WEEKLY, Nov 26, 2022

Hello everyone! I hope you have a good weekend planned, and that those of you in the US managed to dodge the family grilling at the Thanksgiving table about the collapse of this crypto thing. I had fun yesterday trying to explain to friends that, no, fraud was not exposed in bitcoin. You’re reading the free weekly Crypto is Macro Now – if you’d like daily insight into market trends and news that highlights the intersection of crypto and macro, I hope you’ll consider upgrading to the premium version.

Nothing I say is investment advice. If you find this newsletter useful, by all means share with friends and colleagues.

MARKETS

BTC and ETH held steady over the Thanksgiving holiday on low volumes, after a week of surprising resilience given the bad news buffeting the crypto ecosystem. In spite of some intra-week fluctuations, the BTC/ETH ratio ended up more or less flat on the week, while a decline in bitcoin’s dominance hinted that some of the smaller crypto assets were starting to recover from the market’s recent shock.

(chart via TradingView)

One of these is Litecoin (LTC), which is at time of writing is up over 22% vs a week ago and over 42% on the month. The narrative seems to be focused on its upcoming halving (where mining rewards are slashed by 50%), expected in approximately eight months. This could start to direct attention to bitcoin’s upcoming halving, which is not expected until May 2024. In the past, BTC rallies have kicked off 12-18 months prior.

(chart via Coin Metrics)

The FOMC minutes released on Wednesday confirmed the emerging consensus that a slow-down in the pace of rate hikes was imminent, and futures markets are currently pointing to a 50bp increase in December (75% probability) and February (52% probability). Excitement about a slowdown does seem to have tempered slightly, however, and expectations of a 25bp hike in February have dropped over the past week from 40% to 34%.

(chart via CME FedWatch)

In the premium daily emails, I look more closely at market moves as well as at:

BTC volatility trends

Institutional investor intentions

ETH performance vs BTC

Fund flows

Macro relief in the US and Europe

DXY outlook

… and much more. If any of this interests you, I hope you’ll consider upgrading ($8/month).

COLUMN

Central Banks and Bitcoin: Closer Than You Think

Amidst the turmoil of the last few weeks, it’s easy to lose sight of what our industry is about: independence and innovation. These two fundamental drivers of prosperity and progress are not unique to crypto – but only in crypto are they entwined and embodied in liquid assets.

One feature of the innovation is the vast range of assets that exist and continue to emerge. Not all will survive, but those that do will have the potential to impact the entire spectrum of economic influence, from individual savers to professional investors, from merchants to financial institutions, from local communities to central banks.

Central banks? Yes. While we do not yet have clear examples of central banks embracing crypto, it’s not far off. And the US dollar only has itself to blame.

It’s tragically ironic that after a period of the sharpest increase of US money supply in history, nations around the world are suffering an acute shortage of dollars. A couple of days ago, Ghana moved to start paying for oil imports in gold due to a lack of greenbacks. Earlier this month, credit ratings agency Fitch downgraded Nigeria due largely to the central bank’s policy of rationing the supply of US dollars, which has led to fuel scarcity, suspended flights and accelerating inflation. Last month, reports emerged from Egypt of a chronic wheat shortage due to a lack of dollars with which to pay for large shipments of the grain sitting on ships in Egyptian ports. This summer, Sri Lanka found itself unable to pay for fuel, had to close schools and offices, and prioritized allocations to counterparties who could pay in dollars. Earlier this year, dollar rationing by Kenyan banks led to food shortages and soaring prices. The list goes on – dollar shortage stress around the globe is triggering hunger, accelerating price spirals and, in some cases, toppling governments.

A large part of this is political. The US Federal Reserve has a system of swap lines that dispense dollars to foreign central banks in case of need. But not to all central banks – only Canada, England, Japan, the EU and Switzerland have access to standing swap lines. In theory, others can get temporary ones in times of crisis, but even during the height of the pandemic, the Fed only provided swap lines to two emerging economies: Brazil and Mexico.

The worsening credit profiles of would-be dollar borrowers are a factor in this lack of generosity, as is the concern that US loans might go to repay Chinese debt or finance imports from Russia. And while the US can come to the rescue when total implosion is imminent, as it did for Sri Lanka earlier this year, that intervention can carry conditions that many nations are unable to meet – greater distance from China, for instance.

Even holding liquid dollar assets as reserves is not what it used to be. The seizure of Russian reserves at the start of the war in Ukraine has shown central banks that the world’s “safe asset” is not as safe as everyone thought (and as for price volatility, well…)

Now, what if there were a seizure-resistant monetary asset that was not subject to the economic priorities of third parties that could be sold for dollars 24/7/365? Oh wait, there is.

Attention to the idea of central banks holding bitcoin is growing. In May, the Alliance for Financial Inclusion organized a conference in El Salvador that convened central bankers and financial regulators from 44 countries to discuss small business financing, financial inclusion and bitcoin. Most were from small countries, but not all: representatives from Nigeria, Bangladesh, Pakistan and Egypt – each in the top 50 countries ranked by GDP – were present, and beyond Africa and Asia, coverage included nations from the Middle East, Latin America and at least one former Soviet republic.

Even academia is getting involved. Last week, Matthew Ferranti of Harvard University’s economics department published a paper on, you guessed it, central banks and bitcoin. Technically the paper is about the risk of sanctions on central bank reserves and is one the first to focus on the impact of sanctions before they happen, via hedging and the resulting effect on the reserves composition. Ferranti concludes that the shifting global landscape makes a case for the inclusion of cryptocurrency in that mix, and produces a whole lot of formulas and numbers to back that up. The renminbi gets a shout-out, too.

Central banks do seem to be re-evaluating their allocations. A recent report by the World Gold Council revealed that Q3 gold purchases had jumped 18% year-on-year, with central banks accounting for a quarterly record of 400 tonnes (the previous record was 241 tonnes in Q3 2018). Central bank purchases for the year to date reached 673 tonnes at the end of September, higher than any other full year total since 1967.

But it is no secret that even gold reserves are vulnerable. The New York Federal Reserve building on Wall Street holds the world’s largest known monetary gold reserve, much of which belongs to foreign central banks. Access to gold reserves, whether physical or paper, is not 100% guaranteed. Bitcoin, on the other hand, is a bearer asset that is not expensive or complicated to store securely on national territory, a few clicks away from a market.

It’s even possible the embrace of bitcoin by emerging economy central banks could be with US support. The alternative is US lending to high-risk countries, which carries a domestic political cost; the expansion of non-dollar swap agreements, such as with China; or the collapse of some emerging and frontier economies. Apart from the human tragedy, many are key commodity exporters.

I used to think the adoption of bitcoin by central banks for their reserves would happen soon, given the urgent need in some pockets of the global economy – now I realize that getting regulators comfortable with the idea, especially after the high level of misunderstanding of what the FTX collapse is actually about (ie fraud not crypto), could take some time. But it is becoming increasingly clear to me that it will happen, because it needs to. The doubt and distrust sown by recent crypto drama will recede, and the desperate need to shore up economic resilience – combined with a growing understanding of the relative simplicity of an asset that can be converted into dollars or any other currency at any time – will incentivize greater acceptance and experimentation.

We are also likely to see a domino effect: where one goes, so will others. And with this, the world will witness an asset that started retail-first, from the ground up, ending up as a support for not just central banks but also the resilience of entire nations.

KEEP AN EYE ON

(A couple of the main themes from the week, explored in more detail in the daily emails.)

The drama that keeps on surprising

As more details emerge about the bad management, financial carelessness and willful deception in the sprawling FTX network, one encouraging note emerged this week. Binance CEO CZ has announced plans for a $2 billion recovery fund for companies hit by the fallout, with other participants such as Jump Crypto, Polygon Ventures, GSR, Aptos Labs, Animoca Brands and Kronos saying they will participate – apparently over 150 applications have been received. On the surface, this seems like good news, but there is still little clarity on how this fund would be managed. An empire grab on the part of Binance, already the industry’s largest exchange in terms of volume, would be concerning given the harsh consolidation. It would also be helpful to know more about how the recipients would be selected, and under what conditions.

Securities innovation

Last week, the Australian Stock Exchange officially ditched its blockchain project which had suffered from chaotic management, considerable delays and painful budget overruns, giving critics cause for told-you-blockchain-was-not-a good-technology glee. This is shortsighted. That particular project may not have worked (although the issue was not so much the technology as the overreaching scope and the myriad interests involved), but we are seeing meaningful experimentation with the concept of blockchain-based “traditional” securities elsewhere, in what looks like a much healthier approach: test small and iterate from there.

Singapore-based bank DBS completed its first intraday repo trade on JPMorgan’s Onyx blockchain network. Intraday repos are not practical under the traditional system since settlement usually takes two days – Onyx’s instant settlement potentially opens up new types of capital utility.

Fund managers Apollo and Hamilton Lane will be launching digitized funds that will trade on Figure’s blockchain-based marketplace for investors, which already has several other vehicles listed, in a move that should further test demand for lower cost and faster settlement of fund units.

The Dubai Multi Commodities Centre (DMCC), a commodities exchange that is also the UAE’s largest free-trade zone and is owned by the government’s principal investment arm, has partnered with Sharia-compliant gold-backed token issuer ComTech for blockchain-based gold trading.

The government of El Salvador is considering a bill to establish a National Digital Assets Commission which would regulate entities involved in the issuance of digital securities and would set the stage for the issuance of the long-awaited bitcoin-backed “volcano bonds”.

What institutions are up to

A survey sponsored by Coinbase and carried out by Institutional Investor Research canvased 140 institutional investors (not sourced from Coinbase clients) in September-October and found that:

Of those already invested in crypto, 62% have increased their allocations in the past 12 months.

58% of those already invested expect to increase their allocations over the next three years.

54% of those surveyed expect crypto asset prices to remain “flat and range-bound” over the next 12 months.

71% believe they will increase over the long term.

Fund inflows

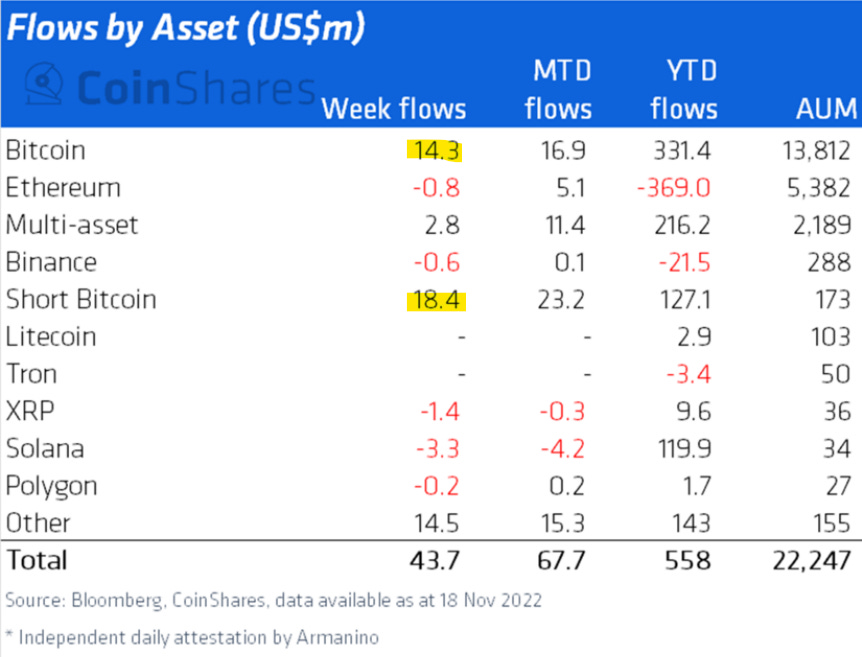

The CoinShares report published this week disclosed some interesting data points that depict a bad market but with some investors coming back in.

Of the new inflows into listed crypto vehicles over the past week, 75% went into short products.

AUM on short-bitcoin products is now $173 million, close to the all-time-high of $186 million.

Short-ether products saw a record weekly inflow of $14 million.

Overall AUM of listed crypto products is down to $22 billion, its lowest in two years.

Inflows into BTC long products reached $14.3 million, slightly down from last week’s $18.8 million but well above the average for the previous few weeks.

Solana continues to see outflows.

Switzerland accounted for almost 55% of total inflows, followed by the US and Germany with approximately 20% each.

(table via CoinShares)

A YEAR AGO

(This section looks back at what was going on this time last year, so we can see how far we’ve come and how far we haven’t.)

This time last year, NFTs still dominated the headlines with eye-watering sales (a gold fur Bored Ape sold for $2.8 million) and luxury brand name-dropping (Givenchy dropped 15 NFTs on OpenSea). Damien Hirst converted a Drake album cover into an NFT, Macy’s launched a parade-inspired NFT collection for charity, and Collins Dictionary decided that “NFT” was the 2021 Word of the Year.

Metaverse land sales were heating up, with a Canadian investment company buying $2.5 million worth of Decentraland real estate, and one Axie Infinity plot selling for the same amount.

And El Salvador was laying plans for a $1 billion bitcoin bond issue, partnering with crypto firms Blockstream and iFinex (see above – a year later, we may finally be getting there?).

GOOD READS/LISTENS

Niall Ferguson offers a sweeping review of the state of the crypto market landscape, with some history, philosophy and sociology thrown in

An unironically hilarious poke at how ridiculous our industry can seem to outsiders by Joe Weisenthal – we gotta be able to laugh at ourselves.

A report by Mikey Ox at 1k(x) gives a good overview of DeFi yields, with easy-to-understand breakdowns, categorizations and examples

An interesting analysis of alternative BTC vehicles by Charlie Morris at ByteTree that compares GBTC, MicroStrategy and the BITO bitcoin futures ETF, with some surprising findings.

Bloomberg’s Trillions podcast looks at the evolution and outlook for crypto ETFs in the wake of the FTX fallout.

Have a good weekend!

This section is not about pretty dresses, so, guys, stick with me.

We all have to wear clothes. What we wear is rarely as important as why we’re wearing it, but that latter part hardly ever gets spoken about. Instead we focus on the choice of shirt color, the length of the sweater, two buttons or four. We almost consciously try to ignore the why – blending in, standing out, signaling wealth, signaling grit…

I’m not at all into fashion (here’s where you say “Noelle, we never would have guessed!”), and I hate clothes shopping. But I like to look nice – however, that is always subjective, right? So, who do I want to look nice for? I actually don’t know. This realization started me down the rabbit hole of why some groups find a certain look nice, while others favor a different vibe.

I’ve also been thinking about signaling, how most of what we do in public sends out a signal to others, whether we realize it or not. The car we drive, the way we walk, the bags we carry, and, of course, the clothes we wear. Even trying to not signal is a signal in itself.

Last weekend, trying to escape the toxicity on Twitter and get crypto contagion out of my brain loop, I binge-listened to Avery Trufelman’s Articles of Interest podcast series. It’s a beautifully produced deep dive into specific articles or segments of clothing that most of us encounter every day, looking at the history, symbolism and current status of jeans, plaid, pockets, hawaiian shirts, button-downs and much more. There are three seasons, from 2018, 2020 (both still totally relevant) and the current one about the American Ivy League look. Thoughtful, eloquent, fun and eye-opening, if you ever want to clear your head with a reminder that the world is also fascinating outside of crypto, I recommend them all.

(image via the American Ivy newsletter)