Wobbly markets, resilient BTC

plus: what's ahead for the week, China's positioning and more

“A person hears only what they understand.” – Johann Wolfgang von Goethe ||

Hi all! I hope you got to disconnect some this weekend.

Today’s email will be relatively brief, as I had a schedule squeeze this morning (post-surgery eye revision, all looking good!). Plus, the lack of synchronization between US and European daylight savings time means I need to TRY to get this out an hour earlier. Whyyyyy do we even still have daylight savings time, seriously?

Tomorrow I should be able to share an update on key stablecoin developments – today is mostly macro and markets.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

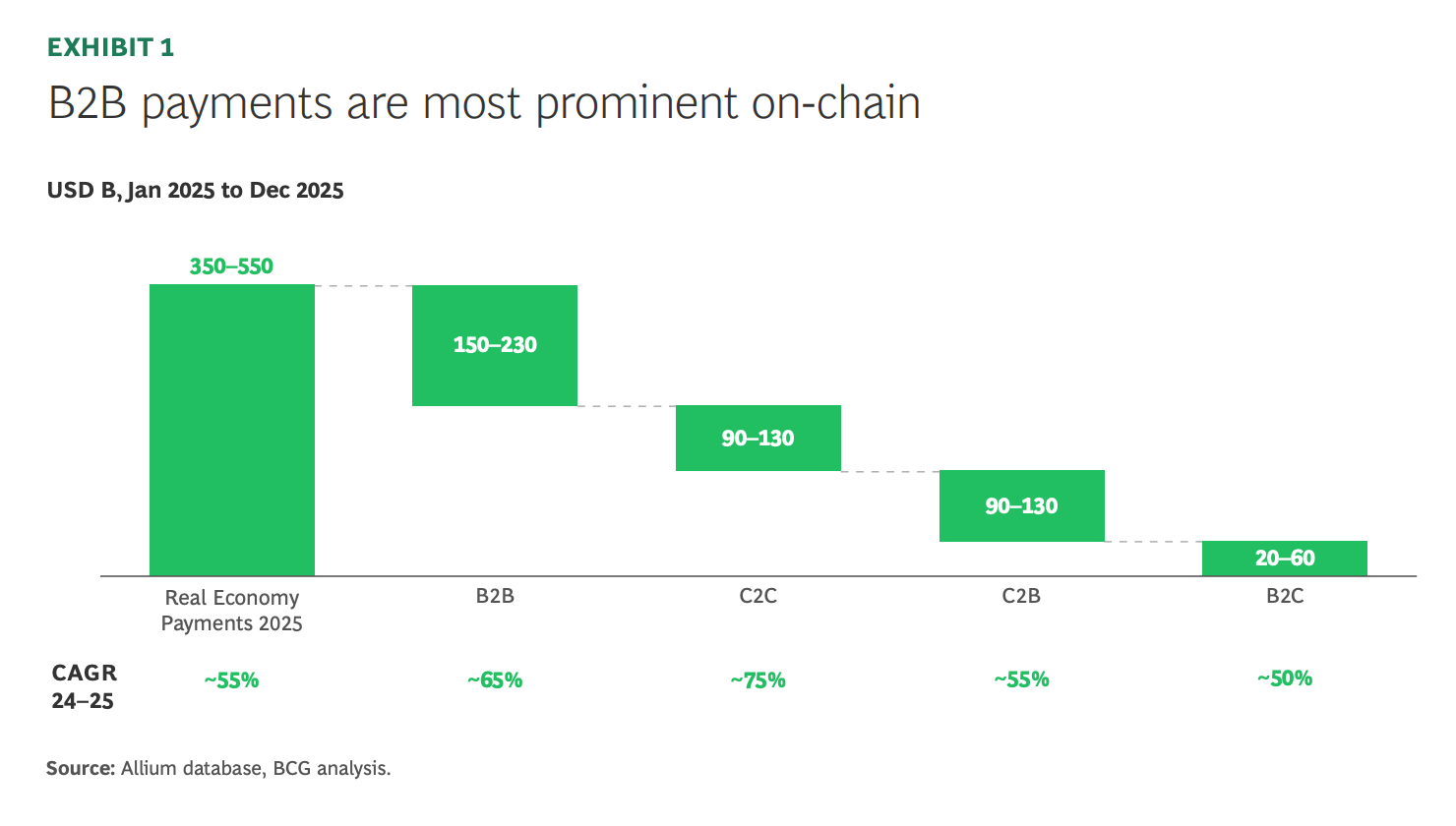

The latest whitepaper published with BCG, Stablecoin Payments: The Truth Behind the Numbers, examines how stablecoins are being used in the real economy today. The analysis estimates $350–550B in on-chain payments in 2025, led by $150–230B in B2B activity, with consumer flows contributing another $200–320B.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Coming up this week:

Markets: sentiment turns

BTC: surprising resilience

Macro: China

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

Coming up this week:

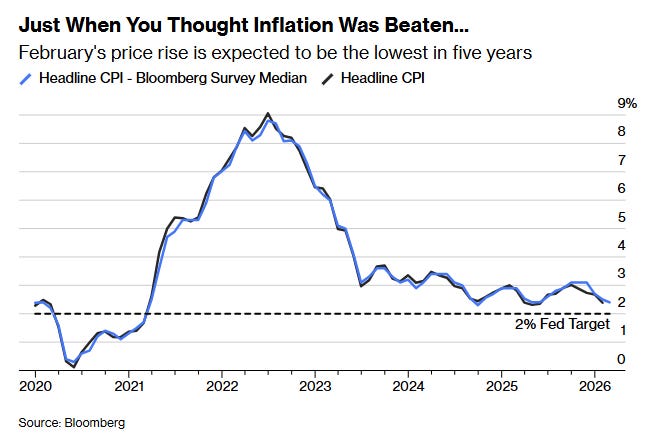

US inflation data this week – not sure the markets will pay much attention given the now chronic uncertainty as to the duration of the oil shock and its impacts.

On Wednesday, we get the US CPI for February, with expectations pointing to a month-on-month increase of 0.2%, the same as in January, while the core index ex-food and energy is forecast to decelerate slightly from 0.3% month-on-month to 0.2%. Year-on-year, the headline index is expected to accelerate slightly from 2.4% to 2.5%, while the core index could decelerate to 2.4%. It’s worth bearing in mind that these indices were compiled before the steepest weekly jump in retail gasoline prices since 2022.

(chart via Bloomberg)

On Friday, we get the second US inflation measure of the week: the Personal Consumption Expenditure (PCE) index, the Fed’s preferred price gauge, is forecast to hold steady with a 2.9% year-on-year increase, while the core index ex-food and energy is expected to accelerate from 3.0% to 3.1%.

We also get the second estimate of the US GDP growth for Q4 – the first estimate showed a deceleration from 4.4% in Q3 to 1.4%.

We get the January growth in US durable goods orders, forecast to decelerate but remain in growth territory.

And we see the latest consumer sentiment report from the University of Michigan – we’ll probably see inflation expectations pick up.

✨ Use the discount code MACRO for 20% off! ✨

Markets: sentiment turns

When the market opened last night, the price of Brent crude shot through the psychological shock barrier of $100/barrel as traders position for what is already the worst oil supply shock in history, in terms of number of barrels disrupted.

(Brent crude, $/bbl chart via TradingView)