WEEKLY, April 27, 2024

stablecoin mainstreaming, suing the SEC, crypto in South Africa

Hi everyone! I hope you’re all doing well, and have good things planned for the weekend.

You’re reading the free weekly version of Crypto is Macro Now, where I reshare/update a couple of the articles from the week.

If you’re a premium subscriber, you’ve probably already read them, so feel free to scroll all the way down for some non-crypto links. If you’re not a premium subscriber, I do hope you’ll consider becoming one! You’ll get ~daily insight into the growing overlap between the crypto and macro landscapes, as well as some useful links. And there’s a free trial!

Feel free to share this with friends and family, and if you like this newsletter, do please hit the ❤ button at the bottom.

In this newsletter:

A stablecoin snapshot

Stripe and stablecoins

Suing the SEC

Crypto in South Africa: big steps

Some of the topics discussed this week:

Whoa, those BTC fees

Upcoming catalysts: Hong Kong, SAB 121 and more…

Spot ETH ETFs: finally some movement (but not much)

Venezuela and stablecoins

Is it rates and inflation concerns? Or geopolitical risk?

Inflation heading up

GDP ouch

A stablecoin snapshot

Visa (yes, Visa!) has launched a stablecoin dashboard, which shows the outstanding supply of fiat-backed tokens at an all-time high, with USDT easily dominating.

(chart via Visa Onchain Analytics)

But, here’s an interesting twist: transaction volume in USDC is higher than that in USDT.

(chart via Visa Onchain Analytics)

This could be because USDT is more held outside the US as a dollar-based store of value, while the USDC is used in the US as a transaction currency.

Another interesting detail? The monthly transaction volume of fiat-backed stablecoins – $2.6 trillion – is double the average monthly transaction volume of Visa in Q4 2023 (the latest data I could find).

The above chart also tells us that transaction volumes in Paxos’ stablecoin USDP and PayPal’s PYUSD is still negligible (you need a powerful magnifying glass to see their bars).

Remember when PYUSD launched, how PayPal’s brand name and extensive network would make the token a rival to USDC? Well, it turns out that getting traction is harder than it seems, especially if users tend to distrust PayPal’s political neutrality. In 2022, it took some deserved heat for deplatforming certain journalists and alternative media sites for their nonconformist views. This understandably did not help its crypto standing, and non-crypto users don’t really need its stablecoin. For tradfi giants trying to break into crypto, brand and network will only get you so far.

Stripe and stablecoins

This is no doubt something that PayPal’s closest competitor Stripe has been thinking about. Earlier this week, it announced that within a few weeks it will enable stablecoin payments. If PayPal’s stablecoin initiative hasn’t really worked, will Stripe’s?

To start, Stripe is not issuing its own stablecoin. It plans to support USDC transfers on Ethereum, Solana and Polygon chains.

While Stripe has not (to my knowledge) been accused of deplatforming for political reasons, it did win the resentment of digital asset natives in 2018 by suspending Bitcoin payment support. But still, that was a while ago, and is more understandable given BTC’s volatility. “It’s not personal, it’s strictly business.”

The plan is for stablecoin payments to settle instantly in fiat, making the process seamless for merchants. If the service is rolled out across the whole network, this will open up online commerce to people without bank accounts in 46 countries. I’ve been asked how people would buy USDC in the first place if they don’t have a bank account (this question only ever comes from those living in privileged financial jurisdictions). In marketplaces around the world, there is usually someone with a makeshift stall that can take your cash and in exchange transfer you USDC, BTC, etc. Or if not a stall in a marketplace, someone has a designated stool in a local bar.

One of the main barriers to greater use for crypto assets as payment tokens has been the lack of merchant choice, and typically it has been a hassle for merchants to get set up to accept crypto. Those that did, often didn’t see enough demand to make it worth the hassle and word got out. Now, merchants pretty much don’t have to do anything.

From what I gather, USDC holders can now make payments at any of the hundreds of thousands of merchants that use Stripe.

This will take some time to roll out, and it’s unclear as to what the initial reach and pick-up will be, but watch those USDC volumes.

Suing the SEC

Bring it.

In February, the Crypto Freedom Alliance of Texas together with crypto firm Lejilex sued the SEC for overstepping its jurisdiction, arguing that trading pre-existing tokens does not necessarily make exchanges securities dealers.

In March, the DeFi Education Fund and apparel company Beba sued the SEC in the hopes of getting a judge to insist the SEC respect the Administrative Procedure Act (which mandates public input on sweeping new rules), and to declare that a token airdrop is not a security.

Earlier this week, the Blockchain Association and the Crypto Freedom Alliance of Texas sued the SEC over a new rule adopted in February (known as the “dealer rule”) which would, among other things, require DeFi apps to register as broker-dealers. The compliance deadline is in roughly a year. The associations argue that the SEC has over-reached on this rule, that the measure is “arbitrary and capricious” as well as unworkable (how does decentralized software register for anything?).

