Trade fragmentation and digital currencies

plus - Markets: getting more comfortable with volatility

“Ideas at first considered outrageous or ridiculous or extreme gradually become what people think they’ve always believed.” – Rebecca Solnit ||

Hi everyone! I hope you’re all taking care of yourselves. It’s almost Friday, and then almost the end of the month and the quarter, and wow I think I need to go and sit down for a bit...

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

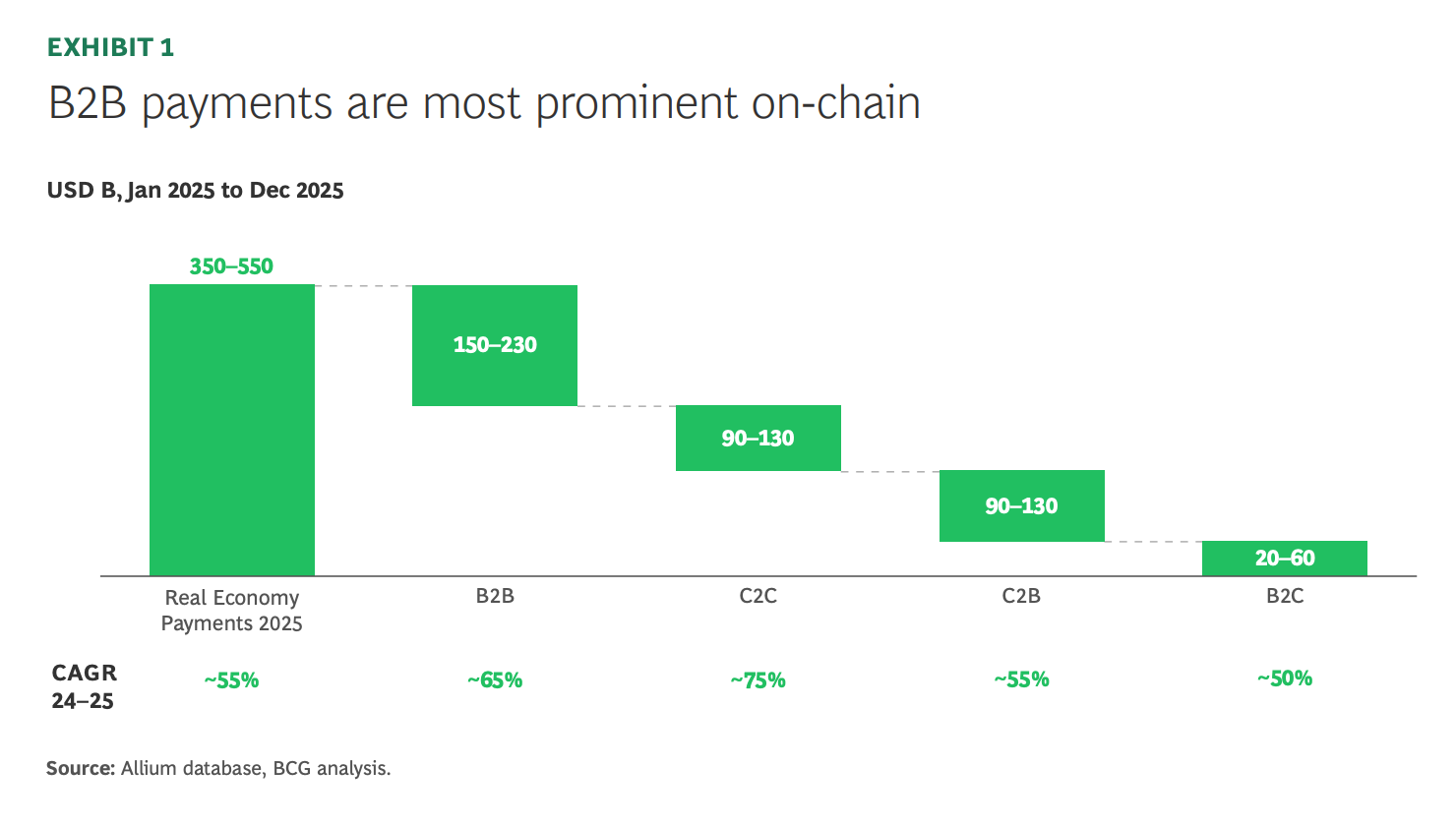

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Trade fragmentation and digital currencies

Markets: getting more comfortable with volatility

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

✨ Use the discount code MACRO for 20% off!

Trade fragmentation and digital currencies

When we say the tectonic plates of geopolitics are shifting, the metaphor has two implications, both different but nevertheless appropriate.

Over aeons, continental drift can move entire land masses across oceans, so smoothly the inhabitants barely notice the gradual climate change.

Or, tectonic plates can crash into each other, creating fire and brimstone and new mountains.

This split metaphor applies aptly to currency trends, specifically to the “dedollarization” many have been mumbling about – there’s the slow drift, and there’s the sharp shocks.

The seeds of the slow shift were sown in the unwinding of Bretton Woods II. To ensure global demand for its now-free-floating currency, the US negotiated with Saudi Arabia the pricing of their oil in dollars in exchange for maintaining security in the Middle East. Other Gulf countries followed and other commodities chose dollar pricing for FX convenience, which rapidly made the US currency the most liquid while US economic growth supported its value relative to others.

