The tariff shift: what, why and how

plus: macro, markets, musings, what's ahead for the week, and more

“The enemy of the conventional wisdom is not ideas but the march of events.” – J. K. Galbraith ||

Hi all! So, did anything interesting happen while I was out?

Kidding of course, of all the days to have to stay away from screens…

You may be tired of tariff talk, in which case you’ll want to skip my take below – I look into the impact, the market reaction, and the confusion ahead. Plus, I take a squint at some significant macro data drops that were drowned out in the noise, cross fingers for progress on CLARITY this week, outline what’s ahead in terms of macro as well as politics for the week, and more.

Production note: Happy to report that the first eye operation went well, recovery taking longer than I thought, possibly have the second this Thursday, will confirm.

✨

My latest op-ed in American Banker (paywall!) looks at the evolving role of tokenized money market funds, and how they are changing our understanding of what money even is: Tokenized Treasuries: What happens when securities become money?

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

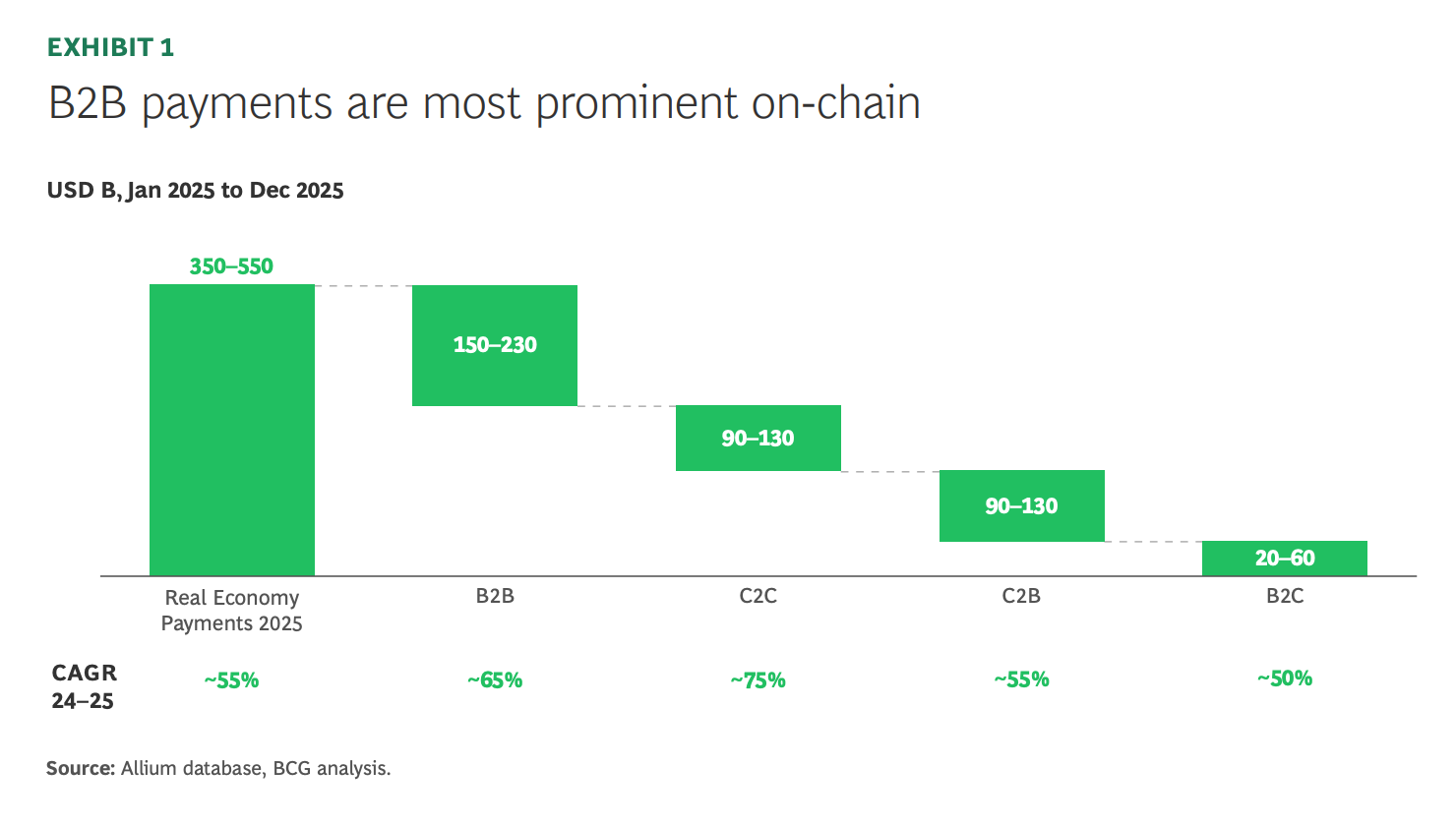

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Coming up this week: politics, Nvidia, wholesale inflation

Monday mood: the CLARITY crunch

The tariff shift: what, why and how

Markets: the reaction

Macro: US economic data

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

Coming up this week:

A relatively quiet week on the macro data front, thank goodness (I mean, after last week…). There will be quite a lot of political scrambling, however.

Today, EU leaders gather to reassess the US trade deal in light of the new tariff situation.

We also get US factory orders for January, expected to show a sharp deceleration.

On Tuesday, President Trump delivers the annual State of the Union speech, which should be spicy, especially if all the Supreme Court justices attend.

We get the Conference Board consumer confidence read for February.

And Germany’s leader Friedrich Merz arrives in China for what will no doubt be an awkward series of meetings.

Wednesday is Nvidia Day! The giant’s Q4 earnings report could either exacerbate stock market jitters, reassure AI optimists, or something frustratingly in-between.

On Thursday, US and Iranian representatives will meet in Geneva to discuss an Iranian proposal for a nuclear deal. Meanwhile, the USS Gerald R. Ford is currently passing through the Mediterranean on its way to the Middle East, adding even more heft to a record buildup of US military assets in the region.

Federal Reserve Vice Chair for Supervision Michelle Bowman is expected to testify before the Senate Banking Committee – her comments on banking regulation reform could be extremely relevant for stablecoins.

On Friday, we get Japan’s December CPI, relevant for the timing of a Bank of Japan rate hike.

And we get the US wholesale inflation (PPI), expected to show a slight deceleration.

Monday mood: the CLARITY crunch

(what’s on my mind as we head into the week)

The deadline imposed by the White House for an agreement between the banking and crypto communities on the stablecoin rewards issue – March 1st – is rapidly approaching. I’m not sure what happens if there is no agreement by then; perhaps the White House stops pushing and pivots to focusing on the midterms, but that feels unlikely at this stage given how much collective work has gone into this.

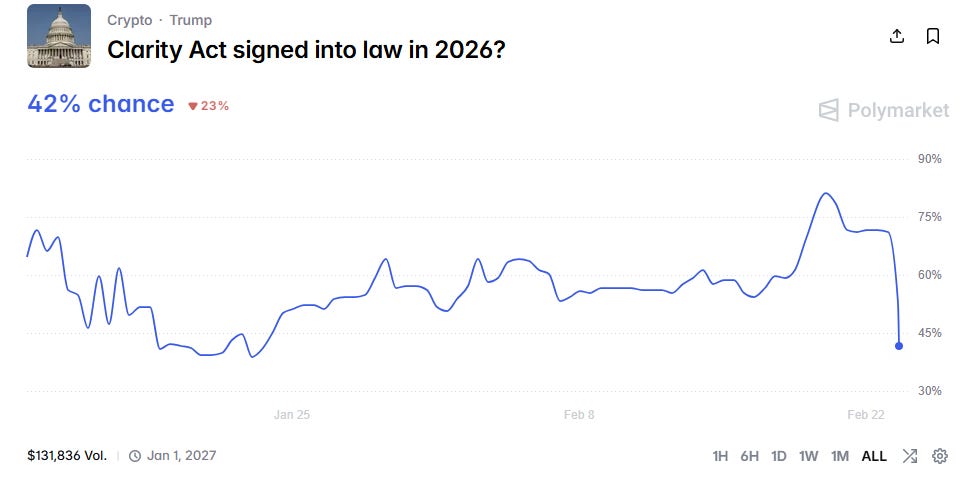

Whatever emerges this week from the negotiations, plenty of people will be surprised: Polymarket currently has passage of the CLARITY Act in 2026 at just over 40%, not a sure thing but not exactly optimistic.

(chart via Polymarket)

I’m in the camp that it will pass, as the banks have a lot to lose if it doesn’t (the GENIUS Act does not say anything about rewards, the banks’ main point of contention). While I still have concerns about stablecoins earning yield or rewards – paying entities and individuals to hold an inert asset could end up sucking funds out of more productive applications such as onchain debt or equity, while centralizing balances as large players undercut smaller innovators – the banking industry should make concessions, as their demands are anti-progress self-sabotage. Embracing the new funding and service opportunities offered by stablecoins has to be better business strategy than trying to stifle their application, and not as if there isn’t already significant competition for deposits from other corners of finance.

But if it doesn’t, it’s not the end of the world for crypto. The agencies will continue to make rapid progress on rule-making, preparing markets and investors for tokenization. Stablecoin distributors can incentivize adoption. And even if the Democrats take the White House in the next election, by then it will be hard to undo what has been built, especially when large financial institutions are making decent profits from onchain activity, and especially when the advantages and the resilience have become even more obvious.

Still, a lot is riding on this week, and if signs of an agreement are confirmed, there will be good reason to celebrate. There’s no such thing as a perfect bill – but having protections for businesses and investors enshrined in law will boost confidence in the crypto industry while setting an example for other jurisdictions.

The tariff shift: what, why and how

On Friday, the Supreme Court finally delivered the decision we’ve all been waiting for: Trump’s use of International Emergency Economic Powers Act (IEEPA) to apply sweeping tariffs is not lawful.

The majority was clear, with six of the nine justices ruling that the Constitution gives taxing authority to Congress, not the President, and that Congress never meant for IEEPA’s power to regulate imports and exports to extend to tariffs.

This was the crux of the argument: does the power to “regulate” include the power to “tax”? The Supreme Court says no, and that had Congress meant it to, it would have said so explicitly.

The Administration has argued that this limitation makes little sense, and Trump in his post-decision press conference railed against a law that allows him to “destroy a country” by banning their imports, but that he “can’t charge a little fee”.

Alex Tabarrok had an insightful take on why this is so – the rule is about prevention not policy:

“A fire chief may have the authority to close roads during an emergency but that doesn’t imply that the fire chief has the authority to impose road tolls.”

Notably, in a rare example of an institution staying within its lane, the justices took care to stay out of whether the trade situation Trump was trying to redress could be considered an “emergency”, preferring to limit their role to interpretation of the Constitution.

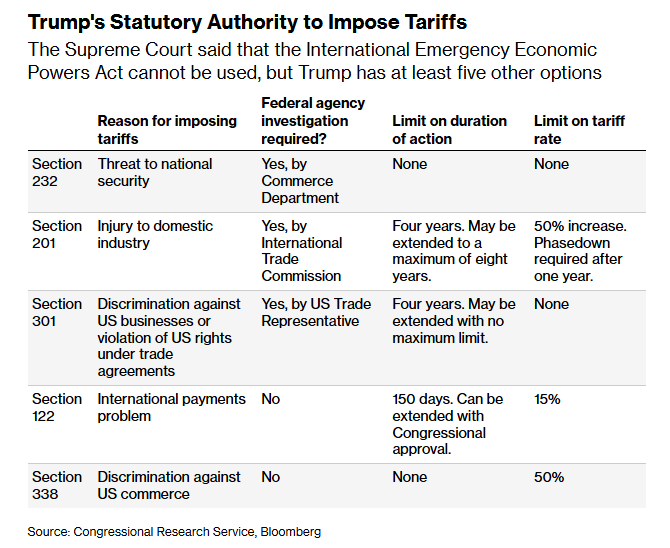

Almost immediately, Trump responded by applying a blanket 10% tariff on all trading partners, under Section 122 of the Trade Act of 1974. This stipulates that the President can unilaterally impose a maximum 15% tariff for a period of 150 days to rectify a balance-of-payments deficit or a sharp dollar depreciation. Any extension would have to be ratified by Congress, which in this case is extremely unlikely given opposition even within the Republican Party and the proximity to the mid-term elections. But it in theory gives the Administration time to work on additional applications. These could draw on Section 232 of the Trade Expansion Act of 1962 – this allows the President to impose tariffs on any item deemed, after an investigation, to be of interest to national security – and Section 301 of the Trade Act of 1974, which empowers the President to respond to unfair trade practices by another country, also after a documented investigation.

(table via Bloomberg)

Someone must have whispered in Trump’s ear, as within 24 hours he had upped the Section 122 tariff to 15%.

There are some exemptions, such as steel, aluminum, copper, lumber, automobiles, semiconductors, precious metals, energy products, fertilizers, beef, tomatoes, oranges, pharmaceuticals, trucks, buses, certain aerospace products, some electronics, and the list goes on – many of these are already subject to Section 232 tariffs.

There’s a potential catch, though. Section 122 allows the President to impose tariffs without going through Congress under a limited set of circumstances: to “prevent an imminent and significant depreciation of the dollar” (not the case), to “cooperate with other countries in correcting an international balance-of-payments equilibrium” (also not the case), and to “deal with large and serious United States balance-of-payments deficit”. This last opening is the one Trump is latching on to… only the US doesn’t have a balance-of-payments deficit. A trade deficit, yes, but that’s not what the law says.

What’s more, Section 122 is meant to apply broadly, not on a country-by-country basis.

This could end up being litigated, especially since the lawyer arguing the Administration’s case before the Supreme Court explicitly said that Section 122 is not applicable as “the concerns the President identified in declaring an emergency arise from trade deficits, which are conceptually distinct from balance-of-payments deficits”.

But, any repeat of the judicial process will take more than 150 days, by which time the tariffs will have expired anyway.

Meanwhile, we wait to see what will happen regarding the various trade agreements, most of which have not been ratified.

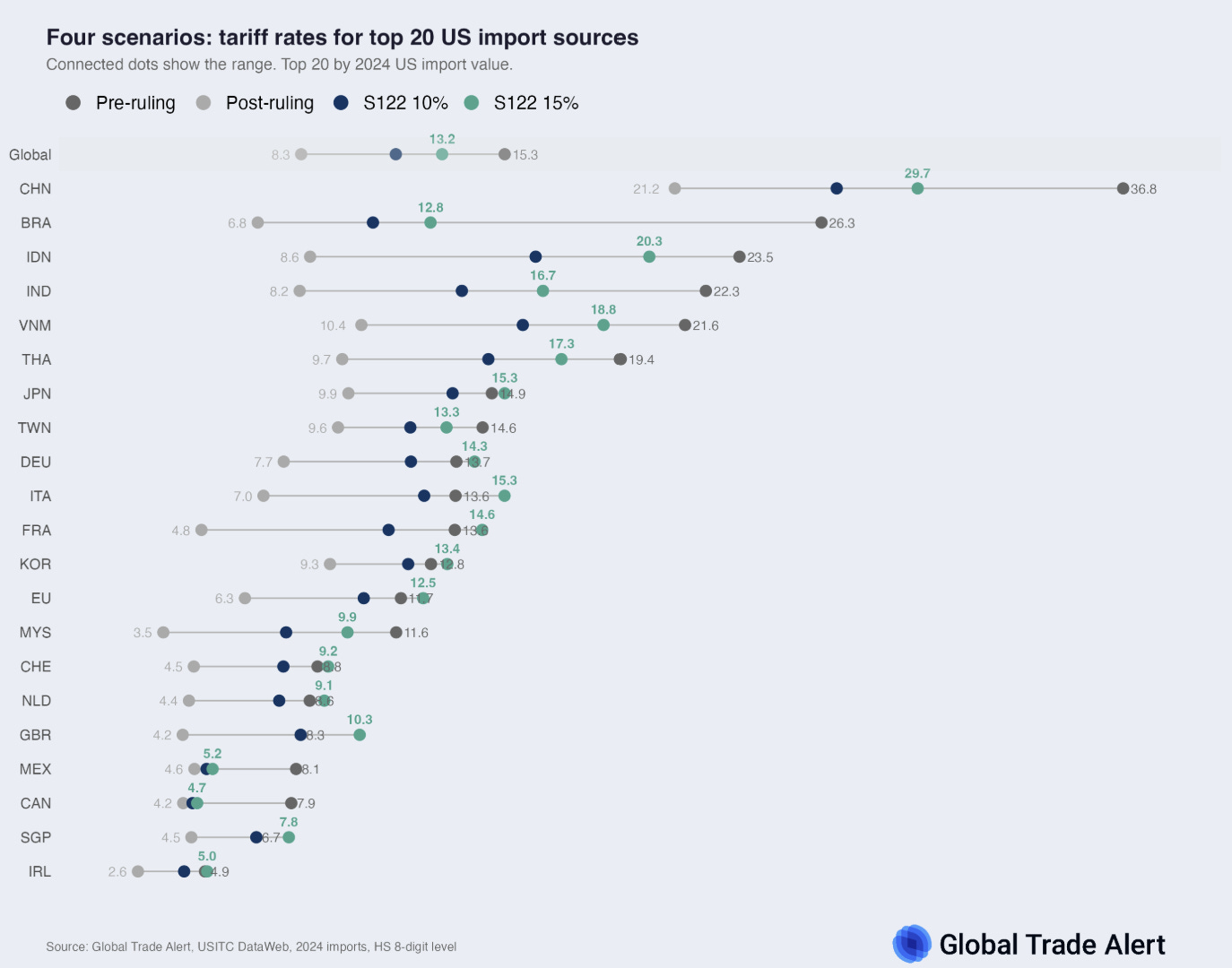

For now, the top beneficiaries are China, which sees its overall tariff rate drop from 37% to 30%, and Brazil which drops from 26% to 13%. Also coming out ahead are Canada, Mexico, India, Indonesia, Vietnam, Thailand, Malaysia, and Taiwan. Other trade partners such as the UK and the EU now face a higher tariff rate than the agreed level.

(chart via Global Trade Alert)

We also will have to wait for the courts to decide on refunds as the justices avoided specifying a remedy, but it is generally assumed they will be disbursed.

Some are trying to spin the Supreme Court move as beneficial for the Administration in that it gives Trump an easy exit from some of the more unpopular measures – Trump had, after all, started to walk back some of the measures most likely to impact inflation, exemptions now cover roughly one third of all US imports, and the trade team was working on a narrowing of steel and aluminium tariffs.

But that feels like a stretch, and the PR victory for tariff opponents will rankle. And the key lever of broad flexibility has been removed from the Administration’s principal negotiating toolbox.

Whatever our views on tariffs, we can breathe a sigh of relief that the erratic flip-flopping on rates by jurisdiction is over. But we can be sure that any slowdown in economic growth or bond market wobbles triggered by deficit concerns will be blamed squarely on the Supreme Court. And that pressure on the Federal Reserve to lower interest rates will intensify.