Wednesday, Mar 8, 2023

50bp still not likely but market understandably nervous, Grayscale-related optimism could be misplaced, and more

“Strong women don’t have ‘attitudes’, we have standards.” – Marilyn Monroe ||

Hi all, and happy International Women’s Day to all my readers! You’re reading the premium daily Crypto is Macro Now newsletter, where I focus on the growing overlap between the crypto and macro ecosystems – I’m glad you’re here. Nothing I say is investment advice! Nevertheless, I hope you find it useful – if so, please consider liking, and sharing with friends and colleagues.

If you landed here from somewhere other than your inbox, or if this was shared with you, I hope you’ll think about subscribing to support my work (or try a free trial!). It would make my day.

MARKETS

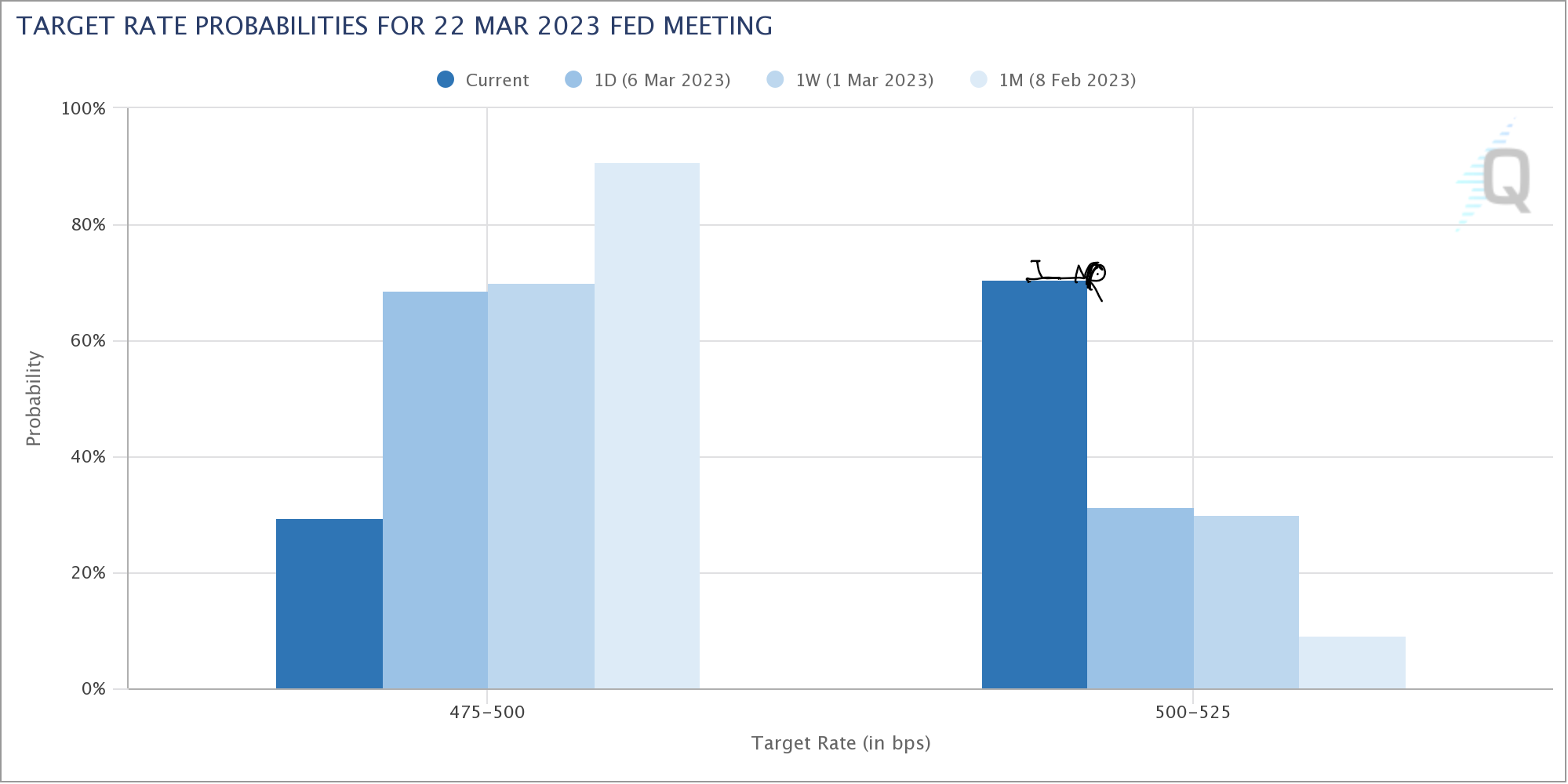

Well, that was a flip. Powell’s testimony yesterday in front of the Senate Banking Committee had a greater impact on markets than his recent FOMC press conferences have, and sent expectations of a 50bp hike in a couple of weeks flying up. Yesterday, CME futures-priced probabilities were pointing to 70/30 odds in favor of 25bp vs 50bp – today, the odds have reversed, with the market pricing for a 70% probability the hike will be a big one.

(chart via CME FedWatch)

I can understand the reasoning. As I mentioned yesterday, the recent pickup in inflationary pressure in sectors that are supposed to be particularly sensitive to interest rates is sending signals that interest rate hikes aren’t working. Obviously, this is because they’re not doing enough of them, right? If the nail won’t go into the wall, it must be because the hammer isn’t big enough. (Yes, I’m being sarcastic – just because I understand the reasoning, doesn’t mean I agree with it.)

