The China question, consumer sentiment and mixed messaging

Plus: what’s ahead for the week, a war impact update and more

“We have no future because our present is too volatile. ... We have only risk management.” – William Gibson ||

Hi all! I hope you had a good weekend. I actually went to the cinema for the first time in years, to see Project Hail Mary - my expectations were low as I loved the book, but it was surprisingly good. 😊

Here in Europe we finally changed our clocks (although I would like that hour back, please) so US readers will start to get this email in their inbox earlier than of late.

🌸

Production note: Easter is a big deal where I live, and so I’ll be taking a much-needed short break from Thursday-Saturday – back on Monday!

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

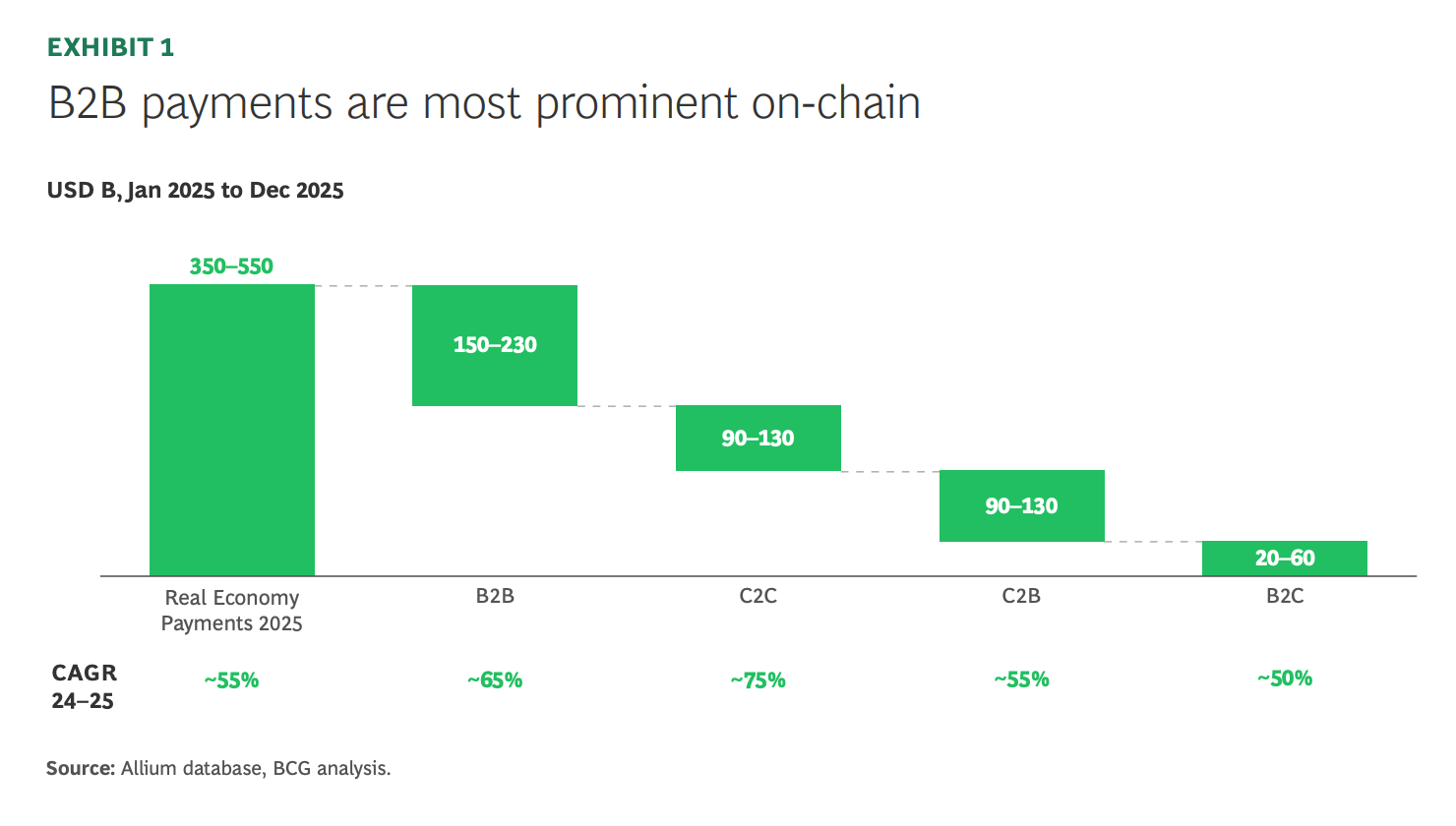

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER

Coming up this week: jobs and inflation

Monday mood: the China question

Markets: incoherence

Macro: US consumer sentiment

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

✨ Use the discount code MACRO for 20% off!

Coming up this week:

The big deals on the macro front this week are US jobs and global inflation. We get a slew of reports on the US jobs market, finally back in their usual rhythm. We also get a slew of post-war inflation reports.

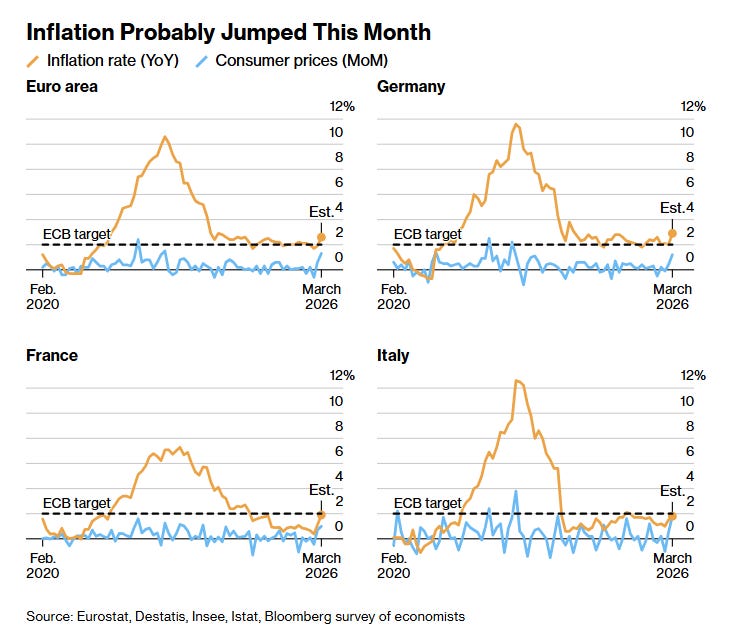

On Monday, we get inflation reports from Germany and Japan – it’s still early days, but these could end up showing some impact from the Iran war. (Spain’s CPI report out on Friday showed the highest month-on-month increase since March 2022, the highest year-on-year – 3.3% – since May 2024.)

The G7 energy ministers hold an emergency virtual meeting.

Fed Chair Jerome Powell speaks at an event at Harvard University.

And the US Senate goes into recess until April 10.

On Tuesday, we get March inflation data for the Eurozone as well as France, Italy and the Netherlands. Expectations are for significant upticks across the board.

(chart via Bloomberg)

We also get the US JOLTS job openings report for February, and the Conference Board consumer confidence index.

On Wednesday, we get the latest read on US consumer strength via the retail sales report, expected to show some resilience with a 0.3% increase ex-autos and gasoline.

Also on Wednesday, we get final S&P Global PMI economic activity reports for the US, China, South Korea as well as several European countries; and ISM manufacturing PMI for the US, expected to deliver the third consecutive month of expansion for the first time since 2022.

Plus, there’s the private ADP US payrolls report for March, expected to show a slowdown from a gain of 63,000 in February to 40,000.

Thursday is a public holiday where I am, so this newsletter will be taking a short break.

Same with Good Friday, which over 100 countries mark with a public holiday.

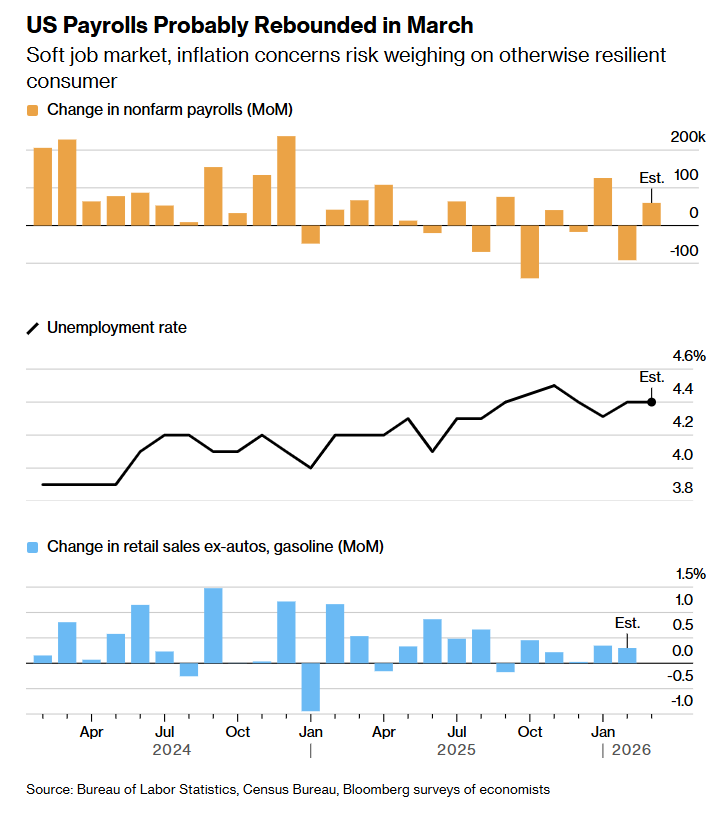

US markets are closed, but we’ll still get the BLS payrolls figure for March, expected to show a rebound after February’s dreadful report of a 92,000 contraction. Consensus expectations point to a net 60,000 jobs added to the US economy in March, with the unemployment rate holding steady at 4.4%.

(chart via Bloomberg)

Monday mood: the China question

(what’s on my mind as we head into the week)

My feed these days is a flurry of conflicting opinions on whether the Iran war is really about weakening China, or whether China will emerge a winner.

Both can be true.