The febrile landscape and the market reactions

Plus: what’s ahead this week, US jobs, BTC and more

“Few new truths have ever won their way against the resistance of established ideas save by being overstated.” – Isaiah Berlin ||

Hello everyone! I hope you’re all doing well and got to disconnect at least a little over the past couple of days, because things are going to be hectic this week.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

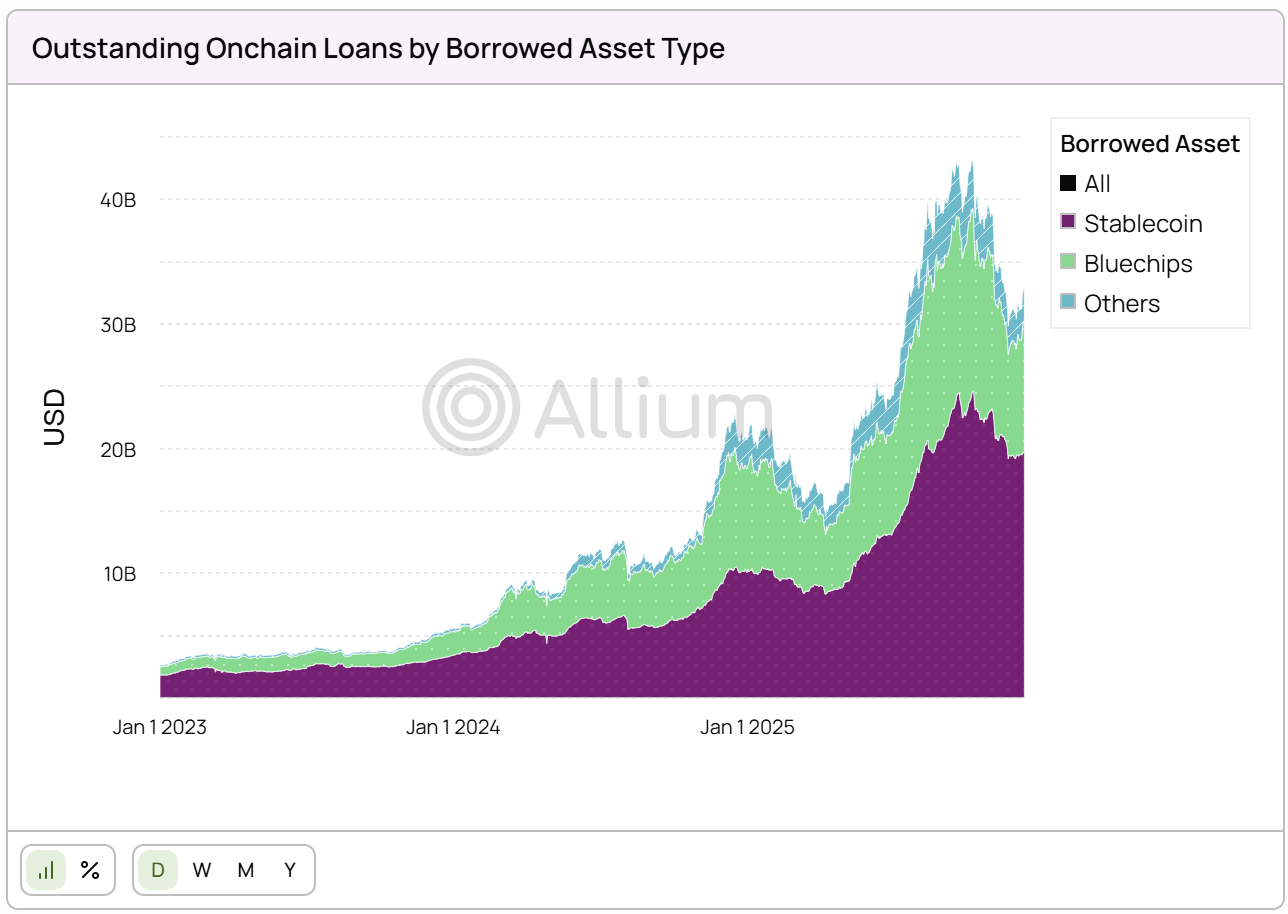

Our latest whitepaper published with Visa, Stablecoins Beyond Payments: The Onchain Lending Opportunity, examines how banks can access emerging credit markets. Looking at the data, outstanding onchain loans reached over $40Bn this year, with stablecoins making up more than half of borrowed assets.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Coming up this week: CPI, crypto markup, Fedspeak, tariffs, earnings and more

A febrile mood

Markets: still numb

Macro: US jobs

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links, a music recommendation (‘cos why not?), and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

Coming up this week:

CPI week! Plus, US Federal Reserve officials are out in force, speaking at events and on media interviews. Doing a quick skim, I counted 16, I won’t list them all here. But one of the key ones will be New York Fed President John Williams’ keynote today at the Council on Foreign Relations.

Also, today Washington D.C. is host to finance ministers from the G7, in town to discuss rare earths.

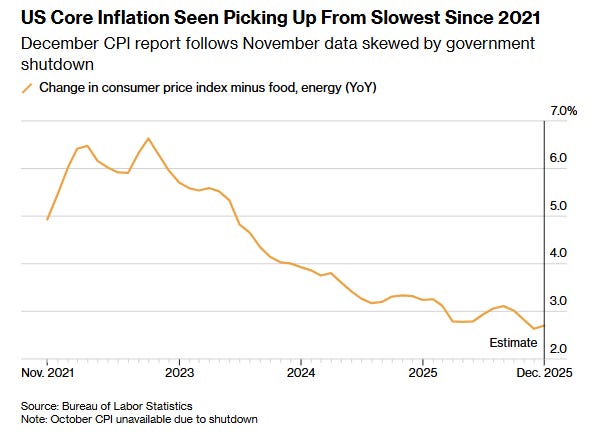

Tomorrow, we get the US CPI report for December – consensus estimates suggest a 2.7% year-on-year increase for the core index (ex-food and energy), slightly higher than the 2.6% growth seen in November.

(chart via Bloomberg)

Also on Tuesday, JPMorgan kicks of Q4 bank earnings reports.

On Wednesday, we should hear the Supreme Court ruling on whether President Trump has authority to invoke IEEPA to enact sweeping trade tariffs. (I wrote about this last week.)

We also get the US retail sales for December, expected to deliver a solid increase of 0.4% month-on-month. And we get the US Producer Price Index – this gauge of wholesale inflation has been holding steady in recent months at around 2.7% year-on-year.

Plus, Fed Governor Stephen Miran speaks on monetary policy at the Delphi Economic Forum Lecture in Athens – since he represents what the Administration wants from the Fed, it’ll be worth taking notes on that one.

And we get the Fed’s Beige Book, which will give us anecdotal evidence of the economic mood in the regional districts, as well as earnings from Bank of America, Wells Fargo and Citigroup.

Thursday is gearing up to be a key day for the crypto industry, as the CLARITY Act gets markup sessions from both the Senate Agriculture Committee and the Senate Banking Committee (for non-Americans, a markup session is a legislative committee meeting to debate and amend a bill). If the committees vote to approve the bill, the next step would be a full Senate vote. I’ll write more about this over the next few days – there’s a lot riding on this one.

Also on Thursday, Federal Reserve Governor Michael Barr participates in a panel on stablecoins at the Wharton Future of Finance Forum.

And we get earnings from Morgan Stanley, Goldman Sachs and TSMC.

A febrile mood

I know that, taken literally, we’re always living through history as each day is a piece in that convoluted puzzle. But there are times when the phrase takes on a meaning that we all instinctively recognize, when “history” takes on a capital H and so much is in movement we’re not sure what to hold on to.

This month is one of those periods. We’re not yet two weeks in and already five key geopolitical regions are changing shape.