Markets were startled by the conviction behind Powell’s comments. The S&P 500 dropped sharply on the open and continued to bump its way downward for the rest of the day, ending more than 1.5% below the Monday close. Yields headed up, with the US 2-year treasury breaching 5.00% for the first time since 2006. BTC had been heading down all morning, but the drop became more aggressive as the hearing kicked off, with the price briefly dipping below $22,000 for the first time since mid-February.

(chart via TradingView)

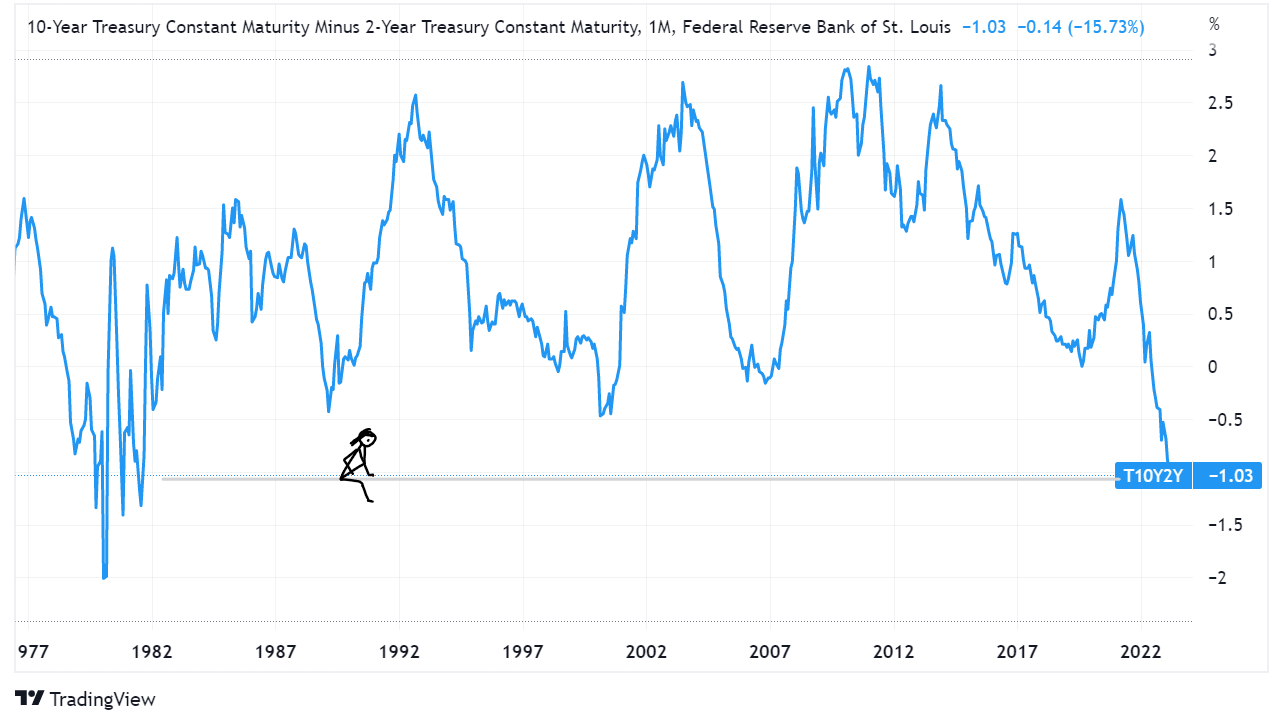

This all feels particularly volatile. The 10yr2yr spread dipped below 100bp for the first time since 1981. This doesn’t necessarily imply a steeper recession, but it does signal that something is very off in monetary expectations.

(chart via TradingView)

Terminal rate is now being priced at 5.64%, and the jump in the implied policy rate for the next year, since just over a month ago, is staggering:

(chart via Bloomberg)

I can appreciate the messaging value in a “proactive” Fed that will “do what it takes” to get inflation down, but I still maintain that moving back to 50bp hikes would be risky for the following reasons:

While the Fed would sell the decision as “reacting to the data”, the market could take it as “panicked”, especially since the Fed itself has been reminding us that data responds with a lag.

As well as panic, it could deliver a further blow to Fed credibility. Powell uttered the word “disinflation” 11 times in his last FOMC press conference. Bumping the pace of rate increases now would send a strong message that, again, he realizes he was wrong. That in itself is not bad (hey, we all make mistakes), but when the bulk of the Fed chair’s job is messaging, it casts a cloud over future pronouncements.

Sharp hikes boost volatility, as we saw last year. The MOVE index, which tracks volatility in the US treasury market, has been climbing rapidly over the past few days and is now at its highest point since December of last year. Higher volatility for assets that are supposed to be the safest in the world is not exactly a vote of confidence.

(chart via TradingView)

What’s more, Powell’s comments did not deviate from what he has been saying all along: higher for longer, and if we need to accelerate, we will. Admittedly, his sentences were more blunt than usual, so perhaps that’s what it takes to drive a message home in this persistently optimistic market.

This creates another problem: given the dramatic shift in market expectations, if the next FOMC meeting produces only a 25bp hike, there could be a strong surge in indices and asset prices, creating a “feel good” effect that could keep inflation higher. That is not at all what the Fed wants, but nor are they likely to let the market dictate their strategy.