More roadblocks for the digital euro

plus: digital competitiveness, bank liquidity, Basel stubbornness, Supreme Court odds and more

“Freedom would be not to choose between black and white but to abjure such prescribed choices.” – Theodor Adorno ||

Hello everyone! What a rough day yesterday…

Some news: I have finally launched Cripto es Macro, a “light” version of this newsletter in Spanish. It felt like a logical step as 1) I live in Spain and 2) a few potential readers have asked for it. For now, it will publish 2-3 times a week, it will share less content than this newsletter, and it doesn’t have access to the archive. Also, for now, it’s free – it will move to paid probably in a month or so. If you know anyone that might be interested, do please let them know!

PUBLISHED IN PARTNERSHIP WITH: ✨ALLIUM✨

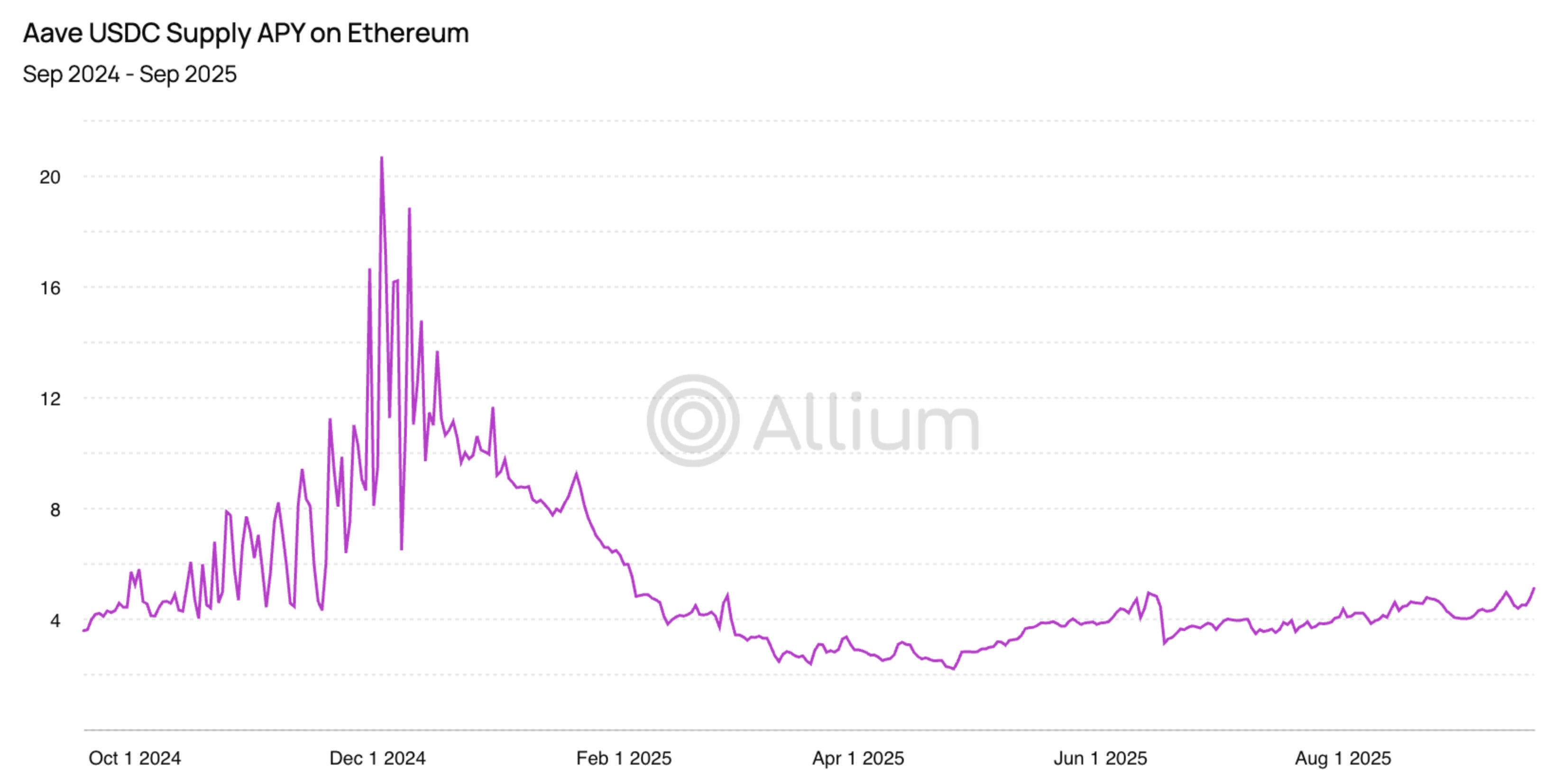

Allium provides vetted blockchain data to answer your hardest macro questions, like:

“How has the lending interest rate of USDC for Aave on Ethereum changed ahead of Fed rate cuts?”

Our data covers 100+ chains and is internally checked for accuracy every 5 minutes. We handle the pipelines and edge cases so you can uncover insights faster with a single, verified data source. Teams like Visa, Stripe, and Grayscale trust Allium to power mission-critical analyses and operations.

For more information: www.allium.so.

IN THIS NEWSLETTER:

More roadblocks for the digital euro

Basel stubbornness

Macro-Crypto Bits: ouch, bank liquidity, Supreme Court odds, digital competitiveness

WHAT I’M WATCHING:

More roadblocks for the digital euro

Today, the European Parliament meets to discuss the digital euro. But it does so amid increasingly vocal opposition.

Fourteen European banks, including Deutsche Bank, BNP Paribas, ING and others, are warning that the digital euro will undermine private sector payment systems – such as Wero, their alternative to Mastercard, Visa and PayPal.

I confess I hadn’t looked into Wero before, as it’s not yet available where I live (Spain) – but according to some cursory research, it’s popular in Belgium, France and Germany where it launched as a pilot last year. While not yet pan-European, its aim is to get there within the next couple of years.

So why, again, do we need a retail digital euro?

We don’t – and Fernando Navarrete Rojas, the European MP charged with ushering the digital euro legislation through Parliament, agrees. He points out that the ECB project addresses the same use cases as private solutions, “without offering any clear added value for consumers.”

He is arguing for a significantly scaled-down digital euro proposal.

In a draft report published on Monday (download link), he suggests some pretty big changes to the EU draft digital euro legislation.

He proposes that the digital euro be limited to an offline solution, leaving online money to commercial bank and other private sector systems. That way, it would represent a digital evolution of cash rather than support the expansion of territory the ECB deems necessary.

He suggests that legislators first establish that a pan-European private payments system doesn’t and can’t exist before proceeding with an online central bank digital currency.

He would like the text to point out that other major economies have ditched retail CBDC plans to focus on wholesale.

And he proposes swapping out language highlighting political support back in 2022 for the digital euro study with the need to consider whether the digital euro addresses “clearly defined problems”, and that it be compared to the “best available market alternatives, in line with necessity, proportionality and opportunity-cost tests”. That’s a hefty dunk.

His text changes will be hotly debated – this is still a draft, after all. And many in Parliament do support the digital euro idea. But Rojas has the backing of Germany’s most powerful bank lobby, which insists that the current plans are too expensive and offer “little tangible benefit for consumers”.

I do think the digital euro is done for – I’ve said this many times before, and convincing signs continue to emerge. Such a seismic change to Europe’s banking industry would need overwhelming political and industry support to get through the tortuous process of legislation without being watered down into irrelevance. Rojas’ draft tells us that the watering down has started.

See also:

Why we won’t get a digital euro, despite the ECB’s insistence (Oct 2025)

The digital euro hits a wall (Sept 2025)

The digital euro gets shakier (July 2025)

The race to the digital euro is getting tense (June 2025)

The digital euro: more smokescreens (March 2025)

Basel stubbornness

The Basel Committee on Banking Supervision seems to have been struck by a glimmer of common sense – but only a glimmer so far.

Back in 2022, the organization entrusted with developing global standards for banking regulation, decided that financial institutions should apply a 1,250% risk weight on cryptoassets held on their balance sheet. Since banks have to hold 8% of the risk-adjusted value of balance sheet assets as capital reserves, this means that for each $1 million of crypto assets, banks have to put aside $1 million of cash as a volatility buffer.

