The cost of escalation

plus: the Feds confusion, inflation alarms, market nerves and more

“Not everything that is faced can be changed, but nothing can be changed until it is faced.” – James Baldwin ||

Hi everyone! I hope you’re all doing ok, managing stress levels, taking care of yourselves…

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

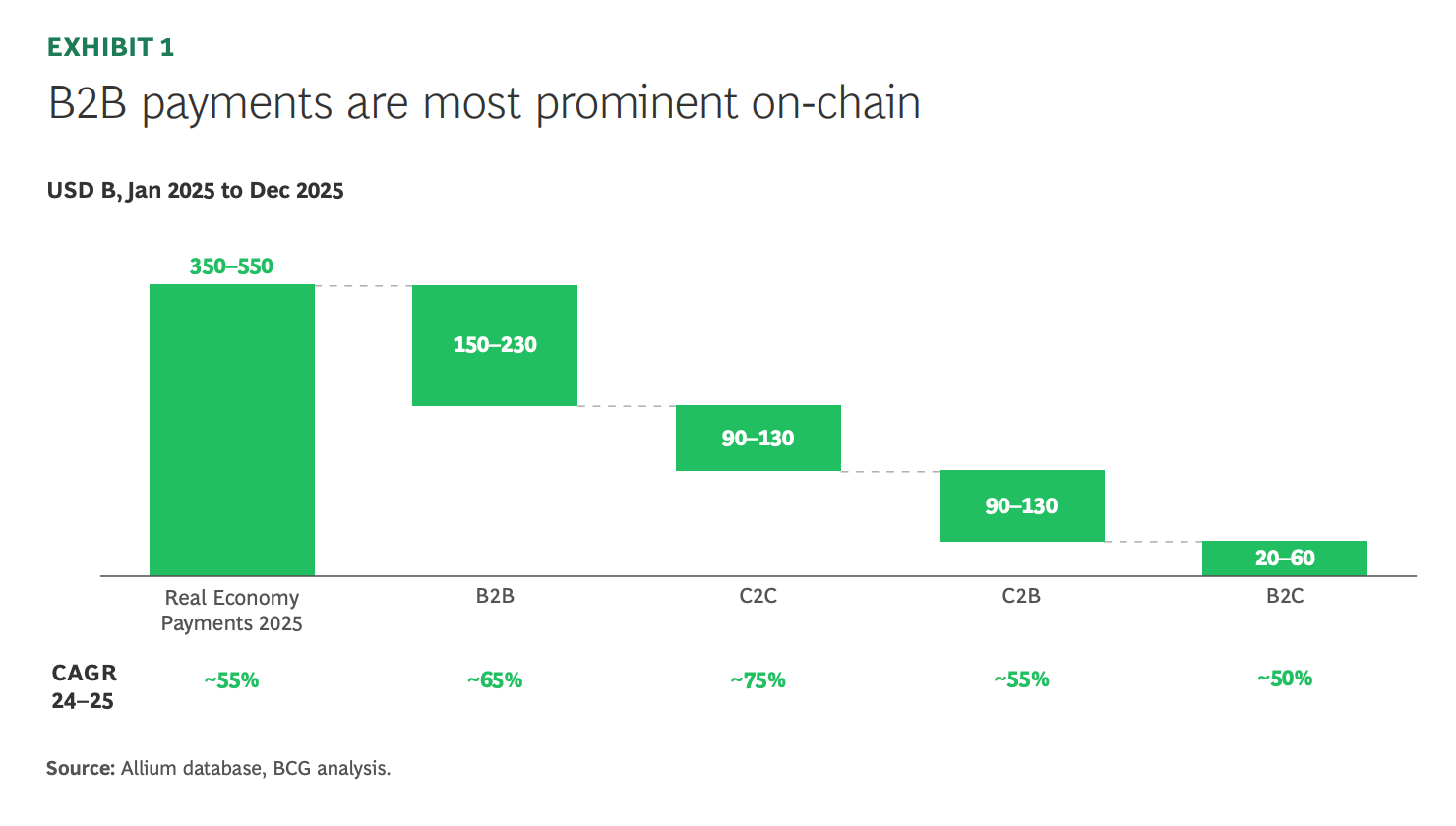

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

The cost of escalation

The Fed’s confusion

Macro: PPI alarms

Markets: hooo boy

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

✨ Use the discount code MACRO for 20% off!

The cost of escalation

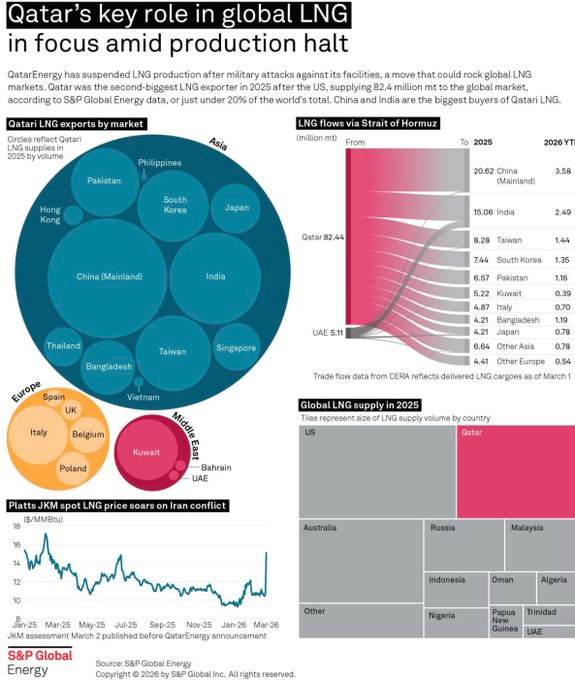

The war in the Middle East entered a new phase yesterday with an attack by Iran on the world’s largest LNG plant.

Ras Laffan, based in Qatar, suffered “significant damage” according to an official statement. We don’t yet have full details, but we can assume those words were chosen carefully and probably understate the impact.

Over the past 24 hours, drones have also hit refineries in Saudi Arabia and Kuwait.

This is a very big deal for global energy prices, now and going forward. Ras Laffan accounted for about a fifth of global supply before production was halted soon after the conflict started as a precautionary measure. The structural damage rules out a full reboot once the conflict cools.

(Brent crude $/bbl, chart via TradingView)

This will lift gas and electricity prices pretty much everywhere, feeding through to inflation and reduced consumption. It will especially hurt businesses and consumers in Asia and Europe, dependent on Middle East imports.

(infographic by S&P Global, via @baldersdale)

What’s more, the squeeze won’t be limited to energy (although that’s bad enough) – food prices are likely to climb as LNG is a key component of fertilizers.

