WEEKLY – DeFi drama, media and first impressions

Plus: assorted links, music nostalgia and more

Hello everyone! I hope you’re enjoying a glorious weekend wherever you are. Get away from screens if you can, they’re noisy.

Yesterday, I had a wonderful chat with Irina Slav on newslettering – you can see the playback here. 📽 “Press Publish” will be taking a break next Friday as it’s a holiday where I live, but you can see previous sessions here. 😊

Earlier this week, I was invited onto Scott Melker’s show The Wolf of All Streets where we talked about macro and bitcoin narratives as well as just how crazy things are. You can watch that playback here. 📽

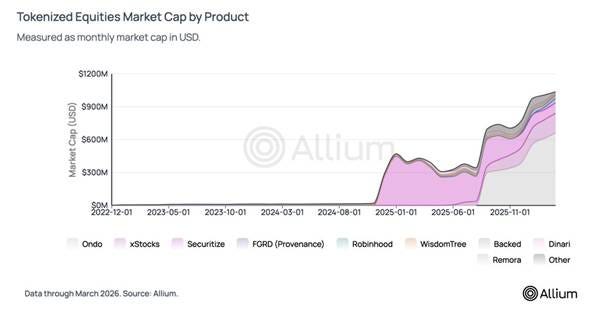

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

In this newsletter:

Crypto, media and first impressions

DeFi disruption

Assorted links: State indoctrination, reading, climate change indifference, essential cinema, QR codes and narrative fallacies

Weekend: an iconic music video from the ‘80s, who do you recognize?

Crypto is Macro Now offers ~daily commentary and updates on the growing overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

Some of the topics discussed in this week’s premium dailies:

Coming up this week: PMIs, retail sales and Warsh’s confirmation hearing

Monday mood: crypto, media and first impressions

Term of the day: Swap lines

Market: fooled again?

US Treasuries: how safe is safe?

Term of the day: Auction tail

Tokenization: Building frustration

Markets: ok, now what?

Term of the day: Helium

Macro: misleading US consumption

DeFi disruption

Term of the day: DAO

Markets: a bewildering disconnect

Energy markets: a different world

Crypto, media and first impressions

Like many of you, I often wonder why smart economists and other academics insist crypto is exclusively for speculation and crime.

Last weekend, I listened to a Macro Musings podcast in which two storied and insightful economists discussed dollar dominance and how that could play out in coming years. (TLDR; slow erosion, potentially accelerated by poor policy decisions.)

One of them had some intriguing things to say about stablecoins and how expectations of high demand would most likely be disappointed; the other dismissed them as a conduit to the crypto market, which is about “criminality, money laundering”.

Regular readers will know by now that what people think about crypto markets is much less interesting to me than why they think it. I’m fascinated by intellectual biases and instinctive blocks, as well as what it would take to break through them.

When I hear highly intelligent people outright reject crypto, I’ve tended to assume that many – especially those in traditional finance – are afraid of a systemic change to the system that pays them, and that the economist profession (and academia more broadly) tends to encourage “safe” views. In other words, many have implicit incentives to not dig deeper into what can often be a distasteful sector.

But after chatting to experienced journalist Brady Dale about media and crypto (you can see the playback here), something else clicked: it’s not just the traditional finance culture that puts up cognitive walls. It’s also mainstream media, which has a stronger inherent and subliminal bias than it would like us to believe.

First, we have to remember that modern media business models depend on clicks for their ad revenue. And that shock and gossip get many, many more clicks than warm stories about people being lifted out of poverty, dissidents being able to transact after debanking, refugees fleeing with their savings on a pendrive, and so on.

So, mainstream headlines about crypto tend to focus on scams and scandals. Back in 2022-23, when people I’d meet people at social occasions found out I worked in crypto, they always only wanted to hear more about Sam Bankman-Fried. Today, many of my media interviews include at least one question about the unfortunately obvious grift.

Every now and then we do see solid reporting from mainstream outlets on how Bitcoin mining supports a wildlife park, finances the construction of power grids in remote locations, or helps a small nation harness its natural resources to boost its Treasury. But, while good journalism is supposed to dig deeper and uncover overlooked narratives, we all know that those stories don’t “perform” as well as the more salacious tales.

Oh, and there’s the price headlines highlighting moves to the upside (often with the tone “gamblers are doing quite well this week”) or downside (with a whiff of vindication).

It’s understandable, then, that the impression most mainstream observers have is that of scandal and speculation.

But the issue goes much deeper than the quest for clicks. Even among subscription sources, coverage is usually limited. After all, media has strong incentives to NOT write about the disruption of the system that maintains it. Individual cases of manipulation are fair (and profitable) game; but highlighting the corrupting creep of centralization and the widening gulf in inequality perpetuated by market structures could upset advertisers as well as readers. This goes a long way towards explaining the consistently snide crypto content from the Financial Times and others (although I do think Bloomberg does a good job).

There’s more. In our chat, Brady made the interesting and overlooked point that most of mainstream media is left-leaning. Most of the crypto industry isn’t. Of course, crypto has plenty of left-leaning advocates who eloquently highlight the need for a systemic re-think of financial rails. But the libertarian origins and the “hands off my money” ethos of the early crypto culture gave the sector a right-leaning tint that many journalists instinctively react to. Or if not the journalists, their editors.

And corporate policy has an impact. Most media organizations will have rules about journalists holding assets that they write about. Some outright forbid it in order to avoid bias – but that only creates a different kind of bias, one born of a lack of familiarity. Others insist writers disclose any crypto holdings, effectively putting a target on their back, inviting reputational harm (“biased!”) or worse. And those brave souls who choose to write something positive about crypto are most likely going to be accused of “pumping their bags” even if they don’t have any. It’s much safer to not write anything good about crypto, ever.

So, mainstream media has a stack of inbuilt incentives to focus on the seamy side of crypto. This is unfortunately relevant as most traditional finance types rely on mainstream media for their information about what’s new and what’s going on in the world. First impressions matter, and when it comes to the crypto industry, they’re usually not good.

Can this be changed? Well, media is changing. Slowly, but inevitably. And that will change the ingrained barriers. Crypto is becoming part of mainstream finance. When prices start climbing, all those who insist it’s going to zero will retreat into embarrassed silence. The energy consumption freak-outs have gone quiet. Also, more and more smart people are writing about the nuances, pointing out that – like all new technologies – crypto has both good and bad uses.

With time, media and education incentives will evolve.

Until then, however, people will continue to learn about crypto via headlines that are much more likely to focus on the cringe than on the opportunity. So, uninformed rejection is not surprising, and we should give some grace to those who have not yet invested the time in understanding the complexity. After all, most are busy people with so much to keep on top of. Sure, they could refrain from publicly opining on things they haven’t done much research on – but who among us does that these days?

Old media may have its incentive problems, but new media does too: opinions, even superficial ones, are the new currency.

✨ If you find this newsletter interesting or useful, would you mind sharing with friends and colleagues and nudging them to subscribe? I’d appreciate it! ✨

DeFi disruption

Hacks and other exploits are distressingly common in the crypto ecosystem, unsurprising given its basis in code and the genius of online manipulators. The hubris-fuelled confidence of the sector’s early days has fortunately faded (I remember being yelled at for questioning the Ethereum DAO back in the day) as by now we all know that complexity always has weak points. But the scramble for profit still incentivizes us to downplay the potential impact of any risk.

I rarely cover examples of losses from crime in this newsletter as they have come to feel more like background noise than foreground impact, but this past week gave us an unfortunate exception. On Saturday, Kelp DAO suffered an exploit that triggered significant contagion and uncomfortable controversy.

Much like how 2016’s Ethereum DAO drama led to a decentralized network taking a centralized decision to roll back supposedly immutable transactions, the Kelp DAO incident shines a harsh spotlight on decentralization and questions whether it can ever become a pillar of modern finance. A big difference between then and now is the sheer size of today’s DeFi market, and the participation or at least peripheral interest from large, sometimes seriously large, institutions.

Some scene-setting: Kelp DAO is a liquid restaking protocol built on Ethereum that takes users’ ETH, stakes it so they can earn part of the reward, and issues them another token backed by that ETH (rsETH) that can then be used in other DeFi apps on other blockchains to earn more yield.

Saturday’s exploit led to the theft of roughly 116,500 rsETH, worth about $290 million at the time, making it the largest crypto hack so far this year. The tokens were then deposited as collateral on decentralized lending platforms (mainly on the largest, Aave) to borrow significant amounts of ETH and related tokens, creating a mountain of bad debt. These borrowed tokens were then deployed across the ecosystem.

(I’m glossing over a lot of the details to avoid getting into deep cryptographic weeds that are extremely relevant for DeFi structures but ultimately not so much for the bigger picture.)

Within hours, Aave had frozen rsETH markets on the platform to contain the damage, but users started withdrawing loans for fear of liquidity issues. Since the exploit, the lending platform has lost over $10 billion of Total Value Locked (the amount held in the application’s smart contracts), a drop of more than 40%.

The drama escalated when Arbitrum’s Security Council took the decision to freeze roughly $71 million in related ETH (stolen tokens, or those borrowed using stolen collateral) on the Ethereum layer-2 chain.

The Aave freeze impacted specific contracts on the platform and fit within its responsibility to protect collateral. Fair enough, the right thing to do. The chain-wide Arbitrum freeze, on the other hand, opened up a whole new box of controversy.

Just how decentralized are blockchains when they can do that? Should a small group of people be able to override onchain finality? What does “immutable” mean when that becomes accepted? Then again, pushing back against crime is good, right?

The precedent is worrying on another level as well. In future hacks, will applications and blockchains be criticized or perhaps even held liable if they don’t immediately freeze involved funds? How long before the fear of repercussions makes token freezes and transaction rewinds a frequent occurrence? Just how “trusted” will onchain transactions be then?

Some have said this could herald the end of the tokenization push.

On the one hand, I get it. One of the main advantages of putting assets and money onchain is the interoperability, the ability to connect with each other and with smart contracts across the ecosystem. Without this kind of “modularity”, tokenization gets relegated to traditional finance on new rails. Put differently, if onchain assets can’t move freely and slot seamlessly into combinations and applications, tokenization becomes no more than an expensive database upgrade.

But, for most of the ongoing tokenization work, free movement is not on the table anyway. Most initiatives supported by traditional finance institutions – issuers, marketplaces, intermediaries – is happening on permissioned chains. It’s more about transaction efficiency and lowering the cost of issuance, not at all about freedom of movement, flexibility, disintermediation and open access.

This taps into a long-standing debate that has been attracting more heat recently: whether we should be building tomorrow’s financial system on public or private rails. There are valid arguments on each side. Personally, I don’t see why the argument has taken a black-or-white hue when the result will inevitably be shades of grey: tokenization will inevitably happen mainly on permissioned blockchains with some public blockchain characteristics, because neither institutions nor regulators will accept pure decentralization. That’s not how I think it should be – I’m totally behind the liberating and equalizing potential of public blockchains. But unrealistic idealism can hinder progress.

After all, traditional finance is married to the legal system and both need a specific entity to be responsible for errors. In decentralized finance, assigning responsibility is complex.

This debate ties into the class action suit against Circle, which chose to not freeze USDC that had clearly been stolen in the recent Drift exploit. Circle insists it can’t intervene without a court order or law enforcement request. To what extent should it be held responsible for preventing crime, and to what extent should it be held liable for not stopping it when it could have?

Taken together, the fallout from the Kelp DAO and the Drift incidents paint a picture of divided ideologies, and build on doubts whether the two can co-exist. Can we have a large financial market running on decentralized principles? Or do investors need the reassurance of some sort of protection before deploying capital? Do market infrastructure providers need liability limitations before providing much needed services and liquidity? Where should the boundaries between smooth connectivity and contagion risk be drawn? I’m sure some wise person somewhere said something along the lines of “freedom is great, until you are scared”.

These debates need to be had, and the risks of both centralized and decentralized approaches need to be examined. Unfortunately, the result will probably disappoint decentralization advocates. But they will hopefully continue to have niche markets in which to experiment, test new structures, and show centralized infrastructure that boundaries can be shifted.

See also:

ASSORTED LINKS

(A selection of reads I came across this week that I think are worth sharing, not always about crypto or macro. I try to choose links without a paywall, but when I feel it’s worth making an exception, I specify.)

Nicholas Carr writes about the fine line between information and indoctrination, what modern communication is for, what we should give up for the sake of security, and many more issues that are so much more fundamental to our society and our freedom than most realize. (Operation Gaslight, The New Atlantis)

An uplifting reminder of how important it is to schedule time to read, and some notes on how to get the most out of it. Personally, I find a half hour of morning reading – more if I manage to wake up early – goes a long way towards quietening the noise of the day’s news flow. (On depth and lightness, A Reading Life)

Quico Toro on why the climate change crisis prevention movement was doomed from the start, but especially now. (The year we stopped talking about climate, One Percent Brighter)

From last year but a new discovery for me, one that gives the clearest answer I’ve seen to a question that has long been on my mind: how do QR codes work? (How The Heck Do QR Codes Work?, PerThirtySix)

Gurwinder on the biological and technological origins of narrative fallacy, and on how a glut of information doesn’t make us better informed, it makes us more susceptible to illusions. (The Electronic Starfield, The Prism)

“The brain evolved for a low-information world, and is overloaded in a high-information one. Like someone with dark-adapted eyes suddenly switching on the lights, we’ve become dazzled by overillumination. And the online world has pivoted to exploit it.”

In one of my earlier Assorted Links this month, I featured an epoch-spanning reading list curated by Ted Gioia of The Honest Broker. Kyle Worley took it upon himself to curate one for cinema, pairing his choices with Gioia’s recommended books. How many of these have you seen? (A Cinema Supplement to Gioia’s Humanities Program, Sacred Slang)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

This video popped into my head earlier this week – a recording of “We Are The World”, written by Michael Jackson and Lionel Richie, and sung by… well, just about everybody who was anybody in the 1980s’ music scene. How many faces can you put a name to?

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.