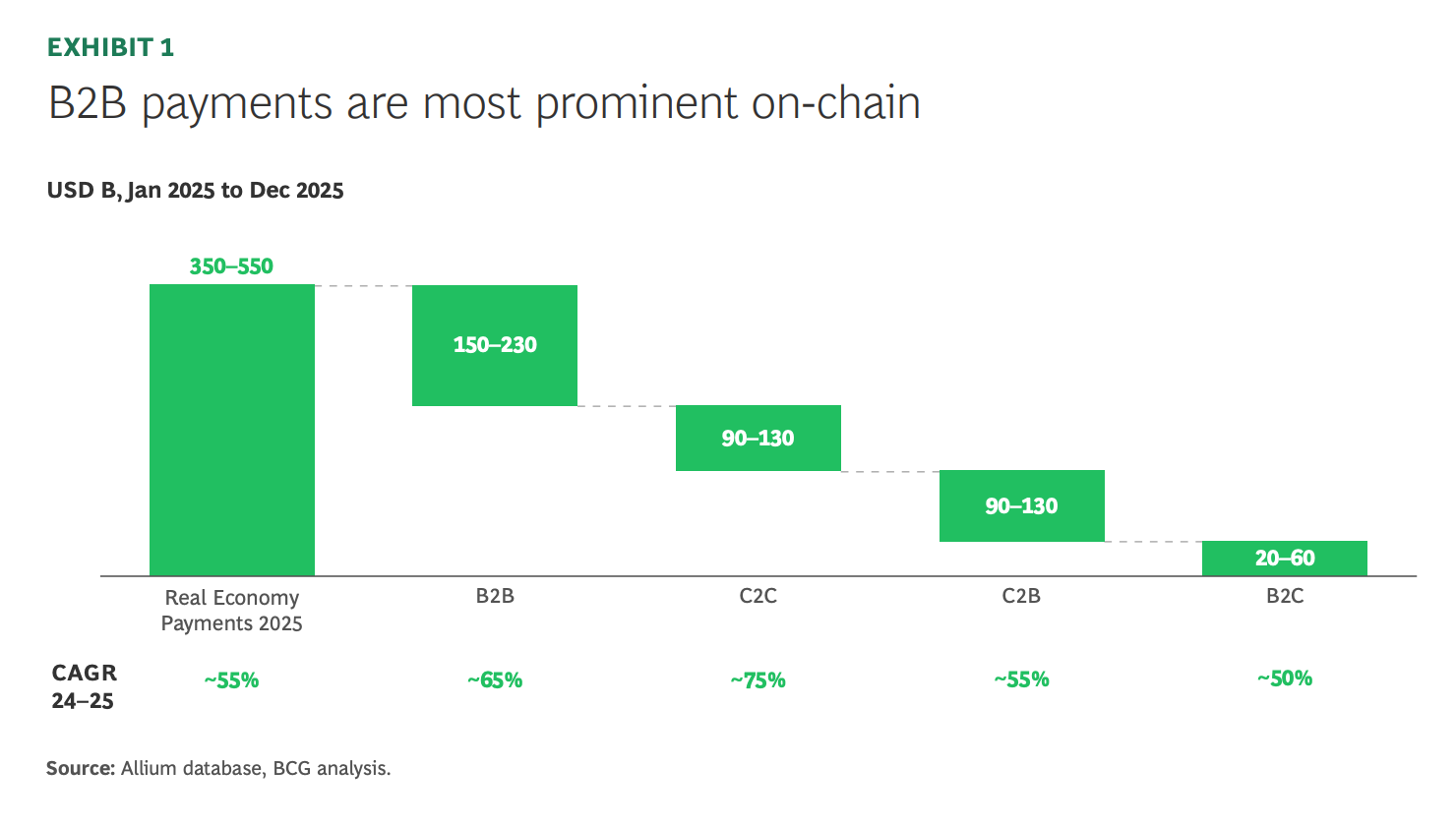

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Stablecoin liquidity: the risk to banks

Bitcoin adoption

Markets: a momentum shift?

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

Stablecoin liquidity: the risk to banks

The New York Fed has published a paper on the risk to banks posed by stablecoins. It may feel like we’ve seen so many of these over the past year, but at least this one takes an original angle.

Stablecoins don’t just compete with deposits; they also demand higher liquidity from banks due to their more agile circulation – this requires banks to hold higher reserves, which dampens lending.

The conclusions are based on matching onchain stablecoin issuance and redemption with Fedwire wholesale payments, focusing on banks that service stablecoin businesses and comparing their liquidity needs to a cohort of similar-sized banks that don’t. Since mid-2023, the former group have seen a surge in Fedwire payments correlated with stablecoin primary market movements, accompanied by sharp intraday reserve balance swings, higher average reserves and lower lending.

If stablecoins scale to trillions of dollars, the paper argues, the distortions passed on to partner banks could destabilize the whole system while impeding the implementation of monetary policy.

The conclusion, therefore, is that higher monetary velocity is bad. To be fair, the authors don’t exactly say that – their aim is to point out an overlooked risk. But the suggestion is clear.

It’s worth pointing out that the model was constructed using one stablecoin issuer and two partner banks.

And it overlooks that, after the banking stress of 2023, stablecoin issuers tend to keep bank deposits at a minimum anyway, preferring to rely on repo for short-term liquidity – so, the impact of higher payments velocity on deposits is mitigated. The authors acknowledge this, but fail to contemplate the rapidly growing asset class of tokenized money market funds which, once widely held as stablecoin reserves, will both enhance redemption reliability and further mitigate the liquidity-related impact on bank reserves.

Plus, the paper ignores any revenue benefit from stablecoin partnerships which could not only boost a bank’s bottom line, it could also strengthen balance sheet health through industry and activity diversification.

As with the protests over stablecoin yield and rewards, this feels like banks clinging to a monopolistic privilege in the face of an onslaught of necessary innovation. After all, reliance on sticky funding is a coveted luxury for any business that wants to leverage deposits into risky ventures – just ask any private equity or debt manager. But that privilege does not help consumers or businesses.

The paper’s conclusions also highlight just how much our understanding of money is changing: it assumes that sticky money needs to be based on the same instrument as agile money. This assumption is worth questioning as we push for a clearer differentiation between money that moves and money that doesn’t.

✨ If you find this newsletter at all useful, or even if you just like my excellent music recommendations, would you mind sharing it with friends and colleagues and nudging them to subscribe? I’d appreciate it! ✨