WEEKLY, Jan 7, 2023

Hello everyone! For those who are not premium subscribers (whom I said hello to earlier in the week), HAPPY NEW YEAR! May this year bring you many joys, big and small. And for those of you who are new here, you’re reading the free weekly Crypto is Macro Now newsletter, where I look at markets and narrative shifts that shape how our industry interacts with the macro economy.

The premium daily version of this newsletter dives deeper into market drivers and news that highlight the growing overlap between the crypto and macro ecosystems. I never give investment advice, nor will you see protocol reviews or app recommendations. You will get insight into how crypto is impacting the world we live in, and where this could lead. If you’re interested in keeping up with shifts in adoption, regulation and perception, I hope you’ll consider subscribing.

Some of the topics discussed this week:

The growing consensus around a US recession in 2023

What a recession could mean for crypto markets

Blockchain in space is not the punchline it may seem

Crypto “deposits” vs “purchases”

BTC vs gold

You’ll find some changes to the usual format in this issue – I need to make it shorter, so I’ll be tweaking the section content. Open to feedback!

MARKETS

Steady markets

With the new year getting of to a dramatic start in the crypto market infrastructure industry – significant layoffs at Silvergate, Genesis, Huobi and others, not to mention the wind-down of DCG subsidiary HQ Digital and the SEC/DOJ investigation – it’s notable that BTC has held relatively steady.

(chart via TradingView)

This lack of movement in the face of really bad news for the sector can be seen in the unusually low volatility levels. The BVOL index, which tracks 30-day rolling realized volatility, just keeps on dropping and is now at its lowest level ever.

(chart via TradingView)

Low volatility may seem like a plus for longer-term value traders as well as those that hope to develop bitcoin’s use cases, but it is both a symptom and cause of traders staying out of the market. This is not great for BTC’s outlook in that traders make the market more liquid and more lively, accounting for the bulk of on-chain movements as well as off-chain exchange moves. The below chart shows that over 65% of BTC that moves on any given day was last moved less than 24 hours before

(chart via glassnode)

The relatively weak trader interest can also be seen in the derivatives markets, with the steep drop in futures volumes for the month of December for both BTC and ETH, and the decline in (BTC) and weak growth (ETH) in futures open interest.

Recession consensus

2023 has kicked off – no surprise – with a slew of economic doom and gloom from official organizations, with the IMF’s Managing Director Kristalina Georgieva warning earlier this week a “tough year” in which one third of the world’s economy will enter recession. Only one third? It seems a given that Europe will face a recession this year, with even the Bank of England departing from the usual spin to predict dire times for the UK. Europe including the UK contributed over 16% of global GDP in 2021 accounting for informal economies, according to World Economics, almost 22% according to other estimates. Consensus (see below) is also increasingly pointing to a looming recession in the US, which contributed almost 14% of global GDP according to World Economics – other estimates have it at almost 25%. So, even with just these two blocks we’re at 30% or 47%, depending on your preferred measure, and this is not accounting for China (around 18% of the global economy), Russia or the myriad developing countries that are struggling to meet debt payments and attract further private investment.

There are, of course, many wild cards in that calculation, and a recession in the US might – just might – be avoided if the consumer remains strong while inflation decelerates. A recession probability index based on employment, industrial production, personal income and trade that has correctly reflected all previous recessions going back to 1970 has barely registered an uptick.

(chart via the Federal Reserve of St. Louis)

The signs that the US is in one are not yet clear – GDP growth in Q3 was positive (+3.2%), the Atlanta Fed (recently pretty accurate) predicts Q4 growth of +3.8%, and employment as well as consumer sentiment are still relatively strong. This week’s official US non-farm payroll report for December showed a persistent (albeit shrinking) increase in employment combined with a slight deceleration in wage growth, reigniting the “soft landing” thesis. The Eurozone showed December inflation moderating at a faster-than-expected pace, and manufacturing PMI for the month recovered slightly.

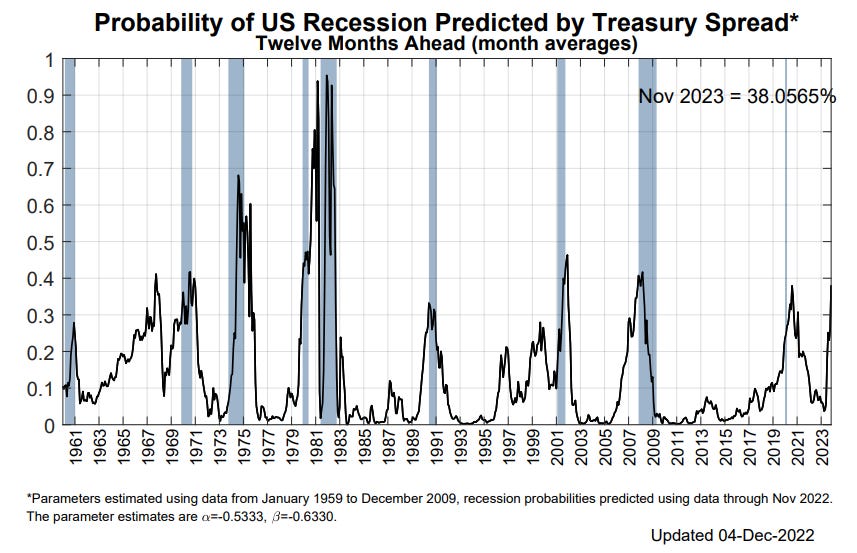

But other indicators, such as that of the New York Federal Reserve recession indicator, based on the 10y3m spread, is signaling a 38% probability of a US recession by November of 2023 (in that every other instance except 1967, the probability reaching that level meant a recession was either under way or close at hand).

(chart via the New York Fed)

Others are even more pessimistic. The Conference Board expects assigns a 96% probability to a US recession starting in Q1 2023. And earlier this week, Bloomberg published a roundup of calls from 500 Wall Street strategists (I didn’t realize there were so many!), which makes for depressing reading. Plus, the yield curve inversions (pick any, all the meaningful ones are at extreme levels) tell us that, without a doubt, a recession is coming.

Oil and inflation

This expectation can also be seen in the oil price which, all else being equal, should be rising given uncertainty about supply. The unusually warm winter weather in Europe has softened the immediate threat of shortages, but the result of Russian political maneuvering around the G7-imposed price cap has yet to be clarified and the re-opening of China should, in theory, boost demand.

However, a global recession will dampen overall energy needs, and China’s reopening has so far been bumpy as Covid races through the population and countries scramble to implement travel restrictions. The current slump in WTI prices (for example) – down to levels well below those just prior to the Ukraine invasion – reflects forward economic expectations. These in turn should feed through to headline figures, possibly reinforcing glimmers of optimism.

(chart via TradingView)

It’s a complicated stage at the moment, with conflicting plot lines, shifting roles and an unsure ending. The oil price is a key metric to watch in that it embodies economic forecasts as well as geopolitical tensions and national policy, and can give hints as to which of the many narrative drivers is predominant at any given time.

COLUMN

A New Philosophy of Markets: Assets That Embody Technology

One thing crystallized for me over the holidays that sheds light on why the crypto industry has been getting so much “bah, told you it was all worthless” dismissal from mainstream sceptics. It should have been obvious sooner, but – just like we can’t detect the earth’s rotation when we’re standing on it – I did not fully appreciate how much public perception of crypto had shifted since the last time prices were bouncing along cyclical lows. Back then, crypto was a new type of money, a global computer, an engagement incentive, a governance value. Now, in the eyes of the mainstream, crypto is a market.

Like many of you, I expect, I spent part of the end-of-year break explaining to family and friends that, no, crypto was not “over”. I puzzled for a while over the extent of this misconception, until it clicked: It’s not that the crypto market got financialized – we all know that, just as we all recognize the damage done to perception and sentiment by the collapse of some of the main architects and beneficiaries of that financialization.

It’s more that crypto became just a market for most casual observers. That’s all, just a market. And with the market in dire straits, well, obviously there’s no longer any point to the whole concept.

Looking back, it’s not hard to see how this shift happened. The increasing levels of institutional interest (Goldman Sachs! Fidelity! Blackrock!), prices (up 20% in a day! down 80% year-to-date!), scams (rug pull! exploit!) and regulatory concern (protect investors! protect the financial system!) fuelled headlines that grabbed attention, incentivizing more stories along the same vein. The power of repetition as mainstream media coverage of the industry broadened cemented the association of “crypto” with “risky”.

I’m not pointing the finger at media – many publications have done a great job of also surfacing the more transformative aspects of our industry. But perception tends to latch on to what it can grasp, and the “public” (generalizing here) is familiar with markets, whereas it doesn’t necessarily understand Merkle trees. Price moves are easier to visualize than consensus algorithms. And the power of institutional signalling is more relatable than weighted decentralized liquidity pools. The markets narrative is stickier than the tech narrative because it is more comfortable. The risk narrative is stickier than the innovation narrative because drama is better at grabbing our attention.

The instinctive reaction here, then, is to vow to start focusing more on the technology angles of crypto – I and many others have argued for that elsewhere. But, while that is still the case, there’s another fundamental aspect of crypto evolution that has been largely overlooked.

We know that crypto assets are both speculative and investment opportunities. We also know that they represent radical new technologies. We can acknowledge that they are all those at the same time. What is harder to wrap our heads around is that the asset is the technology.

For the first time in our history, we have tradeable assets that embody innovation. Sure, investors can get exposure to progress through equities or ETFs, but they are formulaic wrappers around potential earnings streams that only become available to the public long after the innovation is first tested.

Amazon, for example, was founded in 1994 and scrabbled together a start-up existence for three years before offering the public the opportunity to speculate. Facebook was founded in 2004, but didn’t offer a tradeable asset to represent a bet on its potential until 2012. Both were considered extremely risky in their early pre-IPO days, too much so for mainstream investors. And both were extremely volatile at launch and for some time after.

Yet even those examples are not exactly comparable. Amazon and Facebook are not new technologies, they represent a new use of a technology. And both have frequently, and especially in recent weeks, seen their values buffeted by corporate decisions and fiat economy-based earnings outlooks. Bitcoin, ether and others are the new technology. Technically, they are assets that move on new rails – but neither the assets nor the rails work or have value without the other. Plus, there is no earnings risk stemming from strategic decisions taken behind closed doors or from difficult economic conditions. It’s as if you had a chance to buy stock in the internet in 1985 that gave you pure exposure to its adoption, with no corporation risk.

What’s more, crypto assets open up support for innovation unlike any other tradeable vehicle to date. They are pure technology plays that anyone, anywhere can invest in, without having to prove a certain amount of wealth for early access. They are risky, yes, but new concepts usually are, and education as well as platform disclosure rules could offer some protection without erecting inequality-enhancing barriers.

Crypto is so much more than a market. It is also so much more than a new technology. It is a new way of thinking about value, risk, funding and engagement. It adds a jugful of philosophy to the soup of finance, garnishes it with a few dashes of ingenious code and a sprinkle of hype, and stirs it up to get a whole new flavour of evolution.

Maybe this year we can do better at getting that message across. Maybe, with that, we will earn a more thoughtful type of criticism as well as a more nuanced approach to regulation. And, in thinking more about the messaging, perhaps even those of us in the industry can face the next cycle with fortified conviction that what we’re working on matters, probably more than most of us realize.

Good reads

Arthur Hayes continues his sweeping arc of how we got “here” – powerful stuff, with an eye-opening map.

Tyler Cowen offers some excellent points in this editorial that effectively highlights why regulators don’t need to (and shouldn’t) clamp down on the crypto industry.

Thomas Fazi reviews Rana Foroohar’s latest book on the benefits of “deglobalization” while making several strong points of his own regarding the swinging pendulum.

Podcast: The latest episode of Stephanomics lends some nuance to the US-China relationship, and has some insight into the contentious push for global standards

Have a good weekend!

As we say goodbye to the seasonal celebrations (which continue until the 6th of January where I live, with the visit of the three kings bringing gifts), I feel compelled to share with you some photos of just how gorgeous my home city of Madrid is over the holiday season. You may think of siestas or sangria when you think of Spain, and Madrid has a well-earned reputation for late dinners and friendly bars, but I can assure you that in December it absolutely sparkles. There’s nowhere I’d rather be for the most festive month of the year.

Can’t wait for Global Liquidity to return ... all risk assets are fish out of water especially Crypto