Tuesday, Jan 30, 2024

crypto is NOT yet mainstream, not even Bitcoin - currency turmoil - markets are focusing on the beer in the fridge

"By 2005 or so, it will become clear that the Internet's impact on the economy has been no greater than the fax machine's." – Paul Krugman ||

Hello everyone! I hope you’re all doing well and, seriously, how can it still be January?

You’re reading the daily premium Crypto is Macro Now newsletter, where I look at the growing overlap between the crypto and macro landscapes. There’s also usually some market commentary, but I don’t give trading ideas, and NOTHING I say is investment advice. For full disclosure, I have held the same long positions in BTC and ETH for years, and have no intention to either buy more or sell in the near future.

If you’re not a subscriber, I do hope you’ll consider becoming one! It would help enable me to continue to share what I learn as I work on figuring out where we’re going.

If you find this newsletter useful, would you mind hitting the ❤ button at the bottom? I’m told it boosts the distribution algorithm.

Note: I’m speaking at BlockWorks’ upcoming Digital Asset Summit conference in London on March 18-20. Normally I say no to conferences, but this is one of the very few worth travelling for. If you’re thinking of going, it’d be great to say hi, and here’s a discount code you can use: CIMN10.

IN THIS NEWSLETTER

Markets seem blissfully unaware

Currency turmoil accelerating

No, crypto is not yet “mainstream”

WHAT I’M WATCHING

Markets seem blissfully unaware

With the escalation of the conflict in the Middle East now looking more likely than at any point since the attack on Israel, US markets are eerily cheerful.

The consensus seems to be that the US has to respond to the fatal attack this weekend on US troops by Iran-backed militia (but don’t worry, the Goldilocks promise is that it will be “just tough enough”). And yet, after a brief and mild spike on Sunday night, oil prices have declined.

(chart via TradingView)

It seems that concerns about weakening global demand as China struggles are offsetting any risk to supply chains – so far, physical oil is still moving even if it has to be re-routed. And Saudi Arabia’s decision to delay the expansion of its key oil producer’s capacity is read as a demand rather than a supply signal.

But it’s not so much the risk to supply chains that could push energy prices higher should the US trigger a chain of counter-attacks – it’s that when countries are preparing for conflict, energy demand shoots up as it is one of the deciding factors in who wins. It’s surprising to me that even the possibility of this is not moving trader sentiment.

Meanwhile, US markets appear to be feeling particularly happy, with both bonds and stocks climbing. In part, it’s because economic data is pointing to continued expansion, and earnings reporting has not yet produced any market-moving shocks.

