WEEKLY, Oct 21, 2023

manipulation misunderstandings, Zimbabwe digital gold, music links

Hi everyone! I hope you’re holding up ok – crazy times.

You’re reading the free weekly edition of Crypto is Macro Now, where I update and/or re-share a couple of things I wrote in more detail about during the week. If you’re a premium subscriber, you’ve probably already read them (although today’s are updated with some new parts), so feel free to scroll all the way down for some cool non-crypto links.

If you’re not a premium subscriber, I hope you’ll consider becoming one! You’ll get a daily update as to the crypto and macro trends that I feel are being overlooked, along with some market commentary. It’s only $8/month for now, and it would allow me to continue to explore the impact the crypto ecosystem will have on the global economy – I really feel this intersection matters, now more than ever.

Follow me on X at @noelleinmadrid where I share photos of gorgeous city I live in, charts, comments on headlines, and, you know, stuff depending on the mood. Also, if you love short daily podcasts, I’m now host of the CoinDesk Market Daily, where I give a brief rundown of crypto and macro markets.

Of course, nothing I say is investment advice!

Feel free to share this with friends and family, and if you like this newsletter, do please hit the ❤ button at the bottom.

Some of the topics discussed this week:

Crypto and terrorism

A spot BTC ETF is not priced in

Mixed signals for BTC

Is BTC finally reacting?

Is any crypto regulation better than no crypto regulation?

Who do tokenized securities really benefit?

Tokenization disappoints again (for now)

Beware that yield curve steepening

Equities are stretched, and it’s Big Tech’s fault

Manipulation misunderstandings

Monday’s drama in the bitcoin market was not just about a misreporting of what would have been a key development in crypto markets. It was also about media business models, and a misunderstanding of SEC objectives.

Media business models.

CoinTelegraph’s explanation of what happened pointed to a couple of employees who, according to the company, did not follow the usual process when sharing information on social media. Processes are there for a reason, but the real driver here was the need for clicks which are often driven by being the first to break news. The haste to be first is a symptom of the current sad state of media business models, where advertising revenue keeps the lights on. Advertising revenue is directly related to traffic, so speed can trump accuracy. There are signs that we are evolving away from this damaging clash of incentives, such as the popularity of independent newsletters, and the potential for more distributed micro-payment systems.

Misunderstanding of SEC objectives.

Some on X (formerly known as Twitter) were claiming that this error reduced the chances of a spot bitcoin ETF this year. This implies that the misinformation was not a mistake – it was the result of manipulation. There could be some truth to this as, according to CoinTelegraph, the Telegram account from which it got the information has since been deleted. But this is not the type of crypto manipulation that the SEC is worried about. The agency’s insistence on rigorous market surveillance agreements suggests that it is more concerned with actual price manipulation on trading venues. Social media manipulation is very different.

That’s not to say the SEC doesn’t care about social media manipulation. It does, and in 2018 it even brought an action against the now-owner of X for precisely that, accusing him of fraudulently tweeting that funding had been secured to take Tesla private. It has taken other actions against individuals that were quite blatant in their moves.

But the SEC is unlikely to go after anyone in this case. There is a culprit, but their identity is not clear. It could also be hard to prove that it was a deliberate act. It was not a continued campaign, and while money was won and lost, the total amount is not going to be worth the SEC opening an investigation.

So, the possibility that this changes the SEC’s plans to approve a spot BTC ETF is remote. It would need to prove that this sort of thing never happens in other assets on which ETFs are based which, of course, it can’t do.

Zimbabwe, tokens and economic orthodoxy

Can gold-backed digital tokens reduce a country’s dependence on the US dollar? Zimbabwe hopes so. Earlier this month, its central bank announced that the blockchain-based gold-pegged tokens known as ZiGs will become an official means of payment for domestic transactions.

Why it matters:

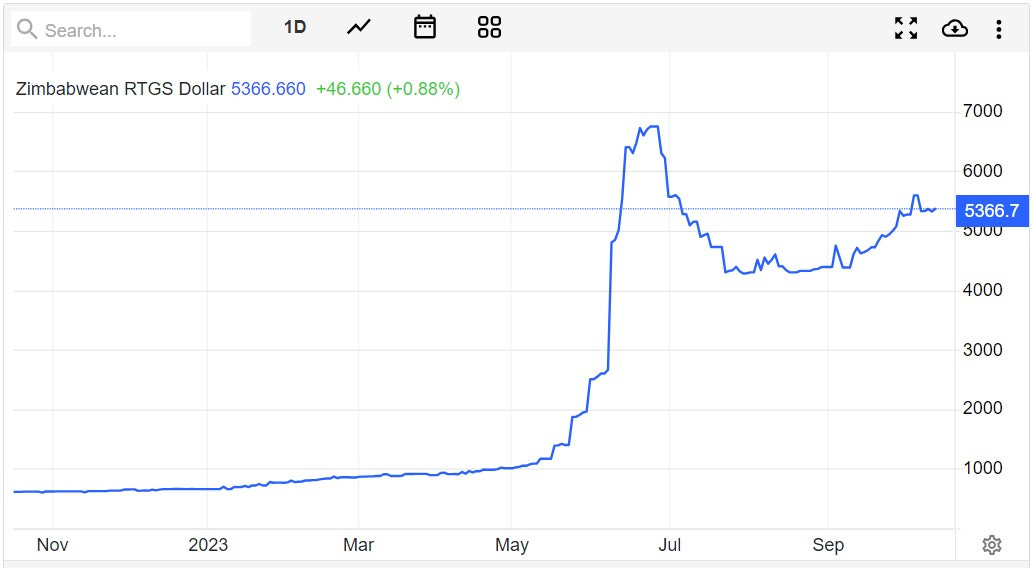

First, some background: back in May, the Reserve Bank of Zimbabwe (RBZ) announced the issuance of gold-backed tokens, to reduce demand for the US dollar. At the time, around 80% of the country’s economy was dollarized, and the government was about to kick off a serious flurry of money printing in preparation for the August election. In May alone, the Zimbabwe dollar lost more than 80% of its value against the US dollar. It has since recovered some, but year-to-date, the depreciation clocks in at almost 90%.

(chart via Trading Economics)

Interest has been barely tepid, however. The first round of issuance attracted 135 bids for a total of just over $12 million, mostly in Zimbabwe dollars rather than the hoped-for US dollar. Since then, demand has weakened further: in the mid-June issuance, there were only 35 new applications. In September, the number dwindled to 16. This covers a total of 350kg-worth of tokens. Back in April, central bank representatives was talking about probably needing 55,000kg for the issuance.

Now, the central bank is renaming the tokens “ZiGs”, and has made them an authorized payment token for domestic transactions. The objective is still to stem the rising demand for US dollars, which are hard to come by.

This could boost interest. After all, here we have a digital token designed as a store of value morphing into a payment token. Greater utility leads to greater demand, right?

Not necessarily. There are still significant barriers:

1) The main one is still lack of trust in the central bank. This is the same institution that has overseen the repeated devaluation of the Zimbabwe dollar as well as the forced conversion of foreign currency holdings at unfavourable rates.

The new system is not exactly designed to improve the low level of trust. There’s no indication that I’ve found (and I’ve looked) as to what blockchain is being used, and how users can verify that they and only they have control over the tokens. It doesn’t sound like they’re seizure-resistant. At least US dollars can be hidden under the floorboards.

2) There’s also no way that I’m aware of for users to verify the backing exists. Maybe that doesn’t matter, maybe it’s the peg that is the important part for value stability. But it does suggest that the issuer could alter the terms and valuation when it deemed necessary.

3) Getting the gold will probably not be a significant barrier, unless demand does take off. Earlier this year, Bloomberg reported that Zimbabwe had around 350kg of gold in reserve, which is roughly the amount needed to back the token sales so far. Zimbabwe is a gold producer, with 2022 production of 35,000 kilograms up 20% on the previous year. But the country relies on gold exports to obtain its much-needed foreign currency. The more it holds back for tokens that are being bought mainly with Zimbabwean dollars, the greater its US dollar deficit.

4) And there’s the expectation that merchants and businesses around the country are going to be able to manage setting up digital wallets. Most of the hassle will be handled by participating banks, but users will still need to get used to a new payments flow.

However, there are a couple of features of the move that I find interesting.

One is that it is a type of CBDC, only on a gold standard. There’s a reason that virtually no gold standard has ever worked, but as far as I know, one hasn’t been tried for an alternative (as opposed to the main) currency. It’s unlikely that Zimbabwe will be the first to make this experiment work given its tenuous economic and political situation. But, it will be interesting to watch.

Another is that the IMF is not happy about this. It has urged Zimbabwe to use “more conventional” methods to deal with its currency crisis, such as tightening monetary policy and liberalizing its foreign exchange market. That would be welcomed by many, but does not seem politically viable and could carry a far greater social cost than the IMF seems to appreciate. A profound change in the nation’s current path is obviously necessary, and it’s unlikely the gold-backed tokens will fix much. The situation is a clear example of how economic orthodoxy is breaking down, and that desperate governments are turning to new ideas while they struggle to hold on to power.

We’ll see more examples of this in coming months, no doubt.

HAVE A GOOD WEEKEND!

Continuing with the theme of Spanish music you might not know, here are three more of my favourites – good weekend mood songs:

Ella Baila Sola – Cuando los Sapos Bailen Flamenco

Bebe – Siempre Me Quedará

Vetusta Morla – 23 de Junio