WEEKLY, Oct 8, 2022

Hi everyone! Welcome to the second weekly Crypto is Macro Now. Thank you to all of you who have subscribed over the past week, I am so pleased you’re here. A brief introduction: I’m Noelle, and I’ve been writing crypto-focused newsletters for six years now, first for CoinDesk and more recently for Genesis Trading. Now that I’m branching out into independent research (the topic is in the title), it feels natural to continue.

In addition to this weekly review, I write a premium daily email that talks about themes relevant to both macro and crypto, and what the changes that we’re seeing tell us about what’s ahead. Some of the themes I looked at this past week are:

Why BTC is highly correlated with the S&P 500, but not for the reasons most think (I expand on this more below)

Why messed-up energy politics create a longer-term opportunity for the crypto industry

Why the unemployment data releases don’t matter that much

If you’re interested in more frequent and deeper updates, consider subscribing – you’ll also get access to the rather clunky archives (I’m still figuring Substack out).

And if you find this at all useful, please share with friends and colleagues.

Correlations Aren’t Correlating

“Bitcoin is correlated!” I often hear that thrown out in macro conversations as a dismissive way of saying that it isn’t really an “alternative” asset at all and that all this mumbo jumbo about it being external to the broader economy is just hopium. But very few who say this have actually dug into the data or thought about the reasoning behind that claim (which is understandable – why mess with convenient narratives). I confess that even I used to think that the surge in the correlation between BTC and the S&P 500 was because the institutional investors marched into the market in the second half of last year. Now I’m not so sure – the institutions did indeed march in, and bitcoin is to a large extent a macro asset now. But I don’t think that’s driving the correlation data.

Before we start looking at charts that tell a different story, let’s have a think about what correlation actually means, and why we care. In theory, correlation is simply the measure of the degree to which the movements of two series are related. It measures how much two measures vary together, divided by how much they usually vary individually. (There are other types of correlation with different formulas, but that’s too nerdy to get into here – for those that care, I use Pearson for time series on a rolling 60-day window.)

Imagine two assets that are clones of each other. How much they move independently will be exactly the same as how much they move together, so ratio between the two factors will be 1. A correlation of -1 means they move perfectly in the opposite direction. A correlation of 0 means there is no obvious relationship between the two.

In reality, these “perfect” situations never exist. Correlations are generally a messy amalgam of erratic behavior that indicates strong or weak relationships, used by investors to design relatively robust portfolio strategies and by analysts and storytellers to spot changes in trends.

Yet one trap many fall into is to treat correlation as a binary condition. To say something “is” correlated is vague and inaccurate. Highly correlated, negatively correlated – those qualifications make sense, yet even then, only at a specific point in time. As we will see further down, when it comes to market relationships, especially concerning an asset as young as bitcoin, things change fast.

Another frequent trap is to assume that a high or low correlation can explain behavior. To some extent this is true – but more often than not, the relationship is coincidental even if related. Ice cream sales and cases of sunburn are highly correlated – but one does not cause or explain the other.

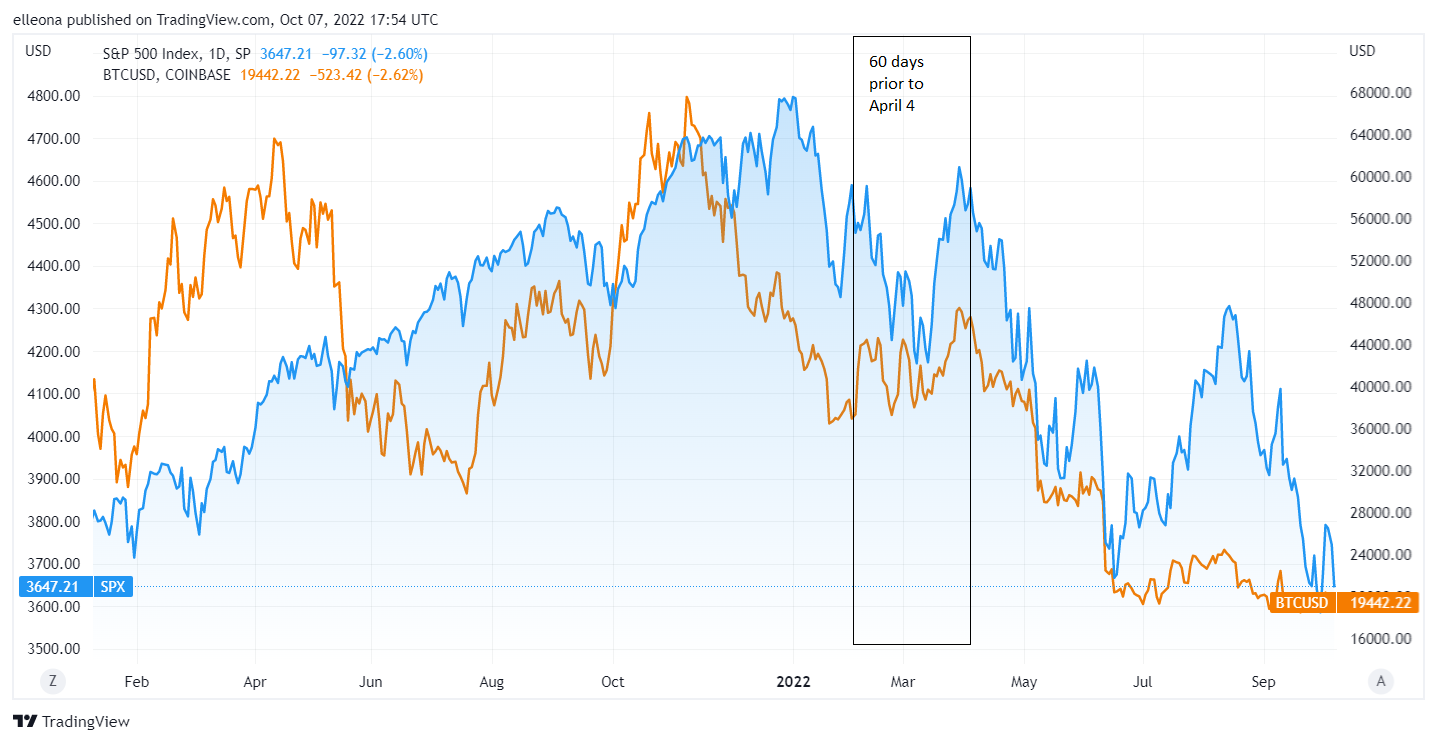

Right, back to bitcoin. As you can see below, it used to be pretty much uncorrelated to the S&P 500 (oscillating around 0), but something changed in April of this year.

(chart via Coin Metrics)

What changed? The overall market mood. Correlation is more about the direction than the size of the price moves (although both matter). The below chart shows that, up until the time that the 60d BTC-S&P 500 correlation had crossed 0 on the way up (never to return?), the two series had sort of been moving in sync but not really. By April 4, the S&P 500 was down 0.7% on the year while BTC was down 7.5%, and the 60 days prior (the snapshot for the correlation calculation on any given day) showed different trends for each.

(chart via TradingView)

What triggered the mood change? Interest rate expectations. Fed funds above 2.50% started to become a remote possibility in terms of market pricing in early April 2022 (when the actual range was 0.25% to 0.50%).

(chart via CME)

This freaked the market out, and the macro investors that had happily piled into the crypto market over the previous 9-10 months exited in a hurry. They didn’t just exit crypto (a high-risk asset relatively easy to sell), they also exited equities. Prices fell across the board, and the 60d correlation between bitcoin and the leading stock index rocketed up to an all-time high of 0.72. Macro investors weren’t the only ones de-risking – crypto fund managers were also exiting, expecting a general market slump. The spike in correlation was not because bitcoin was now a “macro asset”. It was because bitcoin, along with other “risky” assets, was being hit by expectations of monetary tightening. Semantics, perhaps – but it matters, for the same reason that sunblock manufacturers are in a very different business than ice cream makers even though their sales can move together at certain times of the year.

Then, in mid-May, came the implosion of the Terra ecosystem. This was a crypto-specific crisis, and, unsurprisingly, correlations fell as the damage far exceeded that in equities. The de-leveraging triggered by the collapse of hedge fund Three Arrows Capital led to a further de-coupling.

(chart via Coin Metrics)

With that digested, correlations are on their way up again. But this is not, contrary to common perception, necessarily because bitcoin and stocks are joined at the hip. There’s an old adage that says that “in times of fear, all correlations go to 1”. We are in times of fear. But bitcoin and stocks have very, very different value premises, so we cannot assume the correlations will remain high.

That said, bitcoin is a macro asset in that it is part of the global market. The text for the EU’s long-awaited crypto framework was finalized this week, affirming and legalizing the ecosystem’s position in the financial landscape. Legacy institutions from multiple jurisdictions are building or investing in crypto businesses. Regulators around the world are working out how to support the inevitable innovation while protecting their constituents.

So, it is correct to say “bitcoin is macro”, now and going forward. To say “bitcoin is correlated”, however, requires more nuance and explanation, especially to emphasize that the numerical relationship may be convenient for the moment, but it does not mean what many think it does.

A YEAR AGO

(This section will contain a look-back at what was going on this time last year, so we can see how far we’ve come and how far we haven’t.)

BTC - $53,670 || ETH - $3,566 || S&P 500 - 4395

Oct 4, 2021 - Citadel's CEO says regulatory uncertainty is keeping the firm out of crypto. Fast forward almost a year to mid-September 2022, and Citadel – along with other names such as Charles Schwab and Fidelity Digital Assets – is launching a crypto exchange called EDX markets.

Oct 5, 2021 - US Bank launches a bitcoin custody service. In 2020, the then-head of the Office of the Comptroller of the Currency (OCC) Brian Brooks said in an official statement that banks could custody crypto assets. Several known names went to work, announcing custody service plans over the ensuing months. Then Michael Hsu, who took over as Acting Comptroller of the Currency in May 2021, walked that back and now many banks’ custody plans are in limbo.

Oct 6, 2021 - George Soros' family office’s CEO confirms that the fund manager’s personal investments include bitcoin. I’m currently reading “More Money Than God”, by Sebastian Mallaby (riveting), which talks about the legendary figures that created today’s hedge fund industry. I’ve just finished the section on Soros, so this look-back feels meaningful. He sure knew how to read geopolitical and social trends.

KEEP AN EYE ON…

(Three main themes from the week, explored in more detail in the daily emails.)

Tokenized securities. We saw two notable developments in this field this past week: US-based fund manager Hamilton Lane, with over $800 billion in AUM, will offer investors exposure to equities, private credit and secondary investments via tokenized feeder funds (KKR launched a similar initiative back in September). And UK asset manager Abrdn has joined the governance council for distributed ledger Hedera Hashgraph, ostensibly to continue its exploration of the tokenization of traditional securities – a few weeks ago, it became the largest external shareholder in the digital securities exchange Archax.

Crypto mining. YPF – 51% owned by the Argentinian government – is piloting a project that supplies waste gas to a bitcoin mining project, a step forward in global acceptance that bitcoin mining is not necessarily “bad for the environment”. We also have the launch of Grayscale’s fund to invest in distressed mining assets, which implies the firm expects a meaningful flow of crypto mining closures. Bitcoin difficulty is about to kick up another notch, so there will be some more pain, and miners liquidating BTC holdings could add to sell pressure.

More exploits. BNB Chain lost at least $100 million in crypto via a vulnerability in the native cross-chain bridge between two components of its ecosystem. The BNB team was apparently able to freeze the chain to prevent further damage by contacting all 26 active validators. This is not a good look, either for bridges or for decentralization.

GOOD READS/LISTENS

An excerpt of Chainalysis’ upcoming 2022 Geography of Cryptocurrency report, which looks at adoption in the Middle East and North Africa, offers a welcome reminder that crypto is not all about speculation.

Arthur Hayes’ musings seem to be heading more into the field of macro, which I for one totally welcome – always a good and original read. This one covers the sustainability of current adaptations of monetary policy.

An interesting thread by @ErikSTownsend on how the OPEC+ oil cuts are not what they seem but how the oil market might be in for some trouble anyway.

Data centers usually upgrade their servers every 3-5 years. What happens to the old ones? Often, they are shredded to avoid possible data leaks. What if they could be reliably and safely wiped clean and resold?

Podcast: Bitcoin Fundamentals – BTC098, with Jason Lowery, a mind-blowing exploration of proof-of-work vs proof-of-stake systems using examples in nature.

Podcast: Hidden Forces – A fascinating conversation about the role of and outlook for the dollar – Michael Howell’s intervention around 1’07 is particularly compelling, but seriously, all the speakers are excellent.

Have a Good Weekend!

This is not exactly a new song (Nobody Speak, 2016) from DJ Shadow and Run the Jewels, but I’m sharing it anyway because it’s such a great video. It also feels unfortunately appropriate for the breakdown of our times.