Even for stablecoins on public blockchains.

The crazy part is that the 1,250% weight is the maximum, intended for the riskiest of assets. Private equity, for example, only gets 400%. Yet public blockchain stablecoins backed 1:1 by safe assets and bank deposits are penalized with the maximum risk weighting for running on open, decentralized networks. To avoid this, they would need to migrate to a permissioned network.

Given the global push by the US for greater stablecoin adoption, there is now ongoing debate within the Basel committee as to whether the rules should be modified before they go into effect on January 1. Joining the US in this push is Hong Kong, and Singapore has already said it won’t implement the rules until 2027, citing the need for global alignment. The ECB is happy with the rules as they are, no surprise, even though EU stablecoin regulation stipulates a much lower risk ratio.

The sticking point is not necessarily that public blockchains are risky: it’s that they make it harder to enforce KYC/AML. And that is integral to centralized financial regulation.

So, with the clock ticking, there is much at stake. If the Basel committee refuses to consider a change, we are likely to see banks lose out to non-bank stablecoin providers, yet another example of regulation hurting the sector it is meant to protect. It’s unlikely the US Administration would allow that to happen, so we could see it either delay or water down the Basel crypto requirements – which are, after all, voluntary. Officially, there would be consequences to deviating too far from the global standard-setter, but it would take a brave financial regulator to decide to punish US banks.

But if the US gets away with adjusting Basel cryptoasset rules, other nations may think they should, too.

In sum, this could end up being about a lot more than crypto risk weightings.

🍂 If you find these letters useful, or even if you just like my awesome music recommendations, would you mind sharing with your colleagues and friends and nudging them to subscribe? I’d really appreciate it! 😀

Macro-Crypto Bits

Short-form thoughts on key macro/crypto twists:

Markets: ouch

Yesterday, I wrote that markets were “blech” – well, they went from blech to yuk. BTC at one point briefly dropped below $100,000 for the first time since the brief rout last June.

(BTC/USD chart via TradingView)

The S&P 500 was down more than 1%, Nasdaq was down more than 2%. Japan earlier today was at one point down almost 5% (!!), but rallied into the close to end up 2.5% down.

(Nikkei 225 index, chart via TradingView)

What we’re seeing is both a risk-off exit given liquidity concerns and rates uncertainty, as well as spreading doubts about AI valuations. Softbank, for example, was at one point down almost 15% in Japan trading today, and rallied to close down only (!!) 10%. Palantir was down 8%. The Global X AI ETF closed down over 3.7% on the day.

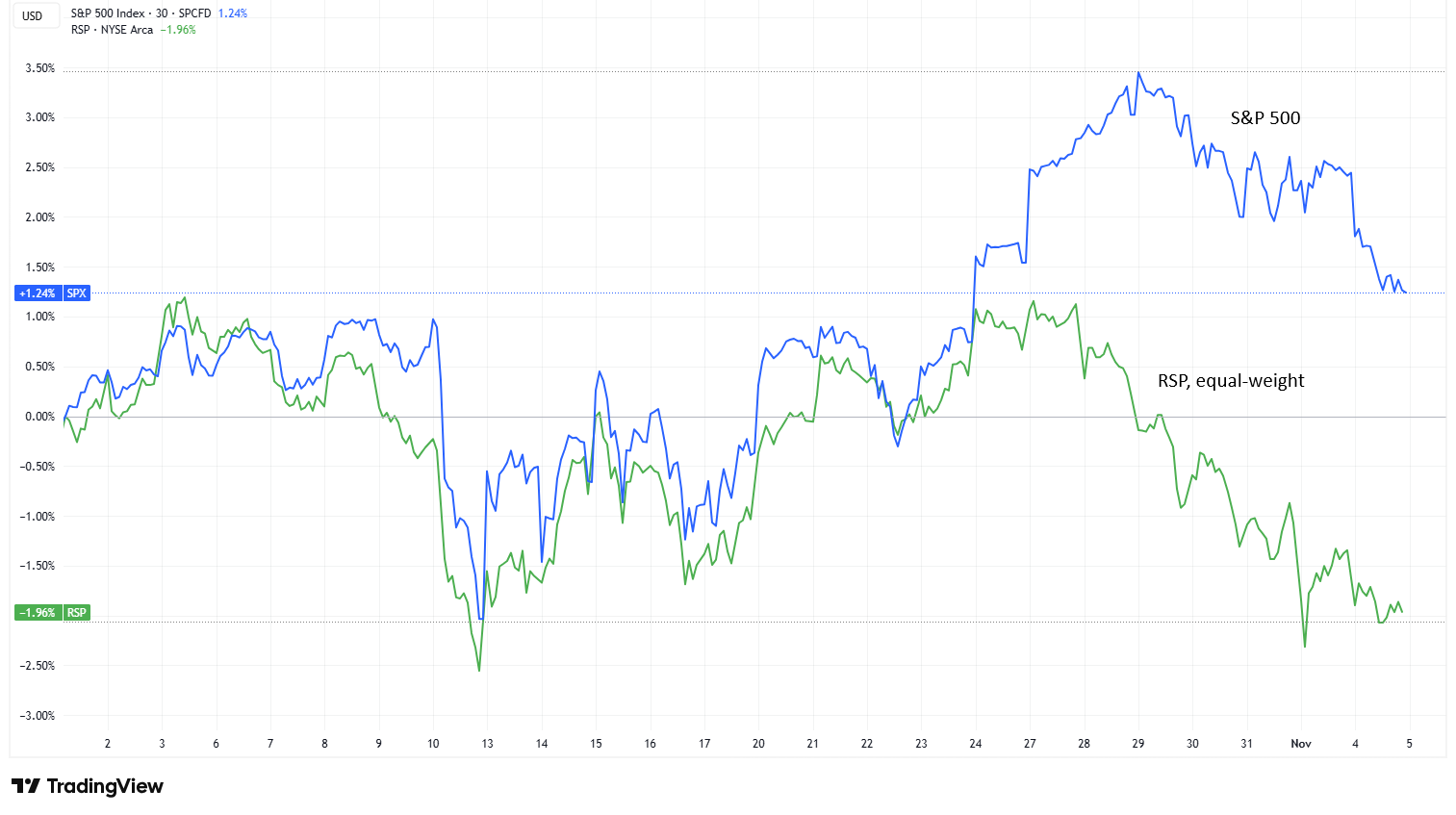

But a large part of this is a reset from the valuation surge over the past week as earnings beats fuelled AI optimism even further. The equal weighted S&P 500 may have fallen less yesterday (-0.7%), but it started dropping last Monday when the big tech names were still climbing.

(chart via TradingView)

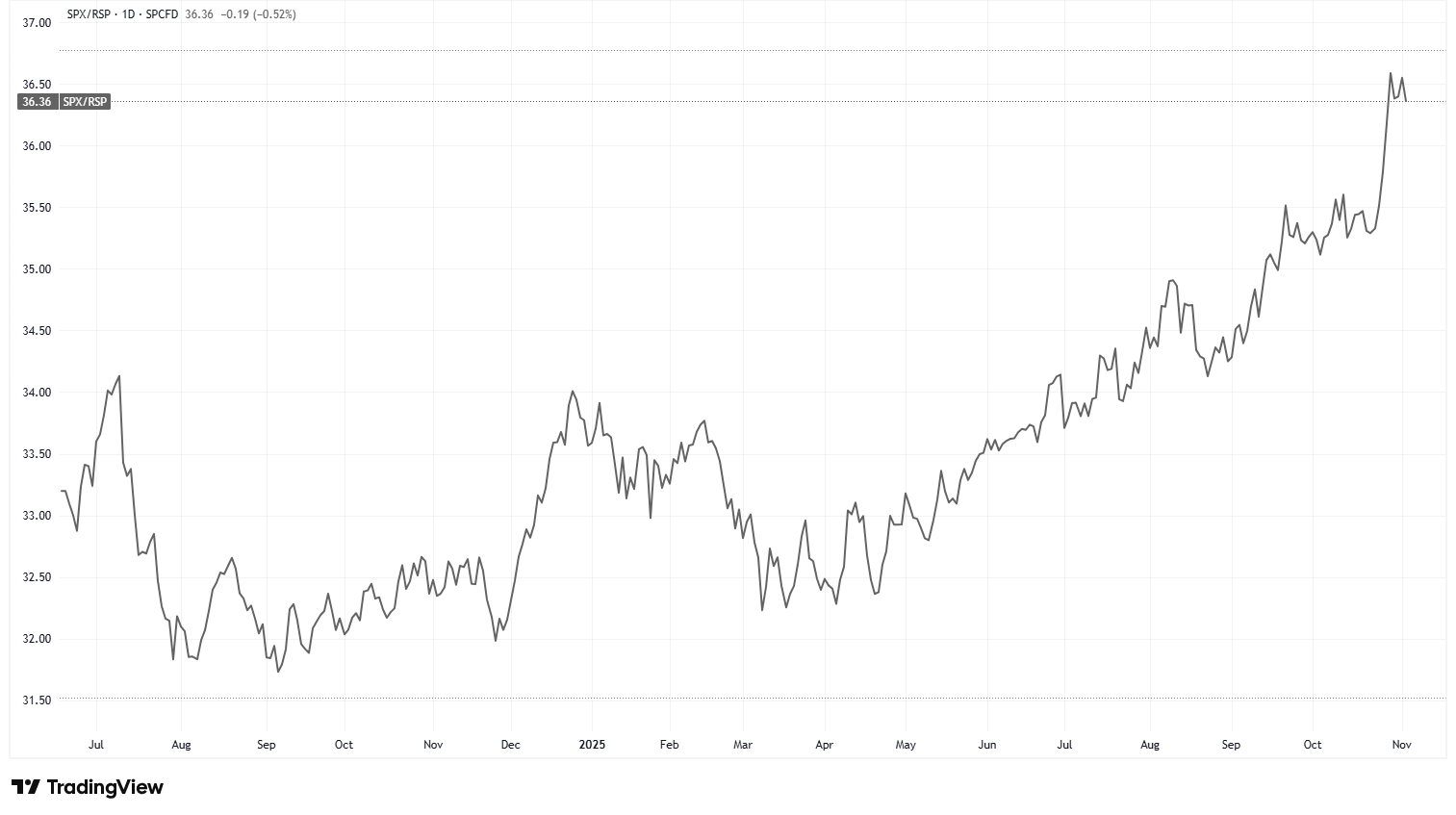

Another way to view the staggering outperformance of the big tech stocks is via the ratio between the market-weight S&P 500 and its equal-weight counterpart – check out that surge in late October as Q3 results came in.

(SPX/RSP chart via TradingView)

So, there’s also some natural correction at work – but AI doubts are part of that.

The rally in both Japan and BTC earlier today suggests that we could see a bounce or at least a breather on the US open – so far, futures are looking neutral.

We’re in a strange market where on the one hand we have plenty of signs equities are overbought and the last time spirits were this high was just before the 2000 bust; and on the other hand, the US economy is not doing as badly as many of us feared in early April – 12 months to the day after he was elected, President Trump seems to have lost his ability to scare markets.

And traders these days are more sharply attuned to good news than bad news, and there are some positive catalysts waiting in the wings.

We should soon start to see signs of the end of the US government shutdown – this will boost activity and start to inject liquidity into the market via the TGA.

We could see more liquidity injections from the Fed to offset building signs of repo stress.

Speaking of which…

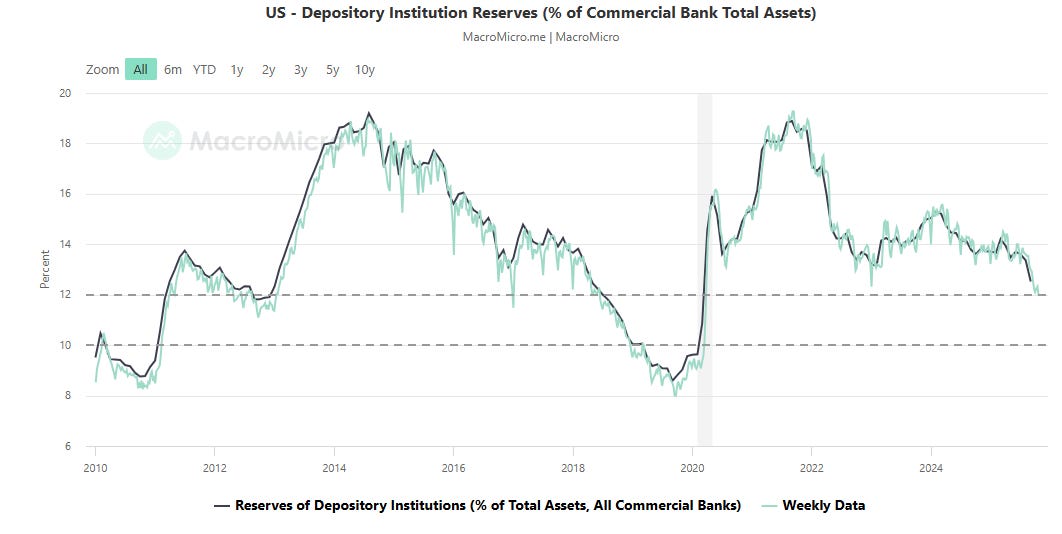

Macro/markets: bank liquidity

Yesterday, I shared a chart showing the repo SOFR rate was spiking, which suggests that liquidity is alarmingly tight.

This is affecting bank reserves, which have been declining as a percentage of total assets and are close to entering the so-called “danger zone” in which, historically, lending rates get volatile.

(chart via macromicro.me)

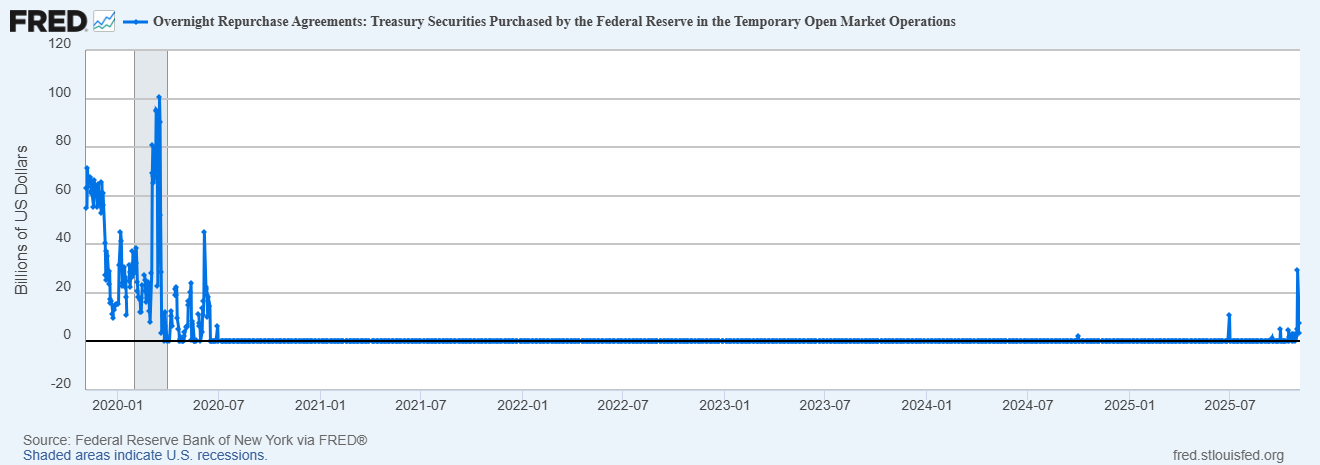

Another sign the Fed is on alert here is the number of times it has seen take-up of its Standing Repo Facility, a backstop overnight repo market for when liquidity is not readily available elsewhere. After a long period of stability after the pandemic, over on the right it’s starting to look not so stable.

(chart via the St. Louis Fed)

Technically, this is not yet Quantitative Easing (QE), in which the Fed buys securities in the market to hold on its balance sheet, as the operations are extremely short-term. But it is liquidity injection, and for the sake of stability, we are likely to see even technical QE soon.

Yet another reason to be longer-term optimistic about risk assets.

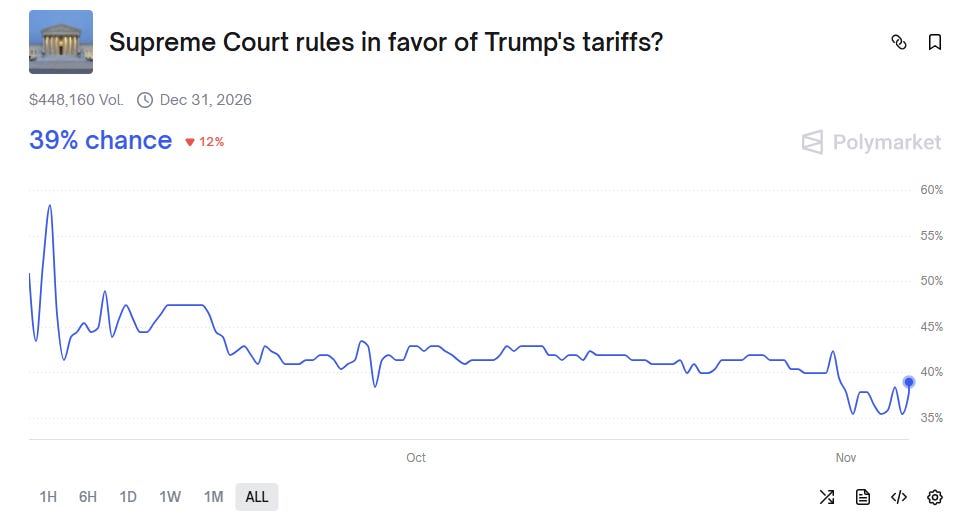

Macro/markets:

I wrote yesterday that the Supreme Court decision on tariffs was a big deal, likely to inject more volatility into markets. But Polymarket suggests that markets are partially pricing in an Administration defeat, so any volatility could be short-lived?

(chart via Polymarket)

This is hard to gauge since we have no idea what the ruling will be. I believe an Administration defeat is likely, which – combined with the Democratic Party wins in local and regional US elections yesterday – could throw more political uncertainty into the already murky soup. But the details will matter for market impact.

Put differently, we don’t know what we don’t know.

Macro: digital competitiveness

Every year, the International Institute for Management Development (IMD) publishes a ranking of “digital competitiveness”, which in its lexicon means “the capacity and readiness … to adopt and explore digital technologies as a key driver for economic transformation”.

It researches and canvasses 69 countries, talking to business leaders and government officials, and compiles its findings into an index that reflects “digital savviness”.

The number one spot in the ranking this year is claimed by Switzerland, which moves up from second.

That place is taken by the US, which has climbed two levels but is held back by the Talent ranking and the Globalization impact.

Singpore comes third, dropping from first.

Perhaps most intriguing of all is Hong Kong’s climb of three places to take fourth, while China sits at 12th.

(chart via IMD World Digital Competitiveness Ranking)

Spain, where I live, is 29th. Italy is 40th. Most of the EU, unsurprisingly, does not shine, with the exception of Denmark (fifth) and Netherlands (sixth).

Do these rankings matter? In detail, no, but stepping back they are a useful gauge for investment in systems and integration. The Hong Kong move is relevant for its goal to unseat Singapore as Asia’s fintech capital, and for its role as gateway into the massive Chinese market. Blockchain technology is mentioned in passing a couple of times in the study, more out of concern for regulatory fragmentation and overlapping yet contradictory priorities from various organizations.

But for connectivity, arguably a key component of digital readiness going forward, blockchain will no doubt play an increasingly significant role.

🎶WHAT I’M LISTENING TO: Strange but with a powerful hook – Sister Rosetta Goes Before Us, by Robert Plant and Alison Krauss🎶

If you find Crypto is Macro Now useful, would you mind hitting the like button? ❤ I’m told it feeds the almighty algorithm.

HAVE A GREAT DAY!

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google (always double-checking facts), but never for writing.

Thanks for the ongoing insights and reporting on digital euro.