The geopolitics of blockchain use cases

Plus: the outlook for US sanctions, manipulation fatigue, what’s ahead this week and more

“No longer certain that one ever does win a war, I am.” – Yoda, The Clone Wars ||

Hi everyone! I hope you all had a great weekend. And, you know, May the Fourth be with you.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

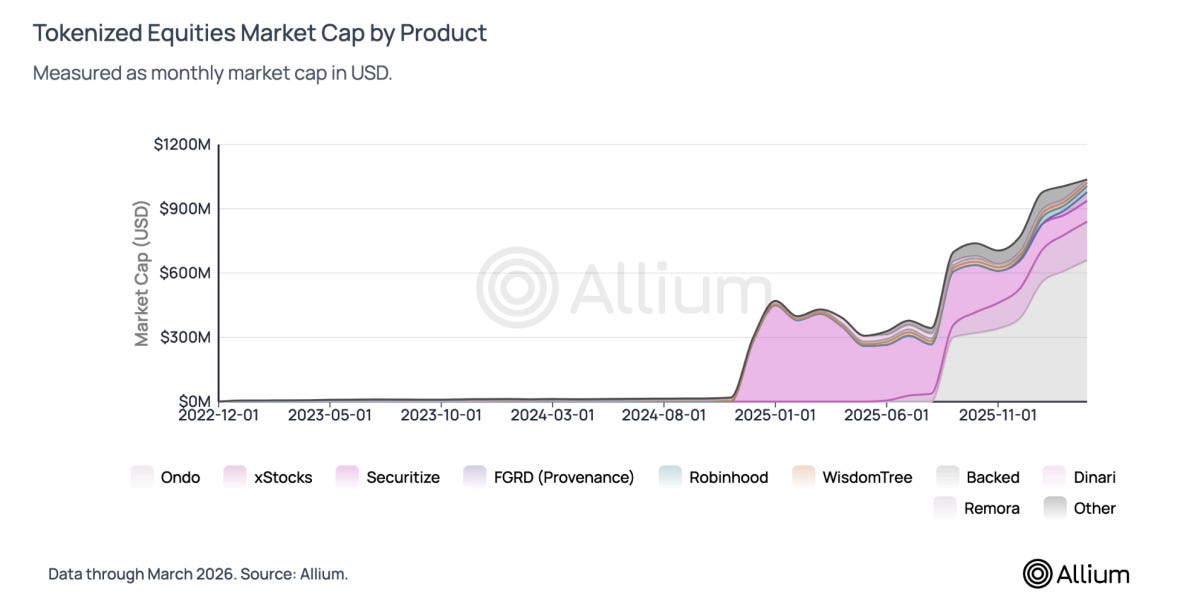

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

IN THIS NEWSLETTER

Coming up this week: US jobs, PMIs and Fedspeak

Monday mood: The geopolitics of blockchain use cases

Markets: what does “help” mean?

The outlook for US sanctions

Term of the day: Teapot refinery

Crypto is Macro Now offers ~daily commentary and updates on how crypto is impacting the landscape, vice versa, and why this matters more now than ever. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

✨Press Publish with John ‘Alyosha’ Johnston✨

Next Friday, May 8th, come join me in a conversation with John ‘Alyosha’ Johnston, author of the Market Vibes newsletter on Substack.

If you don’t already know JJ’s work, it’s an essential read for anyone interested in markets and/or commodities, written by someone who brings decades of trading experience to your inbox and yet still treats each day as an adventure in learning and sharing. We’re not going to chat about price uncertainty or macro, we’re going to discuss newslettering – why he does what he does, how he gets so much done, what’s worked for him on Substack, what hasn’t, what advice he’d give others starting out, and more.

Join us next Friday, May 8th, at 11am EST/5pm CEST.

Coming up this week:

Jobs week! Plus, a ton of public appearances by Federal Reserve officials, too many for me to list – but you may be interested in those from Cleveland Fed President Beth Hammack and Minneapolis Fed President Neel Kashkari, two of the three FOMC meeting dissenters pushing for a removal of dovish language from the statement (both are on Thursday).

Today, the UK and Japanese markets are closed for a holiday, but we get US factory orders, with a slight pickup in growth expected.

Plus, the US Treasury announces its borrowing projections, expected to hold steady.

Tuesday brings the JOLTS job openings report for March, expected to come in roughly unchanged on the previous month.

We also get the two different measures of the US services PMI, and the latest read on the US balance of trade, forecast to show an increasing deficit.

Wednesday gives us the private ADP report on US payrolls for April, with the consensus forecast pointing to a growth acceleration.

And we’ll find out more on the US Treasury’s expected financing schedule.

On Thursday, we get the Challenger report on job cuts, and a preliminary read on US unit labour cost growth, a gauge on wage inflation.

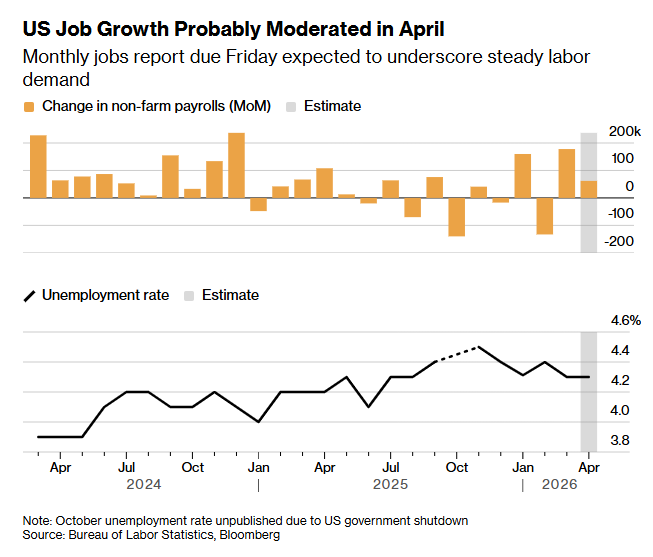

Then on Friday, the Bureau of Labor Statistics releases the big US jobs report for April, expected to show a payrolls increase of 62,000, a stable unemployment rate of 4.3%, and accelerating wage growth.

(chart via Bloomberg)

We also get the preliminary consumer sentiment report for May from the University of Michigan.

Saturday morning brings balance of trade data from China.

Monday mood: The geopolitics of blockchain use cases

(what’s on my mind as we head into the week)

Financial markets, or industry – what plays a greater role in civilizational strength?

Unfortunately, “both” is not a realistic answer as resources require allocation and long-term strategy requires focus.

This question has never been more relevant than now, as geopolitical plates shift, economies mature and new technologies alter the resource balance. You’ll have noticed the gradually increasing heat of the headlines that march across your attention span – these are the window dressing for the building rumble of a more fundamental tension between two superpowers employing radically different approaches to win influence and resilience.

Of course, I’m talking about the US and China. That they are both large and powerful is without doubt. What can be debated is how their relative strengths will influence the competition ahead.

The US dominates financial markets; China wins on industrial heft. This is the result of conscious choices over the decades: the US cultivated the use of the dollar in global trade settlement which in turn fed liquidity on its capital markets while clear rules supported investor confidence and boosted funding activity. China chose to leverage its considerable labour and natural resources to industrialize, with centralized control turbo-charging the speed and spread of growth.

The US is home to the world’s largest financial markets. China is the world’s largest exporter of goods. The US is the world’s largest economy in terms of GDP. China has one of the highest GDP growth rates.

Now, each is eyeing the other’s competitive strength. The US wants to boost its industrial activity, while China wants to strengthen its financial markets. The US is trying to weaken its reliance on Chinese imports; China wants to move away from depending on dollar networks.

You get the picture. Of course, there’s a crypto-related twist.