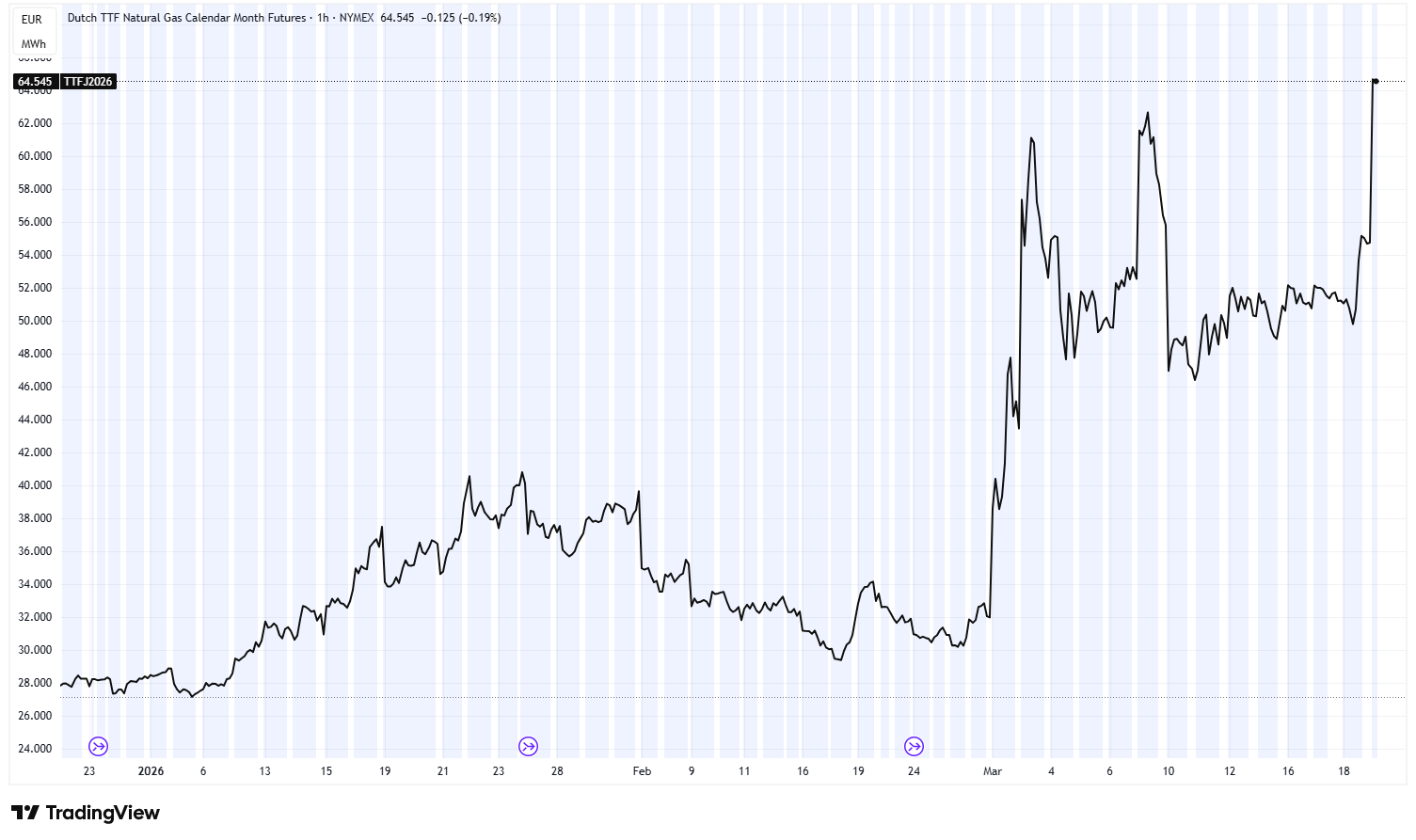

The impact is not just economic, with tighter corporate margins and weakening consumption potentially leading to more layoffs, even more weakness in consumption and so on in an awful spiral. We could also see foreign sovereign as well as corporate holders of US government debt need to sell treasuries in order to cover revenue shortfalls and rising costs.

(TTF Natural Gas, chart via TradingView)

And then there’s the inevitable stimulus ahead as nations scramble to “provide assistance” to businesses hit by the higher costs and economic support for individuals struggling to pay bills amid climbing inflation and unemployment. Where will the money come from?

In sum, conviction the conflict will be over soon is weakening, as is confidence energy will start flowing when it does. Smart strategists insist the US is winning, others insist it’s losing, when the fog of war means none of us know. Qatar Energy has just announced that it may have to declare force majeure on all long-term delivery contracts for up to five years. Meanwhile, US Treasury Secretary Scott Bessent said earlier today that the US is considering lifting sanctions on Iranian oil already at sea, in what is no doubt a confusing message to US allies in the region and an encouraging confirmation to Iran that their aggression is working.

The Fed’s confusion

From the violence of war to the cool calm of a central bank press conference…

Yesterday’s FOMC statement and updated projections packed a few punches, as did Chair Powell’s comments to journalists.

The main points of interest:

FOMC members are more optimistic, on average, for GDP growth in 2026 and 2027. And expectations of long-run GDP growth have been nudged up from 1.8% to 2.0%. When asked about this, Powell explained that most on the committee feel that productivity is increasing, even before the impact of AI kicks in. Good news, but not for those hoping for rate cuts as a higher productivity rate and long-run GDP growth will push up the “neutral” interest rate r*, weakening the case for a “recalibration”.

With higher growth comes higher inflation – the FOMC expects, on average, a 2.7% headline increase in 2026 (vs 2.4% in December’s projections), with core PCE growth moved up from 2.5% to 2.7%. That is too high to justify cuts.

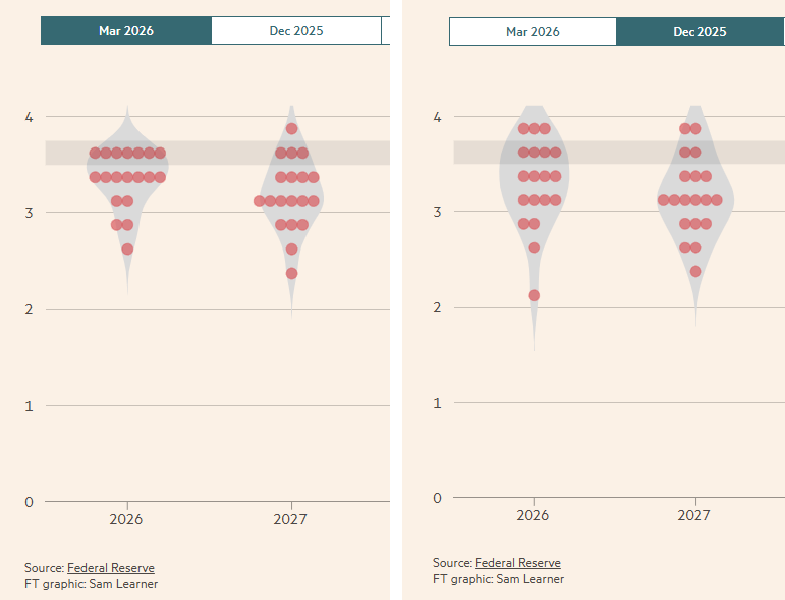

Yet the average expectation for the fed funds rate at the end of 2026 did not change, signalling only one cut this year and one next year, far from the drastic easing favoured by President Trump and Fed Governor Stephen Miran. The distribution of expectations did change, however – even the most dovish call, presumably from Miran, was raised. The number of FOMC members forecasting more than two cuts for the remainder of this year has gone from eight in December to just five.

(charts via the Financial Times interactive graphic)

While no member pencilled in expectations of higher rates in the near future, Powell did confirm that the possibility of the next move being a hike came up in discussions.

As for the likely impact of the war in the Middle East on inflation and the economy more broadly, Powell had this to say:

“The economics effect could be bigger, they could be smaller, they could be much smaller or much bigger. We just don’t know.”

Compared to the firehose of confident predictions in our feeds and headlines these days, that level of honesty is refreshing.

Given the uncertainty, Powell stressed that we shouldn’t read much into these forecasts – but, as he joked, FOMC members can’t pencil in “I don’t know”. He even questioned whether releasing updated forecasts was a good idea at this stage.

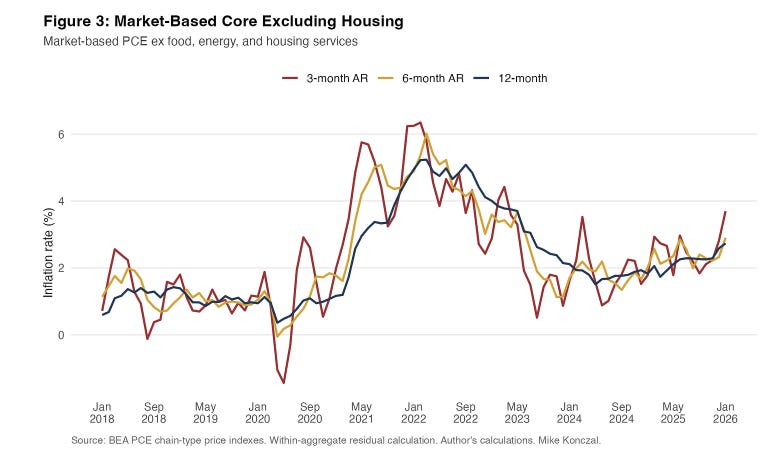

The Fed chair sounded perplexingly baffled as to why non-housing services inflation was proving to be so sticky – it’s “frustrating”, he said. He was more clear on the driver of revived goods inflation: it’s the tariffs.

(chart by Mike Konczal)

Perhaps the upward PCE trend is finally getting through, as Powell sounded more hawkish than usual, going as far as saying that interest rates might no longer be at a restrictive level – in other words, we can be sure he’s voting for no cuts.

He also stressed that inflation is the priority, not a weakening jobs market – no progress on inflation = no rate cut.

The 92,000 drop in the official BLS payrolls report for February was not, he explained, a sign of a crashing job market, as most of the decline can be explained by bad weather and strikes.

Powell’s stance matters more now that we know he might be staying on the Fed Board for longer than President Trump would like. He confirmed that he will remain as temporary chair until his successor is confirmed, per standard practice – Kevin Warsh’s confirmation may get held up due to the ongoing DOJ investigation. And Powell made clear he would not resign from the board (his term as Governor ends in 2028) until the investigation was completed.

Macro: PPI alarms

As if all of the above wasn’t enough bad news for one day, yesterday’s release of the US Producer Price Index (PPI) report for February, a gauge of wholesale inflation, delivered another blow to hopes of softer inflation.