Stablecoins and geopolitics in Africa and the ME

Plus, market narratives, a sigh of relief, and why BTC isn’t decoupling

“Our Age of Anxiety is, in great part, the result of trying to do today’s job with yesterday’s tools and yesterday’s concepts.” – Marshall McLuhan ||

Hello everyone! I hope you’re all taking care of yourselves.

Today I step back from geopolitical drama (with a superficial revisit in the Markets section below) to dive into stealth geopolitics via stablecoins. It feels good to dilute the noise with a slow but transformative story for a change.

Apologies for the late publish – it turns out the story got more interesting the more I dug.

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

As traditional finance and crypto converge, trusted data is the missing infrastructure layer. Allium provides this data foundation for teams like Visa, Stripe and Grayscale.

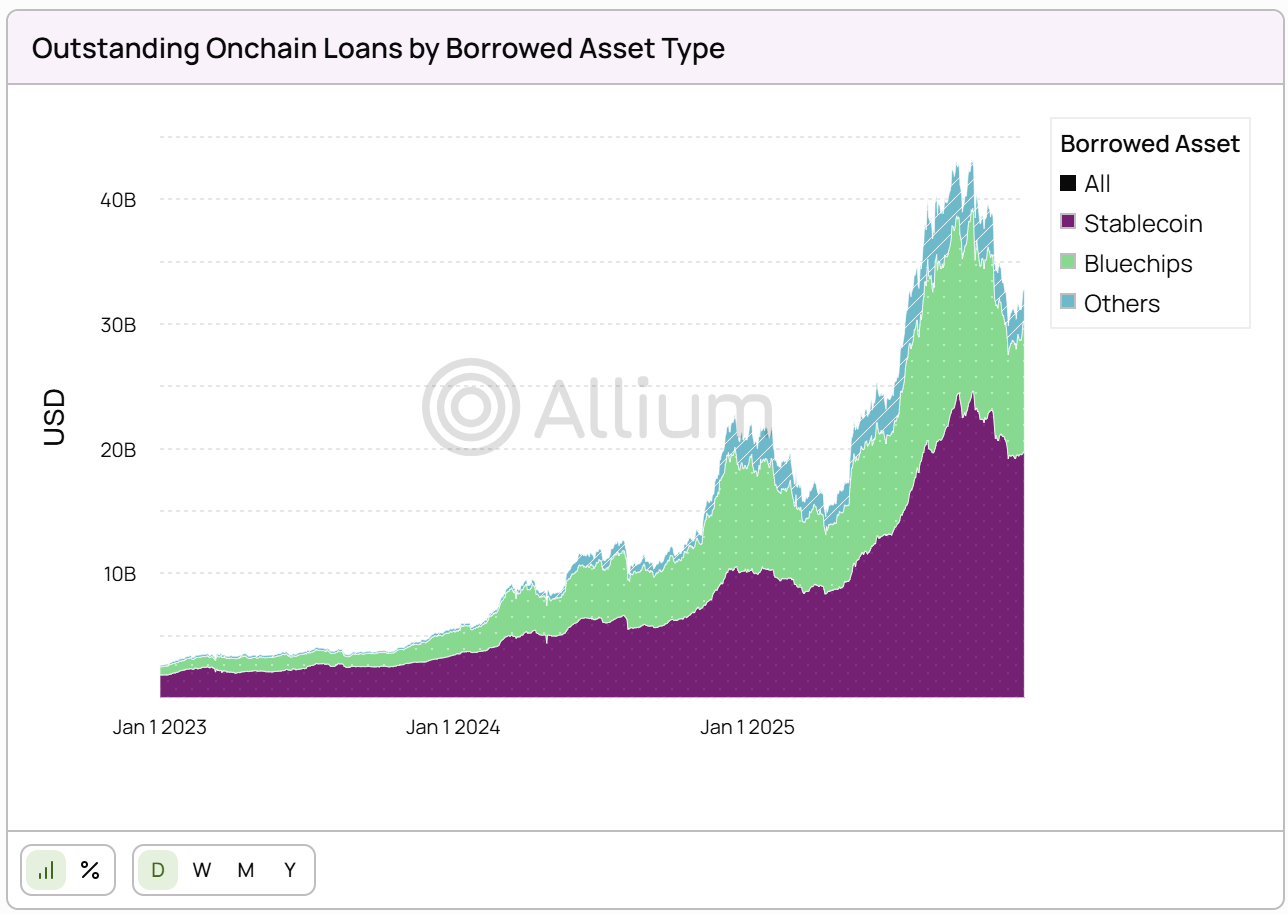

Our latest whitepaper published with Visa, Stablecoins Beyond Payments: The Onchain Lending Opportunity, examines how banks can access emerging credit markets. Looking at the data, outstanding onchain loans reached over $40Bn this year, with stablecoins making up more than half of borrowed assets.

