WEEKLY, Oct 29, 2022

Hi everyone! You’re reading the weekly Crypto is Macro Now newsletter, where I look at the crypto market and its growing overlap with the macro landscape. I’m Noelle, and I’ve been writing crypto-focused newsletters for over six years now, first for CoinDesk and more recently for Genesis Trading. Now that I’m concentrating on independent research (the theme is in the title), it felt natural to continue. If you find this useful, please consider sharing with friends and colleagues.

If you’d like to receive a premium daily email with more detailed market and news commentary and are not already a subscriber, hit the signup button below. Some of the topics covered in the daily email this week:

The drivers of the crypto rally

Mixed signals from the Fed

Divergent asset group narratives

Weird volatility metrics in traditional markets

US economic data starting to show consumer weakness

ETH vs BTC open interest

Bitcoin miner exhaustion

MARKETS

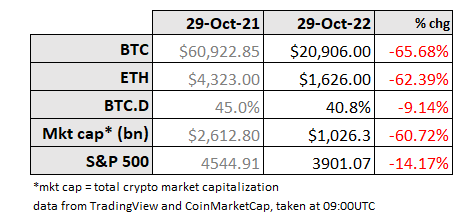

Could it be that the “uptober” myth is actually true? The first month of the last quarter is typically strong for BTC – six of the past seven Octobers have delivered positive returns, more than any other calendar month. Its post-2015 average for October (not counting this month) is 24% according to data from bitcoinmonthlyreturn.com, higher than any other month. BTC would need to blow past $24k before next Tuesday to avoid lowering the average, and there are still three days left in which things can radically change – but it’s looking good, and even if BTC drops from here, we can confidently say that October’s lead is safely in the bag.

As the table at the top of this section shows, ETH has easily outperformed BTC (almost 25% in one week!). This is not surprising, as ETH’s higher volatility means it usually does better on the way up and worse on the way down. What is surprising is the sharp drop in bitcoin’s dominance. A downtrend in this metric was expected as markets recover, since investors tend to rotate into the relatively “safe” crypto asset in times of uncertainty and rotate out when they want extra volatility – but this sharp a drop is unusual, and could be a reflection of the pent-up demand for performance.

(chart via TradingView)

It is also good to see the crypto market capitalization above $1 trillion again, for the first time since late September. This itself could attract more investor attention as, well, size matters, especially when it comes to institutional interest.

And speaking of institutional interest…

Essay

The “Option” of Crypto Regulation

Go around the room at any highbrow crypto gathering and ask what the suited participants are most excited about, and the answer you’ll most likely hear is “regulatory clarity”. They’re not wrong – it would indeed be a boon to the industry as it would give builders and investors a certain amount of protection and usher in even more institutional funds. But it’s not the “make or break” for crypto that it’s painted to be. And those that insist that “all of crypto must be regulated” display a lack of understanding of what crypto is and how it got to where it is today.

Not all crypto markets will end up regulated. But nor do they need to be for the industry to succeed. I’ll go even further – nor should they be.

As a crypto analyst with an institutional bias, I am inherently pro-regulation. Despite my slightly libertarian leanings, I support the role of government in protecting citizens. And I recognize that many investors are more comfortable with some degree of protection when it comes to financial transactions.

This week, Bloomberg published the results of a recent MLIV survey, in which 60% of 564 respondents agree that more regulation would make them more likely to invest in crypto assets. Also this week, CoinDesk reported on a poll conducted by the Crypto Council for Innovation which showed that 52% of the 1,200 participants (of whom only 13% own cryptocurrency) want the industry to be more regulated. And on Thursday, Fidelity Digital Assets published their annual survey of global institutional investors which cited regulatory issues as one of the top barriers to investment.

So, the numbers suggest that investors are awaiting more regulation with open arms. This is supported by the hopeful narrative that more regulation will bring in more institutional funds, which will boost prices.

But let’s look a bit closer before we take a big step back.

The numbers published in this week’s three surveys are not conclusive. For 40% of Bloomberg’s respondents, the degree of regulation will have little impact in their crypto investment decision. For the Crypto Council for Innovation poll, almost half either don’t want the industry to be more regulated or are indifferent. And the Fidelity Digital Assets survey shows that concern about the classification of certain assets came in seventh in the list of investment barriers, while a “lack of regulatory clarity” came toward the bottom. Only 4% of Asian institutions and less than 20% of European respondents cited this as something they worried about.

So, regulatory issues are a concern for many, but not for all. And here we come to the bigger issue: the idea that all crypto markets can be or even need to be regulated.

This stems from the institutional mindset. Most institutions can only transact on regulated exchanges, and all institutions want to avoid future legal issues. What’s more, most crypto market firms want institutional clients, for the transaction volumes and willingness to pay for services. So, crypto regulation is verging on an obsession amongst service providers and a meaningful chunk of investors.

But it’s not an obsession for the whole industry, and to assume that this is the natural state of affairs is to overlook a key feature of both crypto and regulation: they are about choice.

Crypto is obviously so – it emerged as an alternative to the centralized fiat system, and the explosion of innovation, technological progress and incentive experimentation over the past few years has spun off a dizzying array of assets, use cases, governance styles, trading platforms, tribes, even aesthetics.

The role of choice in regulation is not so obvious. We’re taught that we have to obey the rules, but this isn’t true. We can ignore them (please note that I am NOT recommending this!), but there is a price. Sometimes the cost is high (e.g. men with guns will lock you up for a very long time), sometimes not so much (your bank will make sure you pay the assigned penalty). We evaluate the trade-off – and for most, there are moral and social costs as well – and we act accordingly. But the choice is ultimately ours.

In exchange for obeying the rules, we get protection. This is usually a very good thing. But when it comes to financial transactions, for some that protection can feel like centralized control, especially when opportunities are denied based on seemingly arbitrary filters, and individual agency involving one’s own wealth is curtailed because of the threat posed by distant others. For many participants, however, that protection implies fair pricing, recourse if anything goes wrong and the civic comfort that illicit transfers are more easily flagged.

This brings us to the contradiction inherent in the institutionalization of crypto, one that is forging a stronger industry but that is currently suffering from both a myopic focus and a blurred narrative. Crypto markets originally developed at the grass roots level, with no regulatory oversight or protection whatsoever. As the investor base broadened and as certain blow-ups highlighted the often-painful lack of rules, the demand for more reliable platforms led to the birth of the market infrastructure we have today. This in turn fuelled the growth of investor interest, including that of more restricted participants with deep pockets, and the boost in volumes supported both prices and further innovation.

Institutional investor involvement in crypto markets is good. It is a sign of success. But the outsized weight of its influence has led to the conflation of “crypto potential” with “institutional needs”. This makes it easy for us to forget that crypto emerged retail-first, which in turn tends to hone focus on fitting a square peg into a round hole as regulators insist that current rules can cover our industry. This is a generalization, sure, but one that is delaying support for certain areas of progress as infrastructure participants wait for a regulatory clarity that is unlikely to ever get ahead of or even keep up with crypto innovation and demand.

Crypto applications will continue to emerge on the fringes, and there is not much anyone can do to stop this as token issuance and trading is not controlled by any central authority.

And not all of crypto needs “regulatory clarity” or institutional participation. Much of it simply needs testing with real users and real incentives with some degree of supervision to ensure fair markets and mitigate illicit use. More regulatory sandboxes, for example, could further industry experience while deepening official understanding of the risks and opportunities. And there are no doubt other frameworks that could give officials some assurance that crime is not abetted and that participants understand the choices they are making. Fewer rules means more opportunity but less protection. Waiting for a detailed framework or even specific limitations could imply greater safety but more delay.

In sum, regulators could give crypto industry builders and market participants more choice in the rules they follow while showing support for good faith human ingenuity and respect for those it helps. And in so doing, they could perhaps strengthen the appreciation for what regulation has to offer.

KEEP AN EYE ON:

(Three main themes from the week, explored in more detail in the daily emails.)

Rally drivers. Tuesday’s market rally, in which BTC and ETH finally broke out of their slumber and rose 7% and 14% respectively over 24 hours, triggered the largest short liquidation event since July of last year (which back then marked the beginning of the run-up from ~$30k to ~$67k). It remains to be seen whether the week’s moves are enough to awaken the momentum traders, but it does feel like something has changed. In part, the “coiled spring” metaphor I’ve sprinkled around could finally be releasing (it has to happen at some stage). And in part, narrative and on-chain fundamentals have been pointing to a crypto sentiment shift:

A realignment of BTC correlations, with that to gold surpassing that to stocks on a 30-day basis.

(chart via Coin Metrics)

Continuing accumulation, with the amount of BTC that has not moved in over a year reaching a record of over 66% this week.

An easing of rate hike expectations. The US 10-year yield dropped sharply when the US Q3 GDP data came out on Thursday, extending the week’s downward trend to as low as 3.90%, while CME indicators shifted to a 13% probability of only a 50bp hike on November 2, vs a 0% probability just a few days ago. December’s odds are also swinging in favour of moderation, with the probability of two 75bps hikes in a row now down to 40% from more than 75% just over a week ago, and that of two 50bps hikes up to 8%.

(for more market indicators with lots of cool charts, see the daily emails from Wednesday and Friday)

Crypto market expansion. As Hong Kong kicks off its Fintech Week on Monday, it is expected to announce measures to recover some of its recent crypto exodus, including legalizing retail trading for licensed platforms. This would be a marked change from the current system, which for the past few years has allowed centralized exchanges to only serve professional investors.

The potential impact on volumes is significant – Hong Kong was for many years a key crypto centre, serving the vast Chinese market which accounted for the majority of crypto trading up until its official ban by the Communist Party in September 2021 (it had been banned well before that, but somewhat half-heartedly). This is worth keeping a close eye on for how it navigates the proximity to Chinese markets, and whether it is a harbinger of change to come in China or an exception that will need resilience to survive. While Chinese strategy can be inscrutable, especially given this week’s shift in the political winds within the Communist Party, this is very encouraging – even the slightest hint that the Chinese market could be “back” should be enough to get market participants scrambling.

(see also Arthur Hayes’ “Comeback” essay about the impact of the Chinese market and how it seems to be ramping up again – I mention this again further down in the Good Reads/Listens section)

Bitcoin use cases. There seems to have been a flurry this month of development activity on Bitcoin’s Lightning Network, a layer-2 solution that enables fast, inexpensive transactions with greater smart contract flexibility, while benefitting from Bitcoin’s security. Just this past week:

Stone Ridge Holdings, an asset manager with over $10 billion AUM and owner of NYDIG, announced the launch of a startup accelerator focused on the Bitcoin Lightning network.

Crypto developer Kollider‘s derivatives exchange based on Lightning went live.

Cash App announced that its 40+ million users can now send and receive instant bitcoin payments via the Lightning Network.

Synota, a startup that wants to bring energy payments to Lightning, raised $3 million in a seed round.

These are not massive initiatives for now, but they are significant in that they represent the continuing evolution of the Bitcoin ecosystem and the likelihood that new use cases will emerge, further diversifying adoption and the user base.

For a more detailed daily dive into trends that matter as well as market commentary, please consider subscribing to the premium daily email.

A YEAR AGO:

(This section looks back at what was going on this time last year, so we can see how far we’ve come and how far we haven’t.)

Regulation: It may seem like the industry has made fast progress with influencers on the Hill, but looking back a year, we see that although debates may be tilting in a different direction now, the uncertainty has made little progress:

On October 26, 2021, just as the new OCC chief Michael Hsu was wrestling with the legacy of his predecessor Brian Brooks (who issued a statement authorizing banks to hold crypto), FDIC chair Jelena McWilliams said publicly that banks needed to be allowed to get involved with crypto in order to prevent the industry from growing outside the regulated sphere.

Biden’s nominee for head of the CFTC, Rostin Behnam, made a pitch in his confirmation hearing on October 27, 2021, for the CFTC to become the primary “crypto cop”. A year later, his position confirmed, he is still making the same pitch.

Meanwhile, a Bloomberg article reported that the SEC was angling to get more authority over stablecoins.

NFT heyday: For a dose of trippy nostalgia, on October 29, 2021 a crowned Bored Ape sold for $2.7 million, to date the third largest transaction in NFT history.

GOOD READS/LISTENS

An epic and highly enjoyable description of crypto and its ecosystem, from Bloomberg’s Matt Levine, who has a dispassionate yet interested approach that lays bare what is important and veers into the unimportant only when it is truly interesting. As Matt himself acknowledges:

“I write about crypto as a person who enjoys human ingenuity and human folly and who finds a lot of both in crypto… My goal is to convince you that crypto is interesting, that it has found some new things to say about some old problems, and that even when those things are wrong, they’re wrong in illuminating ways.”

Eric Voorhees’ powerful response to Sam Bankman-Fried’s proposed crypto regulation framework is in part supportive but highlights some pitfalls, and contains an exquisite rant against the SEC. This debate is a fascinating and welcome step forward in questioning the ideal role of regulation.

Arthur Hayes points out how significant China has been in the development of crypto markets, and how it seems to be getting ready to ramp up again.

Podcast: Money Talks, from The Economist, interviews Gary Gensler about crypto, the Treasury market and who Satoshi is (an unusual look at the playful side of the head of the SEC).

Podcast: BTC101 – Preston Pysh talks to Luke Gromen about the inevitability of monetary easing, the weaponization of energy, the evolving role of central banks, and a whole lot more.

Have a Good Weekend!

We tend to anthropomorphize animals – and I’m as guilty of this as anyone, no apologies – because we want them to be relatable in a simple, honest way, in contrast to many of our human connections. To be honest, I’m not interested in the biology behind animals’ facial expressions, or even whether our inferences are accurate (I know they’re usually not). What I value is the feeling of emotional kinship that comes from recognition, and if that means I appreciate nature even more, then all for the better. Have you ever tried sticking googly eyes on a mushroom? It triggers feelings, try it.

(image via Comedy Wildlife Photo)

All this is a preamble to try to explain why I look forward every year to the Comedy Wildlife Photography Awards, and this year’s was released last week. Beyond the huge respect due to the hours of work and strokes of luck necessary to capture these captivating images, I challenge you to look at these wildlife photos without chuckling or at the very least smiling.

(image via Comedy Wildlife Photo)

Totally agree with you as well

I’m just wondering if Crypto will have a lower leg from here along with equities and real estate crash — what do you think?

Just want to save dry powder for better final entries before the turning in Global Liquidity— which might have already started with Japan (and China?)

Yes we have rallied off the lows along with S&P etc

What will happen to us in the deflationary bust that follows this (temporary) melt up ??

Interested in your thoughts on this roller coaster-- not sure Fed will be pivot friendly at all next week into Midterms ...