WEEKLY, March 30, 2024

the spread of crypto ETFs, more mainstream misunderstandings

Hi everyone! I hope you’re all enjoying the long Easter weekend, I know I am. Heading out this morning to get stuff to organize my kitchen – not everyone’s idea of fun, sure, but if you know, you know.

You’re reading the free weekly version of Crypto is Macro Now, where I reshare/update a couple of the articles from the week.

If you’re a premium subscriber, you’ve probably already read them, so feel free to scroll all the way down for some non-crypto links. If you’re not a premium subscriber, I do hope you’ll consider becoming one! You’ll get ~daily insight into the growing overlap between the crypto and macro landscapes, as well as some useful links, and (usually!) access to an audio read of the content. And there’s a free trial!

Feel free to share this with friends and family, and if you like this newsletter, do please hit the ❤ button at the bottom.

Programming note: the premium daily will be taking Monday off for the Easter holiday, back on Tuesday!

In this newsletter:

The spread of spot crypto ETFs

“Crypto is no longer decentralized”: Yet another mainstream myth

Some of the topics discussed this week:

ETH vs the SEC

A crypto overreaction to a court decision

The EU is not banning self-custody

Project Guardian: blockchain payments meets global ambition

GDP vs GDI: are we looking at the right data?

Rates expectations: another readjustment ahead

An unnerving absence of tension

The spread of spot crypto ETFs

We will probably look back on 2024 as the Year of the Crypto ETFs. Sure, there will be other key industry milestones, such as new all-time highs, but the flurry of spot ETF listings is arguably an even bigger deal in terms of market impact.

With the US BTC spot ETFs now back to net inflows, attention turns to the possible listing of spot ETFs in Hong Kong.

In December, the Hong Kong Monetary Authority and its Securities and Futures Commission issued a joint statement saying they were willing to consider applications to list spot crypto ETFs, which in theory would be available to both institutional and retail investors. This week, Bloomberg reported that sources were suggesting the Hong Kong BTC spot ETFs could be “in kind” rather than the “cash only” preferred by the US regulator – this refers to the redemption mechanism, with “in kind” offering greater operational simplicity as well as more efficient tax and cost implications.

While this detail alone is not enough to ensure strong inflows, it does imply a more open and agile approach to the potential market, which in turn could attract a broader range of participants.

It also suggests that approval is getting close – this would be a very big deal.

Asian crypto exchange volumes are orders of magnitude greater than those from the US, according to data from The Block.

(a hastily put together pie chart using data from The Block)

Of course, volumes do not necessarily translate into fund inflows, and a significant chunk of Asian volumes are probably not “high quality” (the region is known for its wash trading). But the relative weight does suggest a greater familiarity with and interest in crypto assets, even if only as a vehicle for speculation. Put differently, the task of crypto education would most likely be a much lighter lift for potential Asian investors than it has been and will continue to be for the US market.

And the simplicity of as well as the implied official support for the ETFs could attract significant interest from Day 1.

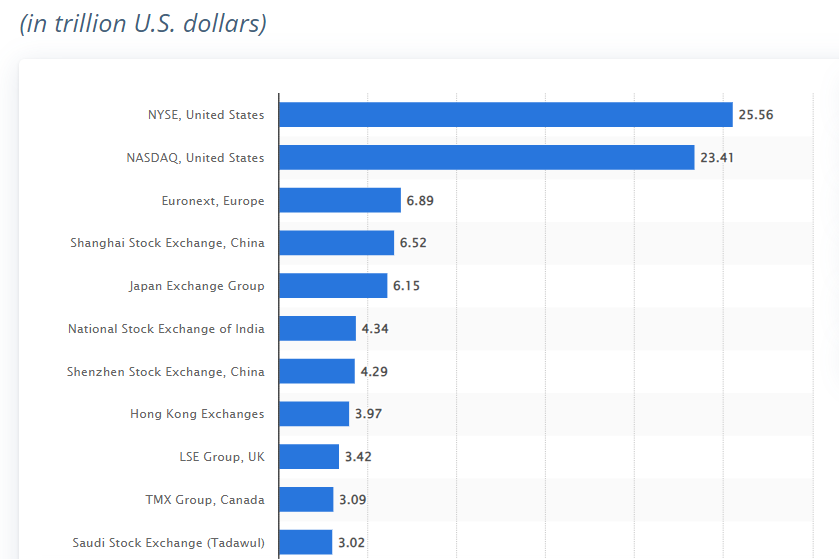

The initial inflows may be notably less than those for the US products, however. The Hong Kong stock market is tiny compared to those of the US, with almost $4 trillion in market cap as of December 2023, vs $25.5 trillion for the NYSE alone.

(global stock market capitalizations as at December 2023, via Statista)

What’s more, ETFs are a relatively new market in Asia, with average daily trading volume only 14% ($20 billion) of equity volume, vs 30% ($166 billion) in the US.

(chart via iShares)

And it remains to be seen what limitations (if any) the Hong Kong exchange ends up putting on BTC spot ETF purchases.

We have also yet to see a reaction from Chinese authorities. Mainland investors can access some ETFs on the Hong Kong exchange, but only those from an approved list. Offshore Chinese investors (of which there are many, and they tend to be large) have more flexibility, but might be reluctant to attract attention – just last month, Chinese state media reiterated its regular warning against cryptocurrency speculation.

However, as a trading venue, Hong Kong has already demonstrated its agility relative to that of the US: it allowed the trading of BTC futures ETFs only one year after they launched on the CME, and that of ETH futures ETFs one year before.

And demand seems to be growing. In February, Reuters reported that the AUM of Hong Kong’s largest BTC futures ETF had multiplied by 5x over the previous five months, to just over $100 million. (For scale, BlackRock’s IBIT BTC spot ETF now has AUM of more than $17 billion.)

Meanwhile, apparently searches from the mainland on WeChat for the term “bitcoin” were 12 times higher in February than the previous month; “bitcoin” was the 11th most-searched term on Weibo; and there are indications mainland investors are increasingly using their $50,000 annual forex allowance to accumulate crypto assets.

It’s not clear when these products will list in Hong Kong, but applications continue to trickle in and reports suggest approval will be granted sometime in Q2.

If so, this will coincide with the launch of crypto spot ETNs on the London Stock Exchange, although these will only be offered to institutional investors, which limits the likely impact.

And earlier this week, Bloomberg looked at recent moves to allow spot crypto ETFs to trade in Japan.

Whether this happens or not, we are potentially looking at continued strong inflows into global spot crypto products, at a time when the case for long-term positions as a hedge against currency debasement becomes even clearer.

Not only will this drive new demand for an asset with a provably fixed supply, but it will also usher in a new age of official acceptance of what just a few years ago was no more than an innovative thought experiment on paper.

To those working in the industry, it may seem like progress has been painfully slow. But the lens of history will tell us that it has actually been astonishingly fast.

“Crypto is no longer decentralized”: Yet another mainstream myth

The Financial Times has done it again. It has published yet another astonishingly inaccurate critique of crypto assets, written by one of its previous crypto asset reporters. I’m among the first to acknowledge there are many things crypto can (and should) be criticized for. What frustrates me is inaccurate critiques, especially from high-reputation media, since they only serve to perpetuate misconceptions that block off potential opportunity for both investors and entrepreneurs.

The essay, titled “What crypto (still) gets wrong”, posits that we have not yet learnt the lessons from 2022, and cites as evidence old cases of regulatory arbitrage, the harmful lack of constraints and the absence of a clear use case beyond speculation, as if they are all post-2022 twists to the crypto tale.

It’s not all about rehashing old topics, however. One recent development it covers is the return of “good vibes”, supposedly due to the launch of BTC spot ETFs. I share the author’s appreciation of a good case of irony and enjoy the nuance in the suggestion that the reason BTC is going up is because its “main benefits have been lost”. But that take focuses on a superficial snapshot that highlights a basic misunderstanding of blockchain technology, the crypto ecosystem, and digital asset structure.

Here's just one of the quotes I find particularly egregious:

“Technical explanations will almost always tell you that crypto’s key attribute is that it is decentralised. It is not.”

First, it lumps all blockchain-based assets into one “crypto” bucket. Not all crypto assets claim to be decentralized, and technical explanations do not almost always insist that they are. Not even close. True, some networks claim to be when they’re not – I don’t want to get into blockchain fights here, so I won’t mention names. And it’s fair to suggest that “decentralization” is an often misused term.

But the author is also misusing it, by implying it’s a binary condition: decentralized vs not decentralized. Many debate whether or not you can have partial decentralization – in my view, yes, as long as it is understood to not be pristine.

Second, a deeper mistake the author makes is to conflate blockchains with crypto market infrastructure.

For instance, the bitcoin network is decentralized. It has no leader, no foundation headquarters, no identifiable issuer, no transaction gatekeeper, no controllable upgrade approver.

Bitcoin market infrastructure, however, is not so decentralized. Nor does it need to be.

It’s about choice.

Those who want to emphasize seizure and censorship resistance, in other words those for whom decentralization is the key feature, can transact and custody in a decentralized, self-sovereign manner. Those who want to emphasize convenient capital appreciation can use centralized services, be they ETF wrappers, third party custody solutions, OTC desks, etc. With bitcoin, each holder can decide which tradeoffs are appropriate. With more traditional assets, this choice is not available.

The assumption that all bitcoin network participants want centralized services is just as wrong as the assumption that none of them do. And it misses the real innovation of the bitcoin network: it’s not the distributed influence and it’s not the speculative volatility. It’s the growth of an unusually free market that will continue to reflect the balance between aggregate global demand and a provably fixed supply.

Similar tradeoffs are available in other networks with different characteristics, presenting market participants the age-old choice between varying degrees of security and convenience.

Essentially, this is another reflection of how free markets work: services and products tend to emerge to satisfy unmet demand. If users of a decentralized market want centralized convenience, they will get it. But that doesn’t mean the blockchain is centralized. And even if all centralized crypto service providers were to shut down tomorrow, crypto markets would continue to exist.

The author of the piece is a good writer, and won an award for his coverage of the FTX implosion. This deserves congratulations, but it does seem to be colouring his crypto lens as his article implies that the whole industry is tainted with the brush of fraud and hubris.

What’s more, neither are purely crypto problems. I would have hoped that the author’s FTX coverage would have taught him the value of decentralized transparency and the pressing need for better investor education. In the end, it wasn’t the search for financial independence and transaction integrity that caused so much pain – it was greed and gullibility. The Financial Times has done some excellent work over the years in covering scams, corporate implosions and the limiting constriction of blinkered regulation. It is sad to see it join the very elite it is supposed to hold to account by spreading inaccurate assumptions about the true opportunity in decentralized networks.

Then again, now that Sam Bankman-Fried has been sentenced, maybe mainstream media can finally move on?

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade.

HAVE A GREAT WEEKEND!

Given the reflective connotations of this weekend, I want to share an uplifting rendition of the Halo theme, sung in a chapel by the Munx Gregoriana choir. Peaceful with a touch of foreboding.