A couple of days later, Ethereum lab Consensys sued the SEC in a push-back against what looks like SEC intention to regulate ETH as a security. In its complaint, Consensys disclosed that the SEC had sent the Ethereum developer a Wells notice – among the SEC’s accusations are that Consensys is an unregistered securities dealer because of transactions run through the MetaMask interface, and that the firm’s purchase and sale of ETH from its treasury are securities transactions. It was also known that the SEC had been investigating the Ethereum foundation and other ecosystem participants.

The move, and the confirmation of the pending SEC action against Consensys, did not impact ETH much, suggesting that traders are not taking the ETH-is-a-security threat from the SEC very seriously – ETH’s value relative to that of BTC has been more or less steady for the past few days.

(chart via TradingView)

A likely outcome from this suit is that we get a court decision on whether or not ETH is a security – or, at the very least, a judicial order for the SEC to finally clarify its criteria.

This is definitely a different mood. The crypto ecosystem, considerably wealthier than last year now that prices have rallied, is taking the battle to the SEC, and counting on at least some courts seeing reason and curtailing the SEC’s reach while forcing it to deliver some regulatory clarity and manageable processes. The SEC, on the other hand, is stretched in terms of resources, has suffered some embarrassing losses in courts, and is under public pressure from both crypto and Wall Street for its egregious rule-making approach and hostility toward innovation.

The crypto industry is unlikely to win all the outstanding suits – but it will probably win some of them, especially given the calibre of the lawyers involved. This calibre extends not just to those directly retained, but also to the seriously impressive legal minds lending support to the notion that political prejudice should not cloud rulemaking from unelected officials and that rationality and reason have to eventually prevail.

Crypto in South Africa: big steps

Earlier this week, South Africa’s Financial Sector Conduct Authority (FSCA) published an updated list of the number of businesses granted crypto asset service provider licenses, with new additions in April bringing the total number to 75. This may sound like a lot – and it is. After all, Hong Kong only has two. But South Africa is a much larger country (population of almost 60 million compared to Hong Kong’s 7.3 million). Even so, basic math shows a much higher concentration of crypto service businesses in South Africa than in Hong Kong, even taking into account the latter’s role as an Asian financial hub.

Even more startling, the FSCA disclosed that it had received a total of 374 applications. I confess I’m confused about the UK’s numbers (does anyone reading this have the definitive data?), but one report I saw said that the UK’s FCA received 28 applications in 2023, of which it approved four.

One takeaway from this is that there is a lot of grassroots interest in crypto currencies in South Africa.

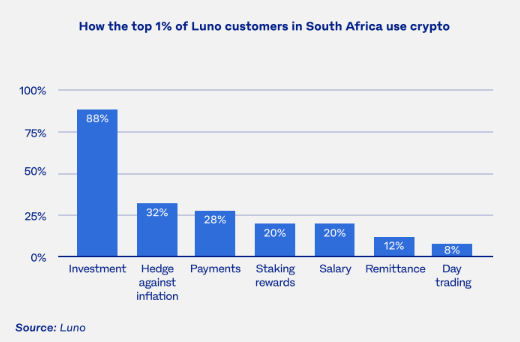

What’s more, it seems that crypto market participants on the continent are not just in it for the trading gains. A survey published this week by crypto exchange Luno (on South Africa’s list of approved digital asset service providers) showed that, at least among Luno clients, the main use case is “investment” – that is, holders with a longer-term time horizon.

(chart via Luno)

Of course, crypto markets vary widely, even within Sub-Saharan Africa. The average holding period for a Luno user in South Africa, for example, is almost double that of a user in Nigeria, suggesting that the Nigerian crypto market is more trading- and/or transaction-oriented.

(chart via Luno)

The report also confirms that the US listing of BTC spot ETFs triggered a wave of interest around the world, with a spike in Google searches in South Africa.

(chart via Luno)

With all that, the emerging regulated crypto space in one of Africa’s largest economies signals more than strong grassroots interest – it strongly suggests that institutions will start to get more involved, encouraging more market participation and continued progress in its sophistication.

HAVE A GREAT WEEKEND!

I haven’t done podcast recommendations in a while (other than the individual episodes I mention in the daily email). The range and depth of what’s out there these days is astonishing, but because there is so much, it can be hard to find quality, quirky listens that are consistently good.

Since it’s the weekend and we should all be taking a mental break, I’m going to share three of my that have nothing at all to do with crypto, macro, geopolitics or media:

On The Rest is History podcast, Tom Holland and Dominic Sandbrook have an infectious amount of fun while diving deep into topics such as disco, Lord Byron, the Titanic, chocolate, Carthage and I could go on. I’m not a history buff at all, but this manages to be mind-bending and wholesome at the same time.

Here's an odd one that’s strangely satisfying: Air Traffic Out of Control. It shares snippets of conversations between pilots and air traffic control, and the takeaway is always the impressive calm, control and attention to detail during emergencies.

The Sporkful is a food podcast that avoids the trap so many others fall into, of sounding reverent and superior. It focuses on eating more than on ingredients, will make you want to both laugh and clean out your fridge, and mixes up formats so things don’t get stale (food pun? I guess).

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade.