WEEKLY: BRICS and markets, ECB threat

and an excellent spy series

Hi everyone, I hope you’re all doing well!

You’re reading the free weekly version of Crypto is Macro Now, where I reshare/update a couple of articles from the week.

If you’re not a premium subscriber, I hope you’ll consider becoming one! For the price of a couple of New York coffees a month, I can help you navigate the tangled web of macro impacts on crypto narratives, and crypto impacts on macro narratives.

You get ~daily commentary on macro, crypto and the space in between, plus some cool links, a smattering of charts, and a daily music link because why not. AND you get access to a premium subscriber chat over on substack.com or on the app! And audio!

Feel free to share this with friends and colleagues, and if you like this newsletter, do please hit the ❤ button at the bottom – I’m told it feeds the almighty algorithm.

In this newsletter:

BRICS: Why new networks matter for markets

The threat from the ECB

Some of the topics discussed the past couple of weeks*:

(*last week was patchy due to travel)

BTC’s emotional barrier

Stablecoin use: not just trading

EU DLT Pilot Regime gets moving

The loss of media trust: sad but inevitable

Why the neutral rate is climbing

Big bank blockchain networks

Can BRICS pull it off?

The weight of the election on BTC

The bigger threat from the ECB

Bonds are signalling a sentiment shift

Stripe’s stablecoin bet is bigger than it seems

Why isn’t tokenization scaling?

The ECB rebuttal

On the move

A pro-crypto Congress?

BRICS: Why new networks matter for markets

Geographical trading distribution

Kraken, Ink and the future of blockchain

Pennsylvania does it again

BRICS: Why new networks matter for markets

The fanfare and ceremony of the ongoing BRICS summit in Kazan, Russia, looks set to deliver more this year than the usual photoshoot and membership positioning.

There will be photos, and there will be membership positioning, but there are more obvious and also subtle messages being broadcast to the watching world.

The web of payments

One of the loudest is the proposal of a new BRICS payment system. This week, members adopted a joint declaration calling for the creation of an independent payment platform based on national currencies. This is not the same as creating a new currency – it is building new rails on which traditional currencies can move, much like SWIFT enables the transfer of funds between banks.

A proposal for a common token is circulating, which would be backed by gold and a basket of member currencies – but even Putin himself admitted last week that “the time has not yet come”.

Details of the proposed platform emerged a couple of weeks ago in the runup to the BRICS Finance Ministers’ meeting: among the possible solutions are a distributed ledger-based platform, as well as closer cooperation between central and commercial banks, and the increasing denomination of trade contracts in local currencies. Both Russia and China already have their internal alternative payments messaging platforms (SPFS and CIPS, respectively) which facilitate some internal and cross-border transactions, and which could in theory onboard a broader range of participants.

China has reportedly given the thumbs-up, India is apparently in favour, and Brazil has long been advocating for more local-currency trade, so it looks like the proposal will go ahead – it remains to be seen in what form, but a distributed ledger would both reduce costs and possibly mitigate future friction from additional sanctions, as payments could be more easily re-routed.

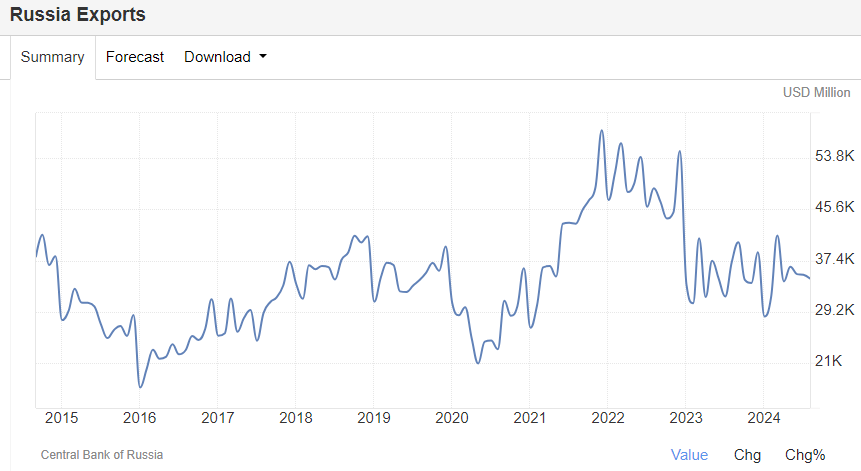

Obviously, the biggest beneficiary would be Russia as its banks have been hit by their exclusion from the global trading system following the invasion of Ukraine. This impacts other countries as well, as trade partners have had to find convoluted ways to pay for imports or receive payment for shipments to Russia. And there is plenty of trade going on – Russia’s exports have dropped from pre-invasion 2021 levels, but are roughly where they were in the three years leading up to the pandemic.

(chart via Trading Economics)

A SWIFT alternative has a strong appeal, not just for smoother cross-border payments, but also as “insurance” should weaponization of the dollar-based banking system accelerate in coming years – given mounting tensions between the US and Iran/China, this is certainly possible.

Sharpening the image

The other loud message lies in who showed up. The United States has been insisting that Putin is “isolated” and weak, and yet on Tuesday the world saw him welcoming leaders from around the globe. A total of 24 heads of state are in attendance, including that of NATO member Türkiye. Even the Secretary General of the United Nations, Antonio Guterres, showed up to pay respects, despite declining to participate in June’s Ukraine-led peace summit in Switzerland. This week, Putin does not look like the global pariah the West would like him to be.

What’s more, the BRICS summit gives reporters the chance to remind readers that BRICS nations account for 45% of the world’s population (the G7 only accounts for 10%), almost 40% of its industrial production, and 35% of global GDP (the G7 barely reaches 30%).

Plus, signs are the appeal of a non-Western trade alliance is growing: over 30 nations have applied to join as members, with another 10 expressing interest. The summit this week officially welcomed new members Iran, Egypt, Ethiopia and the United Arab Emirates – Saudi Arabia is hovering and deeply involved but has not yet officially joined, and Crown Prince Mohammed bin Salman is not in attendance.

Apparently, the group will not be admitting new members next year. However, it has extended a “partnership” invitation to 12 countries: Algeria, Belarus, Bolivia, Cuba, Indonesia, Kazakhstan, Malaysia, Nigeria, Thailand, Türkiye, Uganda, Uzbekistan, and Vietnam. As far as I know, we don’t yet have details on what “partnership” means.

Meanwhile, the summit has given the India-China relationship a boost, as border hostilities are walked back and the leaders hold their first bilateral meeting in five years. Hostility between the two countries has been one of the key barriers to further economic and financial integration between group members – the thaw not only signals bloc power, it could also accelerate broader cooperation.

Coincidentally, this week also saw the first Commonwealth Summit led by the new UK prime minister Keir Starmer – only, leaders of key members chose to attend the BRICS meeting instead.

Against a backdrop of political chaos in the US and weakening UK influence, the BRICS summit is sending an image of relative coordination and expansion.

Why does this matter?

Directly, and short-term, the impact on markets will be subtle. Longer-term, it will be significant.

For now, the dollar will continue to dominate world trade. According to Brookings, the US currency accounts for just over half of cross-border trade invoices, and almost 60% of international payments. But this figure probably does not include the transactions that do not go through SWIFT – this is a small portion of global payments, but we can assume it’s growing.

(chart via Brookings)

We can also assume it will continue to grow, especially once the new BRICS payments network goes live. At the end of 2023, already 20% of global oil trade was settled in currencies other than the dollar – since the BRICS bloc (if we include Saudi Arabia) accounts for almost half of global oil output, this will almost certainly increase.

If so, Bitcoin’s narrative as a hedge against dollar debasement will strengthen, as weakening global demand for dollar-based trade, at a time of increasing supply, should pull USD down in relative terms. The dollar will no doubt continue to be the world’s reserve currency as there is not yet a viable alternative, not even close. But supply relative to demand matters, and even small shifts can influence sentiment and valuation.

Crypto assets themselves are unlikely to form part of any new BRICS currency initiative, with the exception of stablecoins – these are already in use for trade settlement in Russia, and the obvious convenience is likely to swell volumes even further while incentivizing the expansion of blockchain use.

Bigger picture, BRICS is important to keep an eye on for what its growth and increasing sophistication say about the strong currents of change. These always lead to uncertainty which boosts demand for “hedges”, even before any potential impact from US retaliation. Trump has threatened 100% tariffs on any nation pulling away from the US dollar – but the economic and geopolitical cost of such a move would be colossal. Plus, the more the dollar is weaponized, the greater the incentive to build an alternative system.

In sum, this week was significant in terms of global realignment. We don’t yet know the speed or magnitude of the impact on markets and currencies, but they tend to follow trade which follows alliances. The BRICS organization is not playing around.

The threat from the ECB

Last week, two European Central Bank executives from the Market Infrastructure & Payments division published a paper on Bitcoin’s detrimental impact on the overall economy. It was blatantly biased with distorted interpretations, factually incorrect in too many places to count, and poorly constructed in that alternative arguments were not even considered. Unsurprisingly, hilarity ensued. This may be misplaced, though. What we have here is something deeply sinister.

For context, this is not the analysts’ first attempt at quelching Bitcoin interest. Back in 2022 (with BTC under $20,000), they published an analysis insisting that Bitcoin was on the “road to irrelevance”.

Now, their point is more that BTC could continue to appreciate in price and that’s bad.

The reason it’s bad is that BTC will be more expensive to acquire for latecomers, which impacts their spending power elsewhere. Essentially, the gains that have accrued to early Bitcoin participants suck value away from the economy by making BTC cost more for those buying now.

Of course, this is how asset markets work, but the point the authors make is that Bitcoin doesn’t do anything, therefore its price gains are unproductive and unjustified.

“Since Bitcoin does not increase the productive potential of the economy, … the wealth effects on consumption of early Bitcoin holders can only come at the expense of consumption of the rest of society.”

A bewildering argument, yes, but a more worrying implication is the belief that only certain types of “productive” investment should be allowed. The authors have no objection to gold, though, perhaps because it looks pretty in jewellery.

There is no contemplation of how the Bitcoin network could facilitate payments in parts of the world without sophisticated financial systems, or of the value of a seizure-resistant hedge in a fragmenting global landscape. There is also no mention of the data storage benefits of decentralized networks nor the cross-border cost benefits of blockchain-based transfers. This could be because the authors have not actually researched the Bitcoin network. Or, it could be because non-speculative use cases don’t suit their narrative.

I suspect the latter, because the language used is not exactly pulling punches.

“… the consequences of the Bitcoin-as-an-investment vision with perpetually increasing Bitcoin prices imply a corresponding impoverishment of the rest of society, endangering cohesion, stability and ultimately democracy.”

Yes, Bitcoin is apparently a threat to democracy.

Here the document starts to wade into murky territory. It gets political.

Arguably, the ECB can be excused for energetically defending democracy. But the paper at times reads like a political pamphlet, blaming society’s ills on a “common enemy” by essentially saying that Bitcoin is responsible for the widening inequality gap.

The text suggests that early gains are unfair (scapegoating) and dangerous to society (fearmongering), without any evidence or alternative consideration for either. This would be disconcerting language from an extremist political group. But it’s from Europe’s central bank, a supposedly apolitical organization.

The authors even advocate for a specific type of political agitation:

“In any case current non-holders should realise that they have compelling reasons to oppose Bitcoin and advocate for legislation against it, aiming to prevent Bitcoin prices from rising or to see Bitcoin disappear altogether.”

And the stakes are high:

“Failing to do so could skew election results in favour of politicians who advocate pro-Bitcoin policies, implying wealth redistribution and fuelling the division of society.”

Again, the ECB is supposed to be apolitical, and yet here are two of its representatives advocating for political action against a piece of open-source code that ensures decentralized transfer. Hilarious, yes. But also freakishly sinister, when you consider not just what they are trying to do, not just why, but the fact that they obviously feel empowered to do so.

It’s worth pointing out that the paper was not published on the ECB website, but on SSRN, where papers can be uploaded without review. So we can’t be totally sure this is an ECB-endorsed publication.

Yet whether the ECB supported this work or not, the fact that it was published under ECB bylines ties the central bank to the authors’ views, no matter how many disclaimers are thrown at it. It could be a “trial balloon” to gauge reception to the idea, or it could be on SSRN while ECB editors proof-read as a preliminary step towards ominous publication on the official ECB blog.

If, indeed, this paper is a precursor to aggressive action against Bitcoin from the European Central Bank, we can take comfort from one fundamental characteristic of the network: the more authorities try to stamp it out, the more obvious its use case.

And, bigger picture, I hope we start to ask more questions about just how far the ECB’s mission creep should be allowed to go.

PS: A group of Bitcoin thinkers (Murray Rudd, Allen Farrington, Freddie New, and Dennis Porter) co-authored a blistering and yet elegant and academic takedown of the above-mentioned paper. A cathartic read that also educates on the technical, social and philosophical aspects of Bitcoin, as well as on its evolution, both past and future.

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

This past week I finished watching the fourth season of Slow Horses. I’m a big fan of the spy genre, my first John le Carré blew my mind (spies can be like real people??), and so it’s not a surprise that I loved the series’ shabby and chaotic world of intelligence gathering. It’s smart and manic with great acting and a strong script, and I think the fourth was the best season yet.

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade.