Stablecoins and Treasuries: which affects which?

Plus: strange relative moves in crypto, US jobs, endogeneity and more

“Change your opinions, keep to your principles; change your leaves, keep intact your roots.” – Victor Hugo ||

Hello everyone! I hope you’re all doing well. Apologies for the late send today. Sometimes I’ll dive into a topic, thinking I’ll scribble a quick comment, only to find it’s much more interesting than I expected. It turns out rabbit holes are hard to get out of, who knew.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

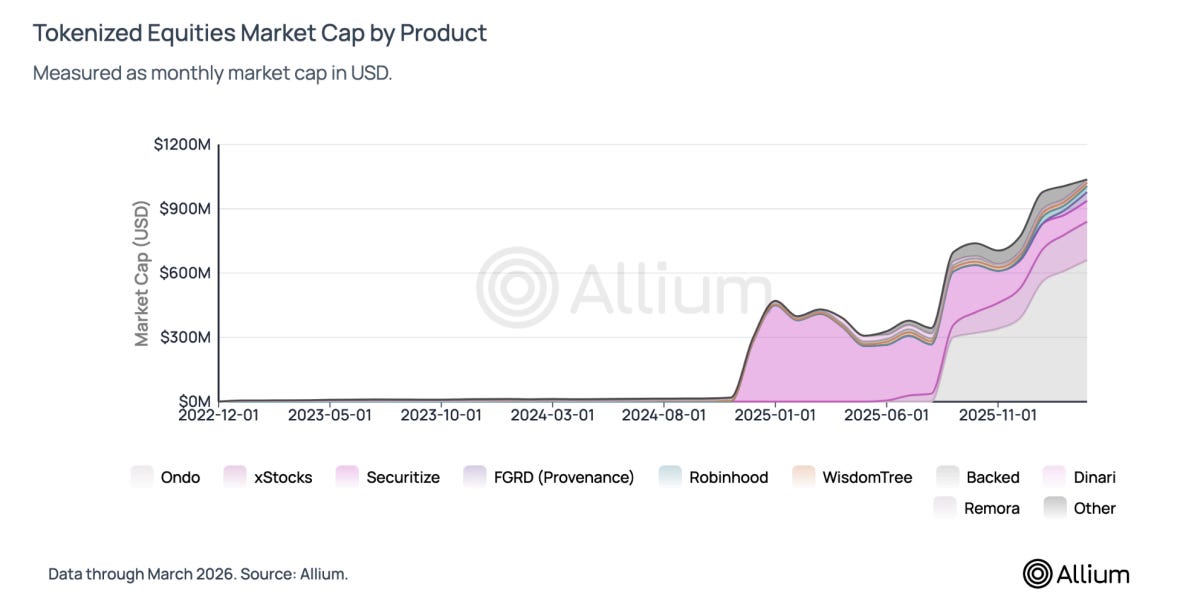

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

IN THIS NEWSLETTER

Stablecoins and Treasuries: which affects which?

Term of the day: endogeneity

Markets: it’s all relative

Macro: US jobs are doing OK

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you so much!! ❤

WHAT I’M WATCHING:

Stablecoins and Treasuries: which affects which?

This morning I started skimming an updated BIS paper by Rashad Ahmed and Iñaki Aldasoro that looks at the relationship between stablecoin demand and Treasury yields. I’m not sure why I did this, as we’ve seen so many of these papers before. Yes, we’ know they’re related, and yes, we know that’s why the US Treasury Secretary is so excited about the potential demand.

I’m glad I did, though, as it turned out to be a lot more interesting than I expected, especially because of the discussion of endogeneity, which has been largely absent from most other papers I’ve skimmed.

(A confession that may sound like a humblebrag but really isn’t: I have a degree from Brown University in Applied Mathematics and Economics, which perhaps goes some way towards explaining why I can be such a pedant at times. Anyway, despite that, I understood very little of the technical side of the paper, which is no doubt more down to my terrible memory and rapidly advancing age than to the education received. I bring this up because I had to look up “endogeneity” and am now fascinated with it – I do my best to explain it in the “Term of the day” section below.)

This paper finds that stablecoin demand influences short-term Treasury yields.

No surprise there, but the authors provide numbers:

A $3.5 billion 5-day inflow into stablecoins lowers 3-month T-bill yields by 0.7 basis points on impact, and up to four basis points within 10 days (deployment lag, some tokens distributed from pre-issued stock).

The effects can be roughly double at times of market stress.

Lifting the lid, the conclusions get more interesting when we compare the updated paper with the original, published just over a year ago. I asked Grok to pull the differences for me:

The methodology has been changed to get a more refined flow-through estimate, but I won’t go into more detail here because there’s not much hope of my understanding it in the time I have to write this. It has to do with a more granular exploration of endogeneity (see below).

This has led the authors to almost double the estimated impact.

Also, the original paper highlighted the asymmetry of the stablecoin impact – a jump in demand had a more pronounced impact than a drop in demand (more upside than downside). The new paper downplays this, focusing more on the state of the market – the impact of stablecoin demand is greater when markets are stressed.

So, extrapolating, if the total current market capitalization of fiat-backed stablecoins of around $270 billion goes up by 10% from here, we’re looking at a roughly 30 basis point drop in the 3-month T-bill yield. That… doesn’t feel particularly significant.

And it’s much, much less than other studies I’ve seen.

Here’s where the “endogeneity” comes in (see below for definition). The authors recognize that: