WEEKLY, Oct 15, 2022

Hello everyone! You’re reading the weekly Crypto is Macro Now newsletter, where I look at the crypto market and its growing overlap with the macro landscape. Since many of you are new here (welcome!), I’ll introduce myself again: I’m Noelle, and I’ve been writing crypto-focused newsletters for over six years now, first for CoinDesk and more recently for Genesis Trading. Now that I’m concentrating on independent research (the theme is in the title), it felt natural to continue. If you find this useful, please consider sharing with friends and colleagues.

And if you’d like to receive a premium daily email with more detailed market and news commentary and are not already a subscriber, hit the signup button below. Programming note: The daily emails for Monday and Tuesday will be short and possibly late as I’m at Blockworks’ Digital Asset Summit (DAS) in London and have yet to figure out how I’ll juggle panels with finding a plug for my battery-challenged laptop. To compensate, I’ll do my best to ferret out some interesting takes to share. (And if any of you will be there, I’d love to say hi!)😊

Crypto, Stocks and Bonds: Comparing Relative Risks

It feels strange to be thinking of signs of spring just as the northern hemisphere heads into autumn – but after the long market winter we have all already been through, shoots of green are eagerly anticipated.

This does not mean that they are expected – there is too much uncertainty and volatility in all markets for rally forecasts to take deep root just yet. However, after the steep drawdowns we have seen in stocks, bonds and bitcoin, it is worth asking how much further market values have to fall.

While the answer to that question eludes even the most experienced observers, the exercise invariably involves an analysis of downside risk. This may seem futile in an environment with so much risk everywhere, but it does unearth some fundamental insights that can inform allocation decisions as the eventual floors get ever closer, especially when comparing relative vulnerabilities.

With that in mind, let’s take a look at the different risks faced by stocks, bonds and bitcoin, with the acknowledgement that stocks and bonds are by no means uniform within their grouping and that bitcoin does not represent the whole crypto market.

Stocks

Drawdown from peak: 27.5%

Date of latest peak: Jan 3, 2022 (S&P 500, per TradingView)

Earnings risk: when it comes to stocks, investors tend to think in P/E multiples – as investor Howard Marks put it: “it’s not what you buy, it’s what you pay”. The earnings in the equation are always forward earnings which are tricky to predict, even for “boring” utilities. Costs, demand, even pricing are all variable and usually unknowable, and in environments of slow economic growth combined with persistent inflation, even more so.

Earnings miss risk: Even if a company were to have healthy earnings, there is a chance that it comes in below consensus estimates. This could trigger a price drop even if the company did everything right other than manage market expectations.

Interest rate risk: Higher interest rates impact a company’s share price on four fronts:

1) demand for investment opportunities is diminished due to the higher cost of financing those investments;

2) the net present value of future cash flows is lower when discounted at higher rates – this is especially true for growth companies with the bulk of earnings expected further down the timeline;

3) higher interest rate costs which hit the amount of earnings that can be distributed to shareholders;

4) a more difficult credit environment could make it harder for a company to finance growth (= reduced earnings) or even service its existing debt – but this last impact deserves its own section.

Bankruptcy risk: Shareholders can lose most or even all their investment if a company declares bankruptcy due to inability to service debt. This can happen through mismanagement or through an unforeseen external event (such as a pandemic or war).

Dilution risk: A company can decide to issue more shares to raise funds, even in weak markets when debt financing is harder to come by. This reduces the amount of earnings to be distributed to each share and should therefore lead to a downward repricing.

Technology risk: No matter how great a company’s technology, something can come along to replace it. Just ask IBM.

Competition risk: New products and/or marketing strategies can also cause a company to lose earnings, especially in markets where preferences change fast. Just ask Netflix.

Regulatory risk: Governments can change the operating rules of an industry (e.g., earnings caps), break up large companies, penalize some technology use over others (e.g., carbon pricing), or mandate lower capital efficiency (e.g., banks).

Narrative risk: Investing “themes” can come into and go out of fashion fast. After all, going short fossil fuel producers seemed like a good idea only a year ago.

Personality risk: Companies are run by people, and people sometimes do weird things which can impact how the market feels about a stock.

Currency risk: For investors holding foreign stocks, expansive monetary policies and/or economic difficulties in other countries can debase currencies and therefore relative value.

Bonds

Drawdown from ATH: 22.1%

Date of ATH: August 4, 2021 (US Aggregate Bond ETF, per TradingView)

Interest rate risk: Most of the potential impacts of rate hikes on stocks also apply to bonds, with the addition of the role of rates as one of the few variable inputs into valuations. Also, the likelihood of official rate hikes pushes up bond yields (market rates need to keep up with expectations of official rates) which pushes down bond prices.

Economic risk: This affects corporate and sovereign bonds through weaker fundamentals that impact the likelihood of repayment. The lower the likelihood of repayment, the higher the rate demanded by investors to compensate that risk, and the lower the bond price. It also impacts longer term bonds through the “term premium” which expresses a view of economic health and therefore likely interest rates further out in time.

Corporate risk: Even beyond economic risk, corporations can mess up and weaken their business fundamentals. Come to think of it, so can governments.

Ratings risk: This is related to corporate and economic risk in that issuers made weaker through an adverse business climate usually get their bond rating downgraded, but ratings agencies are usually late to the party. A downgrade can impact the price of a bond by pushing it out of the range of investors who either prefer or are limited to investment-grade instruments (BBB- and above).

Currency risk: Investors holding bonds denominated in a foreign currency run the additional risk of sentiment-driven currency moves, monetary policy currency debasement, and official devaluations driven by local economic priorities.

Bitcoin

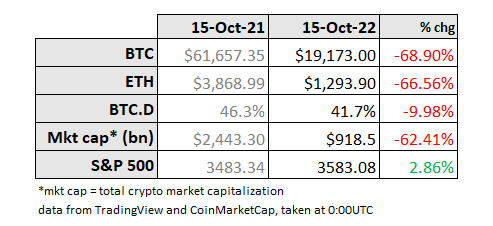

Drawdown from ATH: 73.6%

Date of ATH: November 10, 2021 (per TradingView)

Interest rate risk: As with stocks and bonds, a tightening monetary environment hurts almost all assets, bitcoin included, through the reduced access to funding for investments. Plus, any investor attempting to discount an estimated future value of BTC will get a lower value at higher expected rates.

Narrative risk: It’s possible that all of the narratives underpinning the bitcoin investment thesis – seizure-resistant store of value, innovative data storage technology, censorship-resistant payment rail, etc. – fall out of fashion simultaneously.

Regulatory risk: While no significant regulator is talking about banning the trading and production of bitcoin, certain jurisdictions could implement policies that impact investor interest in the asset, such as taxation or oppressive information gathering.

Technology risk: While the Bitcoin blockchain has withstood over a decade of attempted attacks, the advent of new technologies such as quantum computing, which could brute force the decoding of wallet key encryption, could require updates to the protocol. Any protocol update, no matter how tested and no matter how supported by consensus, does carry some risk.

CONCLUSION

Looking at the above, we can see that stocks have the broadest range of potential downside risks, and yet they do not generally command a higher return in compensation. In good markets, that role usually goes to crypto assets. In bad markets, bonds tend to suffer less.

(chart via TradingView)

So, why has BTC been especially punished so far this year in terms of price performance? Unlike stocks, bitcoin has no earnings risk (because it has no earnings), no bankruptcy risk (because it has no debt), no dilution or debasement risk (because it has a verifiable and programmatic hard cap), and no personality risk (because it has no leader). What’s more, unlike with stocks and bonds, its exposure to interest rate risk is limited to lower market liquidity and discounted future value.

One answer could be that the level of familiarity is still relatively low. This is changing. Another could be that BTC’s high volatility rewards on the upside but hurts more on the downside. But, given the relative risks of the main asset groups, this could be due for a realignment.

Even more relevant for the short-term, do the relative drawdowns adequately reflect the risk profiles of the asset groups? A year from now, which is more likely to have the highest appreciation, even if the interest rate outlook remains uncertain?

When bitcoin was a niche asset removed from macro investment considerations, its merits and pricing could justifiably be considered in isolation from traditional assets. Now that it forms part of the general investing landscape, its potential and its risks deserve to be looked at in context.

KEEP AN EYE ON…

(Three main themes from the week.)

Really weird markets. The hotter-than-expected inflation print on Thursday, which highlighted the stickiness of core inflation and the Fed’s tough battle ahead in getting it down, triggered an astonishing seesaw of asset values as investors veered from dismay over the likely stronger hikes to chasing what could have been a short squeeze. The S&P 500 swung an astonishing 5.6% between the low and the high, one of the wildest moves on record, while BTC’s range was a less surprising 8.7%.

A more sober tone set in on Friday, with BTC, ETH and stocks unwinding the previous day’s surprising gains, each ending the week slightly lower. The yield on 10-year US government bonds ended the week over 4.0%, delivering the 11th consecutive weekly jump, the longest stretch in 38 years. Treasury market volatility as measured by the MOVE index continued to climb this week, yet again reaching its highest point since July 2009. Even Janet Yellen seems to have read something that startled her, because she went from assuring us on Tuesday that everything was fine, to warning us on Wednesday that there were worrying signs brewing.

Again, but with a British accent. The week served as a humble reminder that government bonds are not necessarily “safe”, a lesson no-one will forget any time soon. How this ends up changing portfolio construction is still up in the air, but the myth that the 60/40 equities vs bonds balance will protect wealth is now definitively dead. It is also a reminder of how political markets are. The UK has now had four Chancellors of the Exchequer in as many months, and if Liz Truss is ousted next week as some are predicting, that could be a short-lived record.

Another lesson learnt that officials and regulators around the world are no doubt taking note of: politicians cannot ignore loud markets. Next week will be key for restoring trust to the markets, although “calm” might be a stretch as the Bank of England ended its intervention yesterday, expectations are climbing for the strong hike at the next policy meeting on November 3, and there is still much confusion over what the new government’s fiscal policy will be.

Bitcoin mining adjusts. This past week saw a host of significant shifts in the outlook for bitcoin miners.

The mining difficulty reached an all-time high in response to the increase in hash rate, making it even more expensive in terms of computing power and energy consumption to successfully add a transaction block to the chain.

While this negatively impacts the profitability of miners, new solutions continued to emerge to help them weather market conditions. Binance launched a $500 million fund to provide loans to Bitcoin miners, while crypto services firm Luxor unveiled a bespoke derivatives service to help miners hedge risk.

The industry is still going through an unprecedented time of low revenue and margins, however. According to data from Coin Metrics, Bitcoin miner revenue per hash hit an all-time low earlier this week.

(chart via Coin Metrics)

This is likely to lead to some closures and some consolidation. This week we heard that Crusoe Mining had acquired Great American Mining, also active in the flared gas utilization segment.

And although funding is generally dry for miners at the moment, some mining companies are still able to raise. For example, TeraWulf this week announced that it had secured $17 million in a mix of equity (sold to existing shareholders) and debt (from an already existing loan facility).

Some of the additional topics covered in the daily emails:

BTC volatility

BNY Mellon and crypto custody

Crypto and the younger generation

Too many hacks

Hints at a rate hike pause

Crypto adoption growth in Brasil

If you are not yet a subscriber and would like to be, you know what to do:

A YEAR AGO

(This section looks back at what was going on this time last year, so we can see how far we’ve come and how far we haven’t.)

By mid-October last year, the NFT craze was in full swing. In the week of Oct 8-15, 2021, FTX launched an NFT trading platform. Coinbase announced plans to follow suit, reportedly accumulating a waitlist of 900,000 on day one. Not ones to miss out on trends, Visa and Sothebys also launched NFT platforms. And talent managers started getting in on the act, with Bored Ape Yacht Club founders signing with Maverick (also handler of Doja Cat, The Weeknd, Britney Spears and Madonna), and Hollywood talent agency CAA (handler of Beyonce, Shakira and Jennifer Aniston) signed NFT collector 0xb1 to help monetize their collection.

Bitcoin ETF hype was also starting to gather force, with Ark Invest and 21Shares teaming up to file an application, and the SEC approving three crypto equity ETFs for trading (two from Invesco and one from Volt).

And data from the Cambridge Centre for Alternative Finance showed that the US had edged into the global Bitcoin hash rate lead with 35%.

GOOD READS/LISTENS

Robert Burgess dives into a topic that is top of my “we should be paying more attention to this” list: the dwindling liquidity in the US Treasury market.

What Goes Up podcast: Flash Boys in the Crypto Cloud - Michael Safai of Dexterity Capital talks to Vildana Hajric and Mike Regan about the institutionalization of crypto markets, how they still differ from traditional markets, and what traders look for.

Unchained podcast: Kristen Smith of the Blockchain Association talks to Laura Shin about crypto regulation. There have been so many reviews of the current regulatory status recently, but this one is a particularly good one.

Bankless podcast: What Happens Next in Crypto? Fiskantes and Mattis deliver a constructive and sober outlook on crypto narratives, what the ecosystem is missing, and where the “next big thing” might emerge. An interesting listen.

Have a Great Weekend

By now you’ve probably heard the protest song climbing the global charts and on track to win a Grammy even though it has been banned in its native country Iran and its creator arrested. If you haven’t, it’s moving. Shervin Hajipour uploaded the song to Instagram, and within 48 hours it had received 40 million views. The authorities made him take it down, but by then it had been uploaded to YouTube, Spotify and other platforms. Based on a curated list of protest tweets, it is being chanted in demonstrations, blared from car windows, scribbled on school blackboards, and has justifiably attracted the attention of international media. The raw yearning for aspects of daily life that many of us take for granted – I confess it made me weep, and stands as a powerful reminder of the unifying emotion of an anthem.

Disclosure: I hold some BTC and ETH, and I don’t trade. Nothing I say is investment advice!