If you’re producing institutional crypto research or analytics, start with trusted data. Explore a live demo.

IN THIS NEWSLETTER:

Stablecoins and geopolitics in Africa and the ME

Markets: no, BTC hasn’t “decoupled”

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links, a music recommendation (‘cos why not?), and more.

If you’re a premium subscriber, thank you!! ❤

WHAT I’M WATCHING:

Stablecoins and geopolitics in Africa and the ME

A low-key announcement last week was surprisingly overlooked, given the significance of its potential impact. It’s to do with stablecoins, like so many headlines these days. But it’s also about regional and global alliances as well as the big-picture focus on digital tentacles and strategic flow-through.

The story starts with an unbanked population, pre-paid phone minutes and a widespread network of agents; it potentially ends with the dirham as the “reserve currency” of Africa while China cements its dominance in the continent’s mineral extraction and trade.

The key players are M-Pesa and the ADI Foundation, who last week announced a blockchain and stablecoin partnership. The stage is cross-border payments. And China is lurking in the background.

Player 1: M-Pesa

Back in the early 2000s, Safaricom – partly owned by Vodafone and the country’s leading telecommunications network at the time – noticed that people were starting to share pre-paid mobile phone minutes with relatives and also exchange them for goods and services. In 2005, it initiated a pilot with microfinance institution Faulu Kenya that would allow the repayment of microloans in instalments using airtime which could be bought in bulk from participating agents – the idea was to remove the need for borrowers in villages, where most of the loans were disbursed, to have to regularly travel into the city.

After receiving a no-objection letter from the central bank, the pilot pivoted from the exchange of airtime to the distribution of e-money. M-Pesa launched in 2007, offering mobile money accounts to anyone with a Safaricom phone number. Users could go to an agent (often just a hut on the side of the road) and exchange cash for an electronic balance, with deposited funds held in trust at a commercial bank for 1:1 backing (not all “stablecoins” require a blockchain, who knew). At the public launch in 2007, anyone with a Safaricom phone number was able to open a mobile money account.

Growth was astonishingly fast as, at the time, almost 75% of the population did not have a bank account – M-Pesa offered a convenient alternative. (I wrote about this for CoinDesk back in 2017 – how time flies!)

After initial resistance and intense lobbying from the banking industry to get M-Pesa either regulated like a bank or shut down entirely (sound familiar?), official support for the project’s financial inclusion potential eventually encouraged banks to focus on the growth opportunities: more people involved in digital banking, even on a different system, meant a greater need for onramps as well as demand for loans and other banking services. What’s more, M-Pesa changed Kenya’s banking industry for the better, forcing banks to compete by lowering account thresholds, dropping transfer fees and accelerating the development of mobile banking. (I wonder how many US banks are familiar with the M-Pesa case study.)

The growth rapidly seeped into neighbouring nations. In 2008, M-Pesa expanded into Tanzania, a couple of years later into South Africa, and today operates in eight African countries.

An interesting twist is M-Pesa’s rejection and then embrace of “crypto”. Just as banks initially opposed the idea of competition from Safaricom, the telecom operator hated the idea of competition from blockchain networks and moved to have them shut down, rejecting any form of collaboration and denying blockchain businesses access to its network.

But in December, reports emerged that M-Pesa was pivoting on this strategy via a partnership with the Abu-Dhabi based ADI Foundation.

Player 2: the ADI Foundation

Created in 2024 to build compliant digital asset infrastructure for governments, institutions and retail, the ADI Foundation is backed by the digital arm of the second-largest listed entity in the MENA region, International Holding Company (IHC). The head of IHC is Sheikh Tahnoon bin Zayed Al Nahyan, who is also chair of the UAE sovereign wealth fund, its two largest AI companies, the Emirates’ largest bank as well as a few other technology and holding companies. In addition, he’s the UAE’s National Security Advisor as well as its Deputy Ruler and brother to the President. Last March, he was hosted at the White House where he reportedly met with the US Treasury Secretary, the head of the CIA, Jeff Bezos and other global movers – the man has clout. And I should mention that one of his investment firms last year bought $2 billion worth of USD1, the stablecoin issued by World Liberty Financial (controlled by the Trump family), which was then used to buy a stake in Binance. I know, my head is spinning just writing this.

Last month, the ADI Foundation launched the mainnet and token of ADI Chain, a compliance-oriented EVM-compatible layer-2 built on the zkSync stack. A few days later, it signed MoUs with BlackRock, Mastercard and Franklin Templeton to extend use of digital asset infrastructure in the region.

Launch of a dirham-backed stablecoin is expected in coming weeks, to be issued by the Emirates’ largest bank, First Abu Dhabi.

The stage: cross-border payments

Under the terms of the above-mentioned deal, M-Pesa will integrate ADI Chain into its network and facilitate movement of the dirham stablecoin across its 60 million accounts in eight countries. That’s significant potential stablecoin scale, from a mobile money business already deeply entrenched in African money flows.

The advantage? A widely accepted token for cross-border transfers. The African payments landscape is fragmented, with payments to even neighbouring countries often met with the considerable friction of intermediaries and relatively high costs, especially given the illiquid nature of most currencies on the continent.

The dirham, in contrast, is both relatively liquid and stable, given its considerable international flows and its peg to the dollar. Put differently, it is a better “store of value” than local currencies. But it is not yet widely accepted as a settlement currency in sub-Saharan trade.

Could this change? The UAE is the fourth largest foreign investor in the region, and has plans to ramp up its involvement. Could the dirham eventually become a de facto “reserve currency” for the region?

Stablecoins are already widely used in the region – mainly USDT – but there is as yet no widespread network “compliant” enough for official acceptance. ADI Chain hopes to become that network, leveraging the influence and reach of M-Pesa and offering a deeper integration with a global financial centre.

Could it be a threat to USDT use in the region? I doubt it – most current users will probably continue to find dollars preferable to dirhams, and could be wary of the “compliance” angle. But new corporate and even sovereign users could find the ADI option a palatable onramp.

So, the ADI/M-Pesa deal is significant, given the potential volumes and connectivity. But there’s more going on. Stepping back, here we have another example of the geopolitics of stablecoins.

In the background: China

To start with, we have the UAE seeing an opportunity to expand its financial services, plugging into an already extensive network and offering a gateway for businesses on the continent to access new rails and new markets.

It’s ingenious, especially when you consider the UAE’s role in global payments and its work on becoming even more significant as a finance node, leaning in to its inadvertent branding as “the capital of capital”. Given its origins as a trading post and its key geographical location, it has a long history of multi-currency flows, and its ability so far to stay out of the grand power tussle around global trade makes it a relatively trusted partner for most. Some of India’s imports of Russian oil, for instance, are settled in dirhams. Meanwhile, the UAE’s aggressive work on blockchain infrastructure build with regulatory support represents investment in the currency flows of tomorrow.

Until Saudi Arabia joined in mid-2024, the UAE was the only non-Asian member of the mBridge platform, a multi-CBDC initiative developed by its central bank along with those of China, Hong Kong and Thailand. China is the UAE’s largest trading partner, the UAE is China’s largest export market in the Middle East (COSCO has a terminal at Khalifa Port), and there are reportedly more than 15,000 Chinese firms operating in the Emirates. Last March, China’s Cross-Border Interbank Payment System (CIPS) and the UAE Central Bank signed an MoU to enhance cross-border payment cooperation. And in November, the UAE and China completed their first cross-border CBDC payment, not on mBridge but via a separate bilateral platform.

So, the UAE is going full speed ahead on enhancing its global finance role. A significant leg of this lies in developing digital asset infrastructure to be used not just by institutions and individuals in the region, but by sovereigns and businesses anywhere that want to transact with or via the Middle East. Of course, large US institutions will want to participate in this rollout, given the potential volumes on the table. And the door will be open to US participation, especially since the UAE really wants a guaranteed supply of US-made AI chips.

But the UAE is also hedging its bets and leveraging its role as a long-standing anchor between hemispheres. It is deepening its digital payments development with its largest trading partner, China. And at the same time, it is forging paths into the potentially vast field of African cross-border payments via stablecoins and mobile accounts.

Bear in mind that China is by far the largest foreign investor in mining and other resource extraction in sub-Saharan continent, and you can see not just new networks taking shape, but also the long game of how stablecoins and CBDCs can shape the realignment of global power.

Perhaps you thought that stablecoins were all about dollarization?