The SEC, tokenization and structural change

plus: a new era at the Fed, hawks and doves, and more

“Good questions outrank easy answers.” – Paul Samuelson ||

Hi everyone! I hope you’re all doing well. A special welcome to new subscribers – I’m so glad you’re here. ❤ If you want to find out more about who I am and why I’ve been writing crypto newsletters for over 10 years, check out the “About” page. And feel free to drop into the Substack chat to say hi!

📽 “Press Publish” is back! Tomorrow at 3pm UK time / 10am ET, come join me and Izabella Kaminska, author of The Peg and The Blind Spot, about newslettering, writing, media, information overload and more. Details below. 📽

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

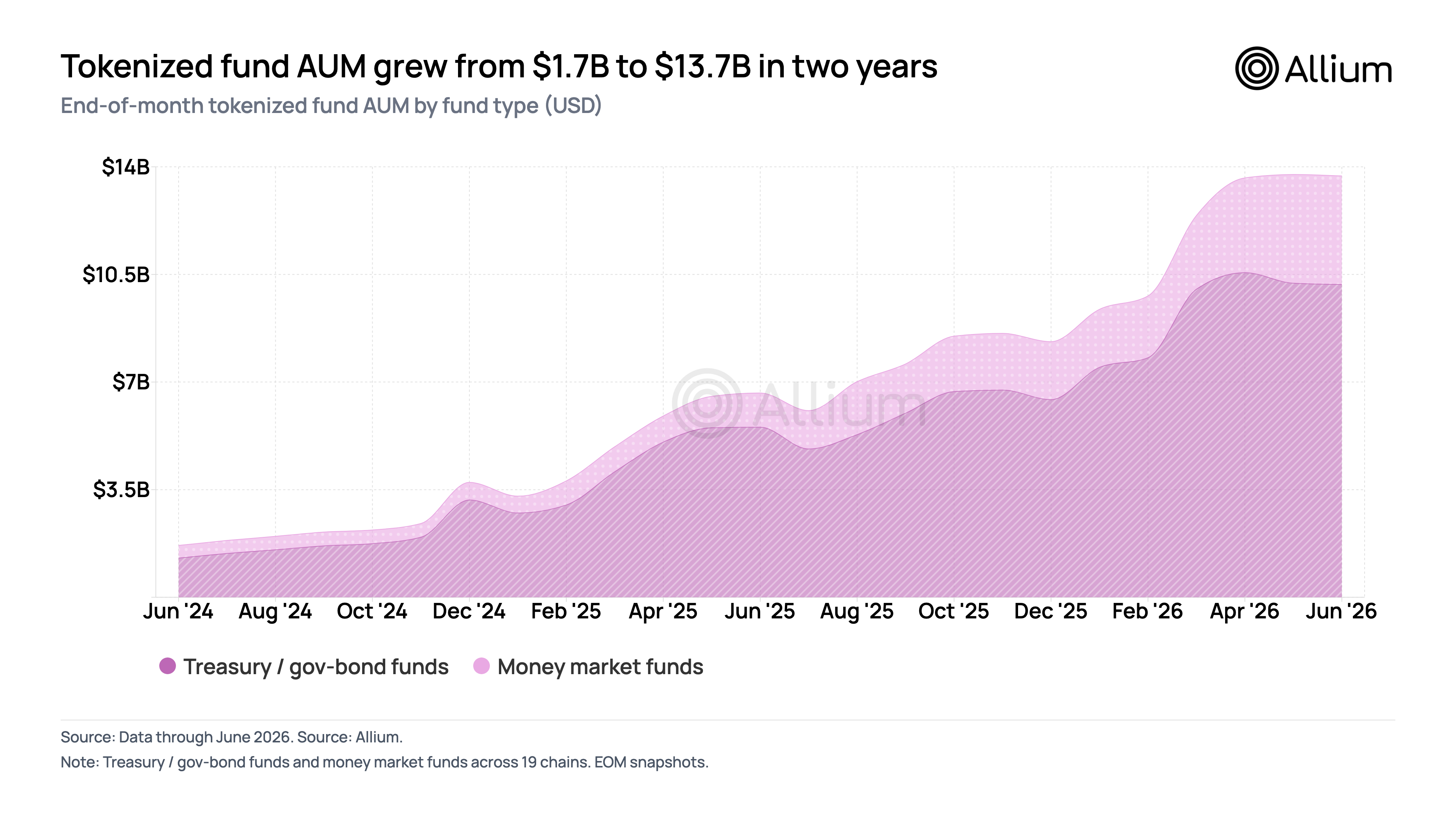

Tokenized US money-market and Treasury fund AUM reached $13.7B in June 2026, up roughly 8x in 24 months, with more than $4B added in the first half of this year alone. Four issuers hold 76% of the market – who are they, and on which chains are their funds concentrated?

To find out more, check out Allium’s data-driven look at where US money-market and US Treasury / government-bond funds live onchain in June 2026, covering issuers, funds, chains and the wallets that hold them.

→ Read the report: https://www.allium.so/reports/tokenized-us-funds-june-2026

IN THIS NEWSLETTER

The SEC, tokenization and structural change

A new era at the Fed

US rates: hawks fly

Term of the day: hawks vs doves

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you so much!! ❤

✨Press Publish with Izabella Kaminska✨

Come and join me and long-time journalist, finance expert and independent thinker Izabella Kaminska on Friday June 19th, at 3pm UK time/10am ET for a live chat about why and how she does what she does: how she manages to produce not one but two excellent newsletters (The Peg and The Blind Spot) while also writing for mainstream media, speaking at events, and juggling a ton of other stuff besides. We’ll touch on her long media career, where she thinks the industry is heading, how she handles the firehose of information, what works for her and what doesn’t, what advice she’d give her younger self, and more.

Again, Friday June 19th, at 3pm UK time/10am ET: https://open.substack.com/live-stream/239917

WHAT I’M WATCHING:

The SEC, tokenization and structural change

A recurring theme in this newsletter is how current securities laws aren’t appropriate for onchain markets. Written nearly a century ago for a narrow, paper-based financial system, they have evolved over the years to incorporate new technologies such as electronic trading and also new types of venues – but, even so, their basic assumptions often don’t hold when it comes to crypto assets and decentralized distribution.

I’ve also written before about how it seems like SEC Chair Paul Atkins is not only updating regulations to incorporate digital asset trading; he’s also using the development of onchain markets as an excuse to modernize both market structure and, even more difficult to change, the regulations that guide fairness.

One of these is Rule 611, also known as the “Order Protection Rule”. This stops anyone executing a stock trade for a client from doing so at prices that are worse than the best available on any national securities exchange. It does not, as many believe, require that client orders be routed to the best price – just that their trades are not executed at a worse price than those on official venues.

Last week, the SEC formally proposed the rescission of Rule 611, on the grounds that it has ended up:

fragmenting the market (by giving “best price” status to any trading centre that can meet or better the market level) – when Rule 611 was introduced, there were eight operating national securities exchanges; now there are around 17, not counting the more than 80 alternative platforms that also trade stocks and today account for roughly 50% of total volume.

diluting liquidity (by requiring brokers to sweep the whole market to execute a large trade, spreading execution across several exchanges to meet the best price rule – liquidity providers tend to post bids and offers on several exchanges at the same time).

adding complexity to an already complex market (as traders were incentivized to invest in increasingly sophisticated order routers, more connections, faster data feeds, constant monitoring, etc.)

But here’s another adverse side effect of Rule 611 – it blocks decentralized trading of tokenized securities.