WEEKLY: Money <> securities, central banks <> BTC

plus, country music

Hello everyone, and welcome to February!

You’re reading the free weekly Crypto is Macro Now, where I reshare/update a couple of posts from the week, and include something from outside the crypto/macro sphere that is currently inspiring me (it’s a fascinating world out there).

If you’re not a subscriber to the premium daily, I do hope you’ll consider becoming one! For $12/month, you’ll get ~daily commentary on how crypto is impacting the macro landscape, and vice versa. I talk about adoption, regulation, tokenization, stablecoins, CBDCs, market infrastructure shifts and more, as well as the economy and investment narratives.

Feel free to share this with friends and colleagues, and if you like this newsletter, do please hit the ❤ button at the bottom – I’m told it feeds the almighty algorithm.

In this newsletter:

Circle and Hashnote: melding money and securities

Central banks and BTC: it’s an age thing

Some of the topics discussed in the dailies:

The perils of concentration

Market reaction

Something else?

Looking ahead

The cycle inflection point

Can blockchains deliver cost savings?

Circle and Hashnote: melding money and securities

BUIDL as collateral

Fintech stablecoins

Tether expansion

FOMC bookends

Central banks and BTC: it’s an age thing

Circle and Hashnote: melding money and securities

One of the most intriguing announcements over the past month was stablecoin issuer Circle’s purchase of tokenized money market fund issuer Hashnote.

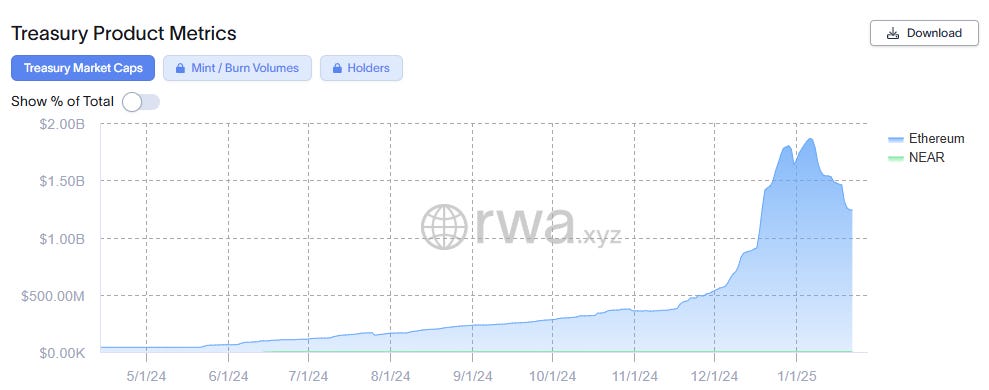

With this move, Circle takes over the market’s largest tokenized money market fund USYC, which passed previous market leader BUIDL, issued by BlackRock and Securitize, in assets under management (AUM) at the beginning of December. Hashnote’s flagship token went on to reach a peak of $1.8 billion market cap earlier this month; since then, it has declined by roughly a third but still stands at almost double that of the runner up.

(USYC market cap via rwa.xyz)

The purchase raises a key question: why would Circle want to acquire a much less profitable business, rather than focus on increasing demand for its stablecoin USDC? Hashnote distributes 90% of yield earned on underlying securities to token holders; Circle, on the other hand, gets to keep it all.

One likely reason is that the boost in size should give Circle a higher potential IPO value – its S-1 was filed in January of last year, although as far as I know we haven’t seen further details as to amount or timing.

The immediate bump in AUM isn’t much, though, in relative terms. USYC adds roughly $1.2 billion to USDC’s almost $52 billion.

(USDC market cap via Visa)

And the potential market is more limited, as USYC is only available to qualified investors, while USDC can be used by anyone.

The sum is greater than the parts

Looking ahead, the boost will come more from synergies and increased liquidity in both. Circle is entering into a partnership with key market liquidity provider DRW and its crypto arm Cumberland (from whose incubation lab Hashnote emerged in 2023), to deepen available pools of USDC and USYC.

