Tuesday, Feb 7, 2023

Two key speeches today highlight the narrative split driving markets: the monetary and the political. Plus, the building retail momentum in stocks and crypto.

“I am not young enough to know everything.” – Oscar Wilde ||

Hi all – I seriously hope that, if any of you have friends or family in Turkey or Syria, they’re ok. So, so awful.

You’re reading the premium daily Crypto is Macro Now newsletter, where I focus on the growing overlap between the crypto and macro ecosystems. Nothing I say is investment advice! Nevertheless, if you find this useful, do share with friends and colleagues.

If you landed here from somewhere other than your inbox, or if this was shared with you, do please consider subscribing to support my work.

Programming note: due to a conflict, I won’t be able to publish this newsletter tomorrow, Wednesday Feb 8, apologies! Thursday’s email will catch you up on key market and crypto news developments.

MARKETS

Two key speeches today: the monetary…

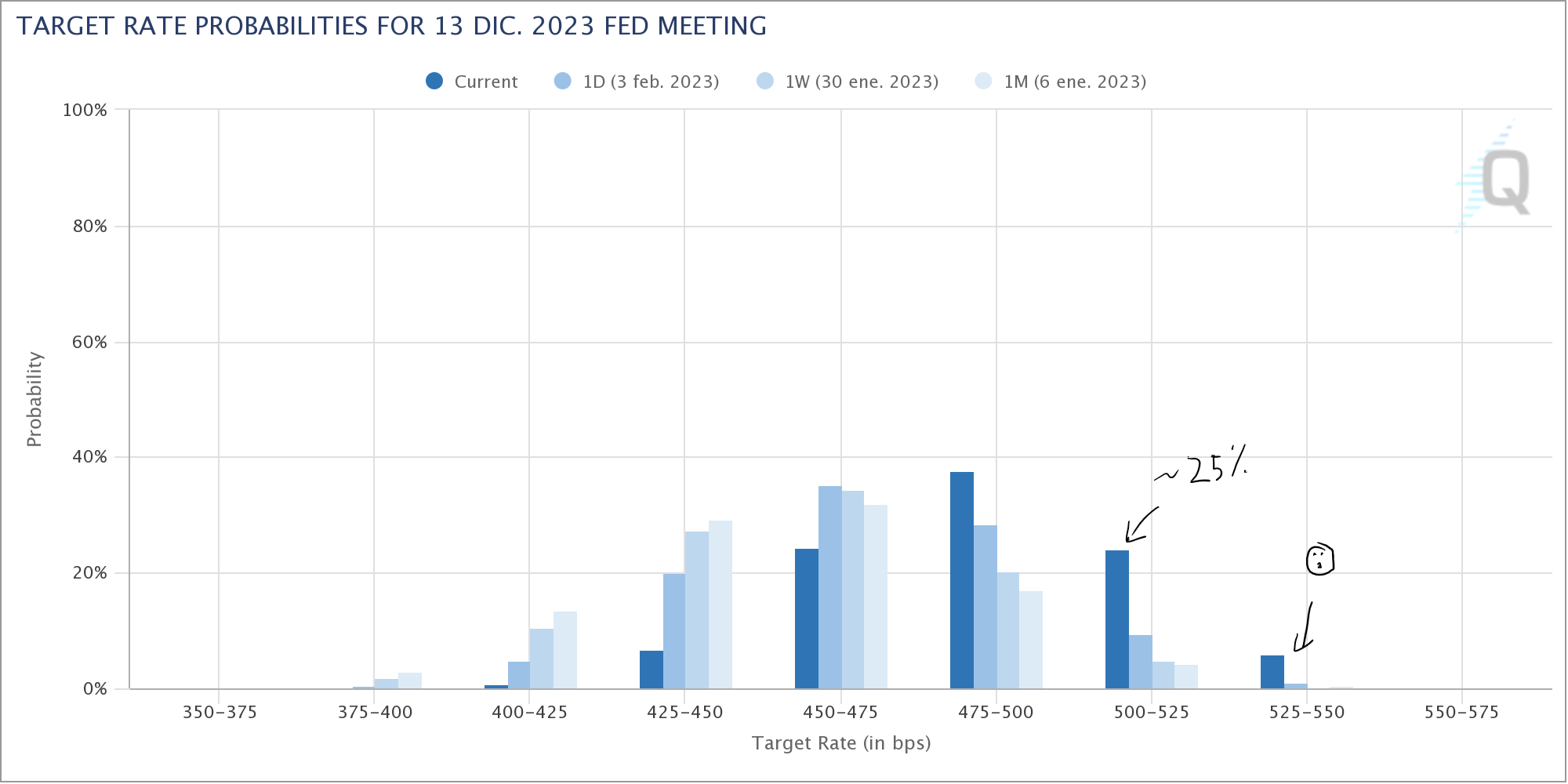

Against a backdrop of rapidly shifting rates expectations, Fed Chair Jerome Powell takes the stage later today at the Economic Club of Washington DC, in his first post-FOMC public appearance. His comments are always scrutinized these days, but these ones will probably be especially so, judging from the sharp moves in yields and futures pricing since last Friday’s strong jobs report broke the prevailing optimism that rate hikes were almost done and cuts were not far away. Now, the market seems to be coming to terms with the idea that the Fed’s official forecast of end-of-year rates at 5.00-5.25% might actually not be too bad an outcome, especially as economists are increasingly saying the quiet part out loud: the official forecast will probably increase. Analysts and investors will be looking for hints of this in today’s comments.

(chart via CME FedWatch, taken yesterday evening)

This chart, from Bloomberg’s John Authers column this morning, highlights the whiplash over the past week, with the grey line representing January’s fed funds expectations curve, the white line showing the curve right after the FOMC meeting, and the blue line drawing the curve yesterday. In my opinion, the curve will move up further. Inflation is not dead, and the Fed sees no reason to cut rates just yet. Even were unemployment to start to move up fast, as I suggested yesterday, it would probably not be fast enough to trigger cuts before the end of the year. And the experience of other countries (such as Spain, France and South Korea last week, Philippines yesterday, Estonia this morning – just some examples of inflation upticks) shows that complacency is misplaced.

(chart via Bloomberg)

In other words, rates expectations are most likely still mispriced.

This doesn’t necessarily mean markets are heading south, however – just yet, anyway. The S&P 500 and Nasdaq continued to slide yesterday, but both are still well above their pre-FOMC levels, suggesting that the walk-back is not yet as adamant as headlines might suggest. This could be down to retail participation. Last week, Bloomberg reported on JPMorgan data that showed approximately 23% of January trading was from retail investors, an even higher percentage than during the meme stock frenzy of 2020. Retail momentum, as we have seen before, does not turn quickly.

(chart from JPMorgan via Bloomberg)