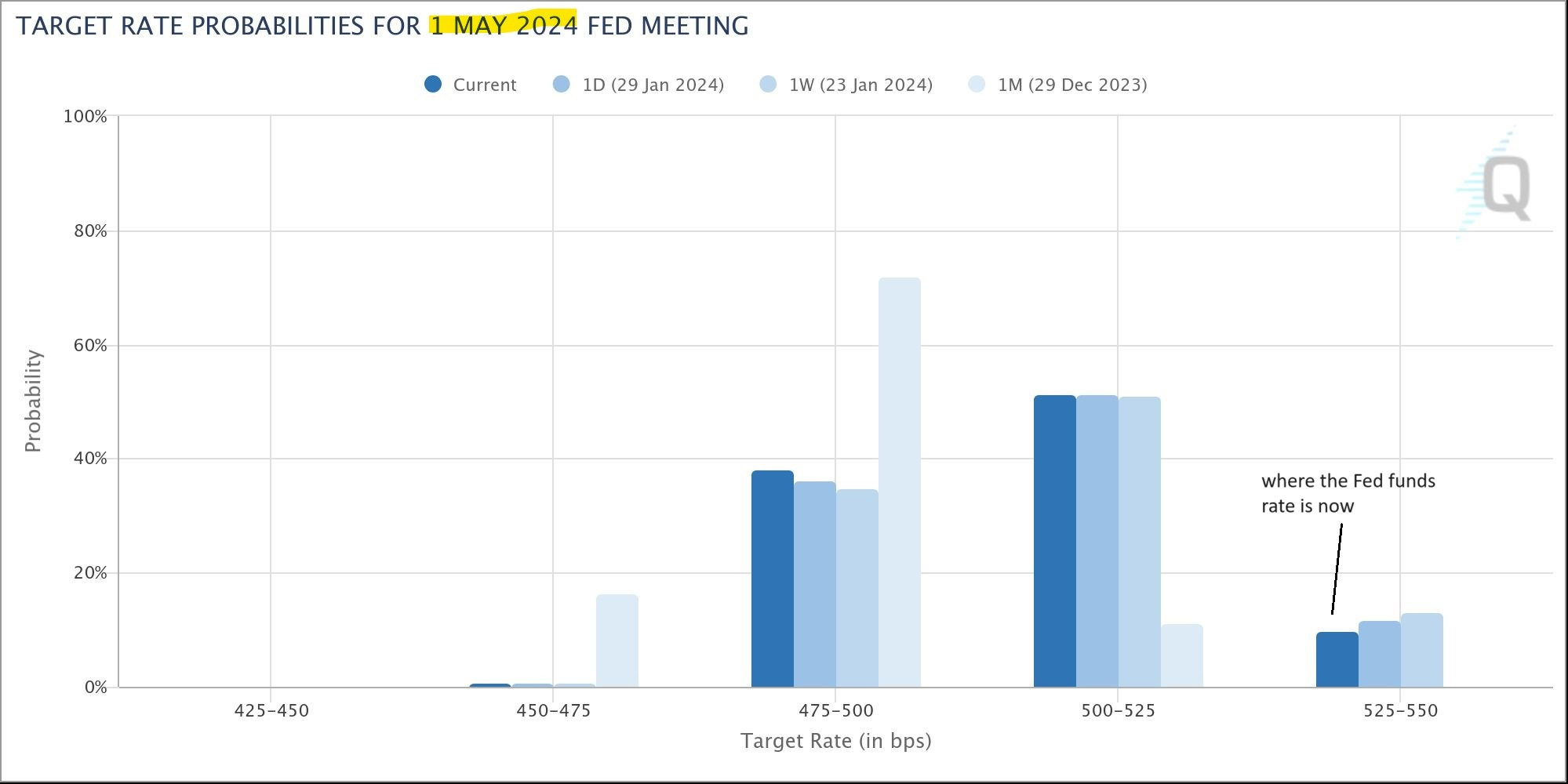

Plus, surely tomorrow Fed Chair Powell will drop strong hints of rate cuts before May, right? Futures markets are pricing in a 90% probability of the first cut at or before the May meeting (I actually and unusually agree with this one, May is likely).

(chart via CME FedWatch)

Also, yesterday the US Treasury announced a surprise cut to its borrowing estimate for Q1, suggesting that there will be less supply of government bonds hitting the market in coming months. Good news for bonds.

This feels fragile, though. Inflationary pressures are hinting at a comeback, even if only from the hike in shipping costs combined with resilient consumers. This morning, we saw Spanish CPI come in notably higher than expected (3.4% year-on-year vs 3.1% previous and expected), and EU consumer inflation expectations are climbing.

(chart via @pboockvar)

This week we hear from Microsoft, Alphabet, Apple, Amazon and Meta, so there could be more bullishness ahead for tech earnings expectations. But what about for the other 100+ companies reporting?

And if conflict in the Middle East does escalate, does anyone think the current Treasury borrowing estimate will hold? True, maybe geopolitical tension will remain at a sinister simmer rather than move to a boil. But the risk is non-zero, and does not seem to be factored in.

You’ve seen those scary made-for-TV movies when you know there’s a killer hiding behind the curtains but the unaware executive has just arrived home and is happily grabbing a beer from the fridge? This feels a bit like that.

Currency turmoil accelerating

Regular readers are possibly tired of me talking about greater global interest in digital hedges such as bitcoin and stablecoins as a result of increased currency turmoil. Bitcoin may be relatively volatile, but that doesn’t matter much to those stuck with rapidly depreciating currencies. And stablecoins may be more centralized and with lower upside, but that doesn’t matter much to those desperate for dollars and wary of financial censorship.

Well, signs are picking up that things are getting particularly shaky in way too many countries. Here’s a selection of headlines I’ve seen on Bloomberg so far today (emphasis mine):