In the early 2000s, the world started to notice that the climate felt a bit different: the plates had been shifting. With strong growth in Asian economies and the discovery of American shale, the US was no longer the largest customer of Gulf oil. The emergence of new military powers further weakened the dollar-security relationship in the region, as Gulf states became closer to Pakistan, Russia and others, and the diversification of protectors as well as a greater drive for self-sufficiency accelerated as Saudi Arabia’s relationship with the US deteriorated under President Biden.

Against that background of slow drift, the past few years have brought a few tectonic plate collisions in the global currency balance. There’s never just one particular starting point for a chain of events, but a strong candidate is the West’s reaction to the Russian invasion of Ukraine: seize Russian reserves held in European and US banks, use sanctions to isolate its financial system, and deny it access to international payments where possible.

Nations around the world were jolted out of their complacent assumption that the US would never weaponize the entire global dollar-based network.

Fast forward to the Iran war, which throws into sharp question the original deal of Middle East security in exchange for oil sales based in dollars, and you have yet another catalyst for a rewiring of trade rails.

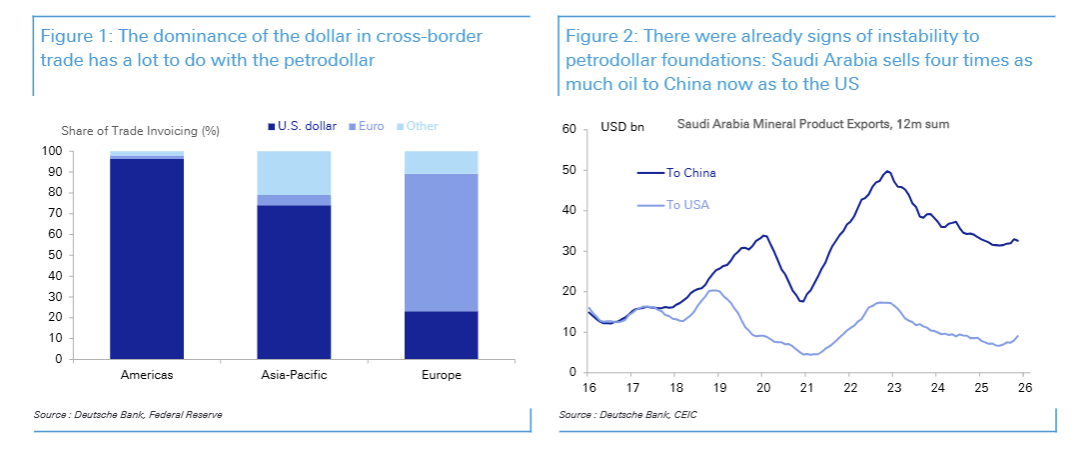

Earlier this week, Deustche Bank published a report on the impact of the Iran War on dollar hegemony that is worth a read.

It notes that there are two main forces chipping way at the regional hegemony of the petrodollar, a key factor in global dollar demand.

One is to do with trading relationships. Over the past couple of decades, as I mentioned above, Middle East oil exports have been swinging away from the US and towards Asia.

(chart via Deutsche Bank)

And reports that Iran is allowing some ships through the Strait of Hormuz if the oil is paid for in yuan highlight that it’s no longer diplomacy or security guarantees that ensure the smooth passage of oil; it’s now down to bilateral agreements which do not need dollar clearing. Iran has promised that, even after hostilities cease, the management of Hormuz will never be the same. It’s also unlikely that either Russia or Iran will ever go back to fully trusting US banks or payment rails.

The other key force the Deutsche Bank report highlights is the shift away from fossil fuels. This has been underway for decades due to concerns about climate change, but is likely to accelerate given renewed concerns about energy security. Not all nations are blessed with sufficient hydrocarbons in the ground; many will have to invest heavily in nuclear and other renewable grids.

This weakens the global dollar demand anchor provided by Middle East energy, and opens the door to new relationships and new payment pathways.

Strangely, the Deutsche Bank team only make one passing reference to the role that digital currencies are likely to play in this shift; they point out that Saudi Arabia is a member of CBDC platform mBridge, along with China, Hong Kong, Thailand and the UAE. But they don’t go further than that, even though a key plank of dedollarization is the underlying plumbing. Using traditional payment rails for global commerce generally implies touching the US-controlled SWIFT messaging system and relying on FX conversion that will often have a dollar leg. The mBridge platform is just one of the emerging alternatives that bypass those potential chokepoints.

Others include:

Saudi Arabia started exploring a digital rial back in 2019;

Russia is moving towards a phased national rollout of its wholesale CBDC in September;

India is due to propose a BRICS CBDC platform later this year;

China has “steady development” of the e-CNY as one of its goals in its latest Five Year Plan;

Europe is making strides on its wholesale and retail version, publicly declaring the goal of reducing dependence on US rails;

I could go on, and probably will in coming weeks, especially as CBDC and national stablecoin frameworks emerge – this is one of the reasons I started this newsletter three-and-a-half years ago. Hong Kong is due to announce its first authorized local stablecoins any day now, further cementing its role as the mainland’s financial and digital sandbox as well as a gateway to global financial markets.

The globalization efficiency of the past few decades is evolving into a more fragmented, bilateral trade map. Blockchain rails are one of the tools building this new world. Not only do they bring a layer of digital efficiency to bilateral trade resistant to third-party interference; but they also set a base for the development of new types of marketplaces for the exchange of tokenized assets, potentially deepening local liquidity and opportunity.

In sum, building payments plumbing resilience is a key step in the rewiring of global trade; it also sets the stage for growth in a more decentralized global market infrastructure and liquidity distribution.