Wednesday, Jan 17, 2024

Fed vs fiscal vs risk, economic signals, support for democracy

“Seek simplicity, and distrust it.” – Alfred North Whitehead ||

Hello everyone! Today’s email is later than usual due to a schedule issue, sorry!

You’re reading the daily premium Crypto is Macro Now newsletter, where I look at the growing overlap between the crypto and macro landscapes. There’s also usually some market commentary, but I don’t give trading ideas, and NOTHING I say is investment advice. For full disclosure, I have held the same long positions in BTC and ETH for years, and have no intention to either buy more or sell in the near future.

If you’re not a subscriber, I do hope you’ll consider becoming one! It would help enable me to continue to share what I learn as I work on figuring out where we’re going.

If you find this newsletter useful, would you mind hitting the ❤ button at the bottom? I’m told it boosts the distribution algorithm.

IN THIS NEWSLETTER:

Was it Waller’s words that moved rates expectations?

The global economy can breathe a bit easier

Africa’s faith in democracy: a bumpy road ahead

WHAT I’M WATCHING:

Was it Waller’s words that moved rates expectations?

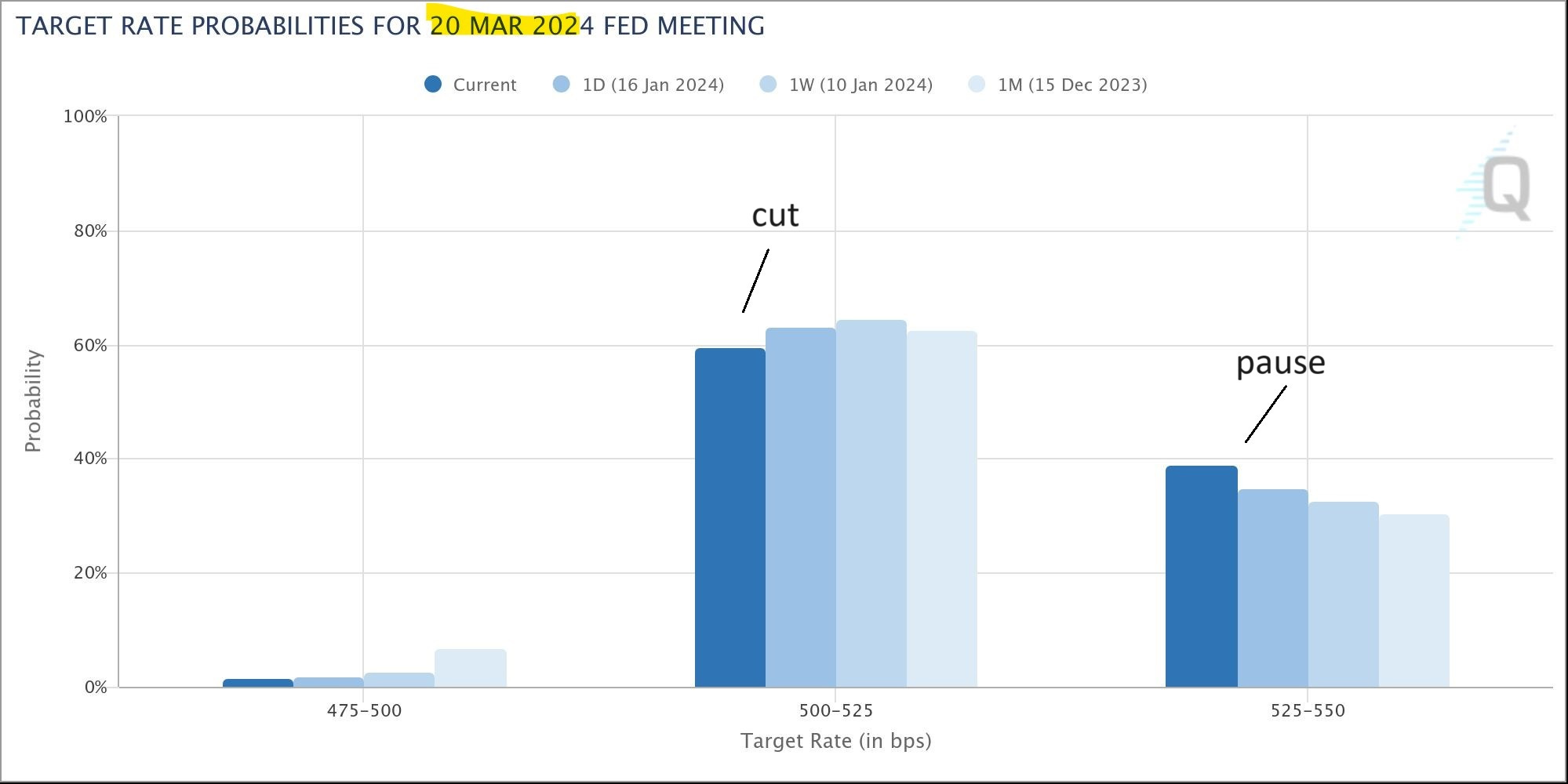

Rate expectations are on the move. The probability of the first rate cut coming in or before the 20th of March has moved from almost 90% at the beginning of the year (not reflected in the chart below, which shows the move from a day, a week and a month), to a more reasonable (but still too high) 60% now.

(chart via CME FedWatch)

This is largely being attributed to comments from Federal Reserve Governor Waller in a virtual speech yesterday, in which he said rate cuts this year were very likely, but that there was “no reason to move as quickly or cut as rapidly as in the past”. This reinforces what other Fed officials have been saying, that March is too soon, but for some reason the market appeared to take Waller more seriously than it has similar comments by his colleagues.

Only, I don’t think it’s Waller that is moving the rates expectations here.

Ok, maybe partly – his comments were detailed, and his role as a governor rather than a regional central bank president could give them extra weight.

However, I think the bigger impact comes from Trump’s win in Iowa.

There are several forces at work here:

1) One is the likely flood of bond issuance under a Trump administration to cover a widening deficit. Trump has said that he would like to make permanent the individual tax cuts he introduced in 2017, which are set to expire in 2025. And on the campaign trail, he has often said he will cut taxes even further.

He has reportedly promised to “unilaterally” cut government spending, although the wiggle room here is limited, especially if domestic and geopolitical tensions increase. And lower government spending could lead to lower economic activity and tax revenue, increasing the deficit even further.