Working together off exchanges, USDC and USYC can support each other’s liquidity via smart contracts. Currently, USYC enables funding and redemption 24/7 via the web page. Originally, this functionality was fed by PayPal’s stablecoin PYUSD; now, USDC is also an option, and given the token’s superior liquidity, is likely to become the main settlement token. What’s more, acting as an on- and off-ramp for USYC gives USDC yet another use case and driver of demand as well as circulation.

It's this easy conversion into and out of yield-bearing assets that is, in my opinion, the key to the whole deal. It’s more than just a new service – it leverages the utility of both flagship assets. And it nudges forward the transformation of how money works.

With seamless switching, traders, crypto businesses and other regular users of stablecoin USDC can convert their holdings into a yield-bearing asset, instantly, with little more than the push of a button. “Money” now earns a yield.

Of course, this is also available in traditional markets, but not without several intermediate steps and probably an entity to advance the funds or securities on credit. In traditional markets, money and securities move on different rails, which complicates switching. On blockchains, they’re on the same rail, and actual, no-credit-involved switching happens in seconds.

The opportunity to make your on-chain money “work” for you more, with no opportunity cost, would have obvious appeal to regular crypto users. It should also appeal to tradfi entities looking to lock in a yield-bearing asset with convertibility into a token that can be transferred anywhere at any time – no need to wait for business hours. Imagine the utility for corporate treasurers: a yield-bearing token that can act like money thanks to instant swaps at any time of day.

But this does more than just put money to “work” more efficiently. It also enables the symbiotic interchange between an asset meant to move, and an asset meant to stay put.

I’ll elaborate: Tokenized treasuries and money market funds are meant to stay put and earn a yield. They can easily move, sure, but that’s not their purpose. This does not mean they are only held in wallets earning passive income – increasingly, tokenized assets are used as collateral. USYC, for example, is accepted as collateral on the Deribit and QCP platforms, and more agreements like this are no doubt forthcoming. Tokenized treasuries and money market funds are an attractive collateral: “safe” (backed by the US government), easy to transfer, and able to plug into smart contracts that can pay part of the yield to the trading venue.

Stablecoins, on the other hand, are meant to circulate. They are the most popular form of “money” in the crypto ecosystem, and can solve issues of liquidity and settlement with their ability to whizz around the world in minutes, at any time of day, any day of the week. But, much like cash, they’re only useful when they’re moving. There’s an argument to be made that having them available offers “optionality” which many will find useful, just as you might keep a few bills in your physical wallet. But that optionality comes with an opportunity cost that is only justified if the tokens eventually move.

With seamless switching, on-chain cash essentially starts to earn a yield. And, yield-bearing tokens essentially can act more like cash even if their transferability continues to be restricted.

There’s more

A few other points of interest in Circle’s announcement:

The move could also partly be a bet on stablecoin demand growth. This would of course benefit USDC, but also USYC given its use as reserves for stablecoins such as Usual’s USD0 stablecoin – this was responsible for the tokenized money market fund’s surge starting last October. In a similar vein, BUIDL is now used as reserves for Frax’s stablecoin (more on this below). For stablecoin issuers, tokenized treasuries are more flexible than traditional bonds in that they can be mobilized or liquidated at any time, rather than wait for business hours.

While market leadership for stablecoins is likely to remain in the vaults of Tether’s USDT and Circle’s USDC, coming regulation could free up market diversity and encourage more stablecoin launches, potentially increasing demand for USYC. It’s notable that Stripe recently paid over $1 billion for stablecoin issuance platform Bridge.

The move is also likely to be a bet on increasing tradfi participation in crypto networks. As part of the news drop, Circle revealed that USDC is launching on Digital Asset’s Canton network, an enterprise-facing interoperability public blockchain that not only connects crypto ecosystems, it can also connect blockchains with centralized databases. It is already used by several large tradfi institutions such as Goldman Sachs, HSBC, Broadridge, BNP Paribas, Bank of America, Clearstream and many others – this doesn’t include participants in the initial pilot, which would expand the list considerably.

USYC is already available on Canton. The incorporation of USDC broadens the potential utility for tradfi users for reasons mentioned above.

In sum, the Circle-Hashnote deal is smart. I don’t know the price paid but, strategically, there is not just considerable likely market growth ahead – demand for on-chain collateral and yield-bearing tokens is still in the foothills of the adoption slope. It also highlights how the synergies between the two types of asset could enhance the utility of each, while altering our understanding of how money and collateral work.

Central banks and BTC: it’s an age thing

Not there yet, but perhaps almost.

I’ve been predicting for over a year now (and I’ve been wrong on my timing) that we would soon see a non-US central bank holding BTC as part of their reserves.

The Financial Times reported earlier this week that the head of the Czech central bank has proposed that his institution study the possibility of including BTC in its reserves as part of a broader diversification plan, with possibly as much as 5% (roughly $7 billion) ending up in Bitcoin.

This met with swift pushback from European Central Bank (ECB) Governor Christine Lagarde, who said on Thursday:

"I am confident that ... bitcoins won't enter the reserves of any of the central banks of the General Council."

In a post on X the previous day, however, governor Aleš Michl repeated that the idea was under study and that he found it interesting given BTC’s low correlation to bonds. To calm the froth, he added:

“[N]o decision is imminent”.

Two interesting takeaways here:

1) One is that, if the Czech central bank really wanted to diversify its reserve, it could do so without the approval of the ECB. Governor Michl sits on the board of the ECB's General Council, an advisory and coordination body for all EU member states. But, as Czechia is not in the eurozone, it has monetary policy independence.

That said, it’s unlikely Governor Michl will want to antagonize anyone over this issue, at least not yet – but it’s notable the determination to study the idea anyway.

2) This could have a lot to do with Governor Michl’s age. When he was appointed to the position, he was 44, just a smidgen older than the EU’s youngest central bank governor on appointment to date, Lithuania’s Gediminas Simkus, who was 43 when he took office.

It’s not news that the younger generation are more open to the idea of bitcoin and crypto assets than are their seniors. Most central bankers today are in their late fifties to late sixties or even older, and are therefore typically resistant to new technologies and uncomfortable change.

It’s also not news that the current roster of central bankers will gradually “age out”, replaced by a younger generation more in tune with new technologies and with the notion of institutional and cultural independence.

Another interesting detail is that Governor Michl was a fund manager before he became his country’s senior monetary official. In his interview with the FT, he stressed:

“I like profitability.”

This is not typical language for a central banker.

But it is most likely representative of a new shift. As monetary institutions struggle to adapt to a changing landscape, it’s logical that their executives will bring a broader range of experience, most likely substituting the emphasis on economics expertise (since that arguably hasn’t been particularly successful) to one focused on markets.

In sum, the notable part about Governor Michl’s interest in crypto assets is not that an august institution is considering a new type of reserve diversification. It’s that central bankers themselves are changing.

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

I read recently that the surge of interest in country music is indicative of a cultural swing towards individualism, Americana, old-fashioned ruggedness, in line with the results of the US election. I mean, that makes sense, but it’s not that simple – for example, I’m not American, not right-wing, nor am I particularly rugged. Nevertheless, I’ve liked country music pretty much all my life. The storylines, the twang, the brisk chords and harmonies, country songs can be both sad and uplifting at the same time. Melancholy mixed with motivation.

Below are some of my favourite country-ish tunes, none of them particularly new but all of them still captivating in my book.

Boys ‘Round Here, by Blake Shelton (great video)

Mama’s Broken Heart, by Miranda Lambert

Two Black Cadillacs, by Carrie Underwood

That Girl, by Jennifer Nettles

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade.