WEEKLY, Sept 14, 2024

gold, rates, Russia and BTC

Hi everyone, I hope you’re all well! It sure feels like it has been an eventful week, what with the debate, CPI, SEC flip-flops and gold’s surge.

Below, I look at the latter, as well as what could be behind the sharp change in US rate cut expectations for next week. I also share something I’m happy to see my tax euros contribute to, for the moments of genuine (not mocking! ok maybe a bit) mirth.

You’re reading the free weekly version of Crypto is Macro Now, where I reshare/update a couple of articles from the week.

If you’re not a premium subscriber, I hope you’ll consider becoming one!

Feel free to share this with friends and family, and if you like this newsletter, do please hit the ❤ button at the bottom – I’m told it feeds the almighty algorithm.

In this newsletter:

The story behind gold’s surge

BTC still under pressure

Some of the topics discussed the past week:

Employment data: still no clear path

Rates: let’s get this started

A pivotal week, but not because of the data

A warning to Europe

Trump and the dollar

Spies everywhere

The debate impact

CBDC roundup: the EU, Hong Kong and China

CPI, yawn

Small businesses are nervous

Investment managers are also nervous

The story behind gold’s surge: rates, fiscal and military.

BTC still under pressure

The story behind gold’s surge

Something is going on with gold. And rates expectations. And the dollar. And much else besides, so let’s try to unpack this.

The gold price has been on a tear recently, but surged even more towards the end of the week.

(chart via TradingView)

That size of a move suggests big buyers, either institutional traders or central banks or both. What’s more, it coincided with a drop in the DXY dollar index, which reinforces the idea of foreign reserve adjustments.

(chart via TradingView)

I can think of three possible reasons:

1) Rate cut expectations have jumped again. On Thursday, I wrote that it felt like a relief to have markets finally reflect a more realistic expectation of a 25bp cut next week, rather than the overly optimistic (and alarming) 50bp. When I wrote that, the CME FedWatch model reflected an almost 90% certainty that the Fed would take the cautious route.

I logged on yesterday morning to see that we’re at 50/50. What happened?

(chart via CME FedWatch)

It can’t be the economic data. Thursday’s release of the August US Producer Price Index (regarded as a wholesale inflation indicator as it measures prices received by domestic producers) came in higher than expected on a month-on-month basis, both for the headline (0.2% vs 0.1% expected and 0.0% in July) and core figures (0.3% vs 0.2% expected and -0.2% in July). This is not worrying, as the Personal Consumption Expenditure trend (the Fed’s preferred inflation measure) should still be down, but it does suggest some caution is still warranted.

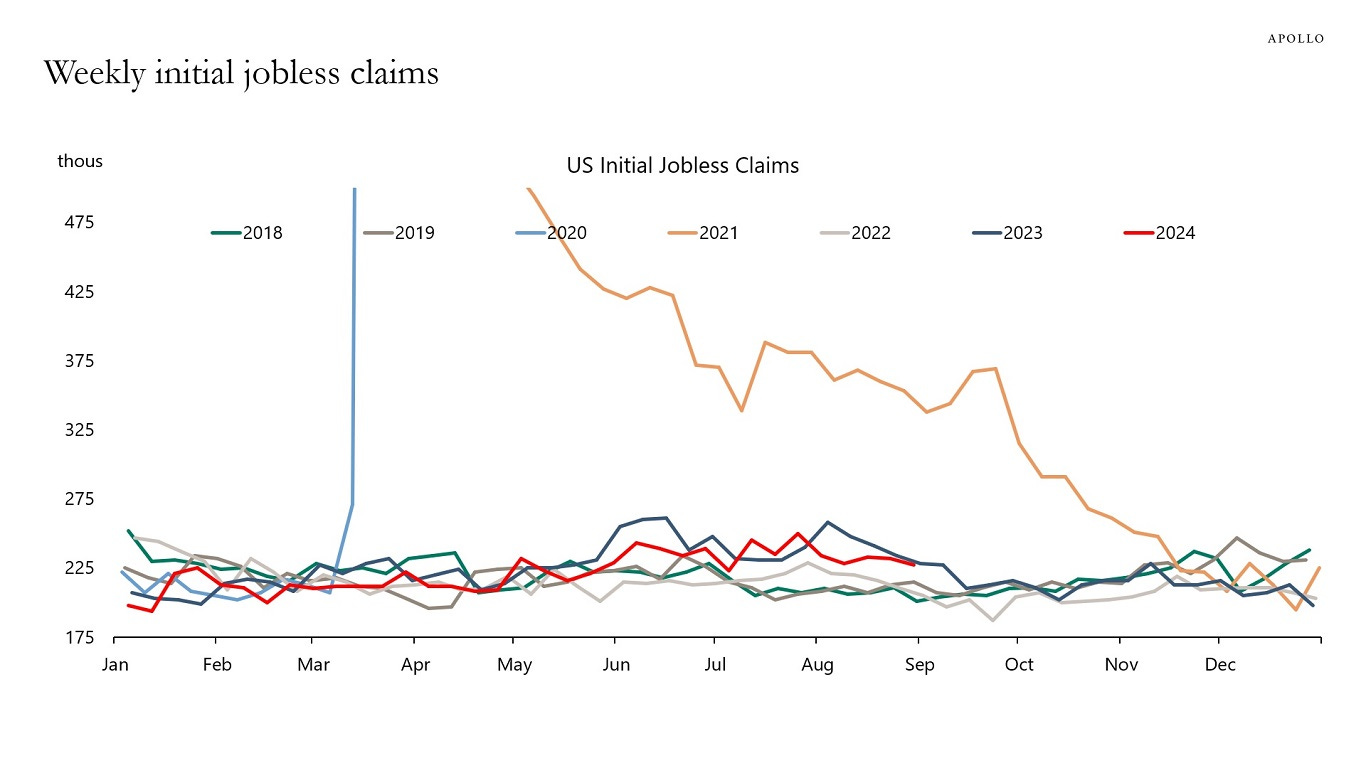

And there was nothing out of the ordinary in the weekly jobless claims data – these are still chugging along at normal levels for this time of year. The below chart from Apollo Global was plotted before this week’s release, but the new numbers showed a continuation so the point holds.

(chart via Apollo Academy)

What could have moved sentiment is an article in the Wall Street Journal published on Thursday by Nick Timiraos, who some refer to as the “Fed whisperer” for his ability to call FOMC decisions. Nick suggests that a 50bp cut is very much on the table.

“[Officials] are nervous about keeping interest rates too high for too long amid evidence that higher borrowing costs are working as intended to slow inflation by cooling spending, investment and hiring. They don’t want to let slip through their grasp a soft landing, in which inflation falls without a serious jump in joblessness.”

Nick does stress that Fed officials acknowledge that starting with a smaller cut gives them more flexibility while signalling a lack of grave concern. But he points out that they are aware of the case for a larger cut to get ahead of slowdown risk.

The below chart of payroll growth in previous rate cycles, shared in Nick’s article, shows that starting to lower interest rates is not enough to prevent a sharp drop in employment, which of course the Fed wants to avoid.

(chart via the Wall Street Journal)

Nick wasn’t alone – Colby Smith also wrote on Thursday for the Financial Times that the Fed faces a “close call”. What close call? After the CPI print, things looked pretty clear and there has been no data out since then to change that!

If these pieces were written by pretty much anyone else I would dismiss them, since I’ve long been in the camp that caution is warranted here because there is inflation uncertainty ahead and having to raise again would not just dent but bash confidence in markets and the Fed.

But the thing is, Nick and Colby know their stuff and it’s unlikely they’d write uncertainty-generating pieces just for clicks.

And, because Nick and Colby know how to read the data like the rest of us (probably better, actually) and know what the market has been expecting, we have to wonder why these two pieces came out on the same day. Both journalists no doubt have good sources within the Fed since they’ve been covering that beat for ages, and I’m not suggesting they were nudged to shift the tone, but they probably got some indications from somewhere that the market might be getting this wrong.

The renewed possibility of a 50bp cut next week goes some way toward explaining the dollar weakness, especially given recent reminders by Bank of Japan officials that more rate hikes from the largest foreign holder of US government bonds are likely. A weaker dollar is good for the gold price (the denominator effect, and the relative outlook).

Beyond the actual numbers, the uncertainty itself is damaging. This degree of doubt just a few days away from the FOMC meeting is unusual.

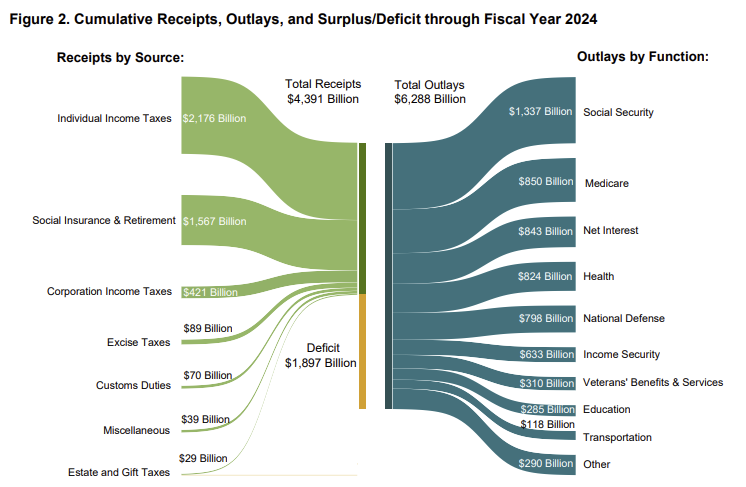

2) The US budget deficit just keeps on surprising. This week’s Treasury report for August showed that the monthly budget deficit of $380 billion didn’t just come in roughly $100 billion higher than consensus forecasts – it was the sixth highest on record. The accumulated deficit for the fiscal year to date (since the end of September ’23) is up to $1.9 billion, already the third highest on record, after 2020 and 2021.

According to the Congressional Budget Office (CBO), part of the overshoot was due to September 1 falling on a Sunday, which brought some payments forward to August. But even accounting for this, the monthly deficit still would have reached $300 billion.

I added up the overshoots for the fiscal year to date, the difference between the reported figure and consensus forecasts – so far, the budget deficit is a whopping $266 billion ahead of expectations. This is roughly 13% ahead of the CBO’s forecast of a $1.9 trillion deficit, which itself was recently revised up by 27%.

If the CBO’s forecast turns out to be more or less correct – in other words, if September’s deficit comes in at a meagre $93 billion 😂 😂 😂 , then the US will have increased its deficit by over 18% in a year in which the economy was doing well.

And since neither presidential candidate has even mentioned curbing the rate of increase, it could be that investors are concerned about the flood of US dollars that will be needed to finance the purchase of increasing debt issuance, especially if declining yields make US treasuries less attractive as a reserve asset.

(chart via the US Treasury)

In the chart above, note that the US so far this fiscal year has spent more on net interest payments than on defence. In a recent article on Bloomberg, historian Niall Ferguson pointed out that, throughout history, any great power that spends more on interest than on defence doesn’t stay great for long. This should worry investors. Rates will come down, but enough to offset the rising debt levels?

3) The risk of military escalation ratcheted up on Thursday.

Ukraine’s president Zelensky has been begging the US and the UK for authorization to aim donated missiles at targets within Russia, a move that Russia has repeatedly said would signal a “new phase” of the war. President Biden and Prime Minister Starmer met in Washington yesterday to discuss the issue, with the New York Times reporting on Thursday that approval was likely.

Putin has reminded them that permission would mean the US and UK are effectively joining the war, and that he would take “appropriate decisions”, which sounds diplomatically sinister. “This, of course,” he said, “will significantly change the very essence, the very nature of the conflict."

The shift in tone is especially unnerving as Russia is in the process of revising its nuclear doctrine and recently moved some weapons to Belarus, promising that they would only be used if Russia was threatened.

Against this backdrop, accumulating gold sounds like a good idea.

BTC still under pressure

But what about gold’s digital peer, bitcoin? Surely the factors propelling gold higher should also support BTC? A weaker dollar, the start of an easing cycle, geopolitical tension should all be good for BTC’s price – and yet it continues to lag. Last night’s bump is welcome (triggered by the move in rates expectations?), but it’s not yet clear that the factors keeping it down over the past few weeks have dissipated: political uncertainty in the US, and growing concerns about a market rout due to an economic slowdown.

(chart via TradingView)

The latest polls from Reuters/Ipsos give Vice President Harris a significant five point lead, while Predictit has her way ahead, at 57% vs Trump’s 46%. Polymarket has them neck-and-neck, but with increasing odds (now at 75%) that Harris wins the popular vote.

And macro uncertainty (see above) is not good for risk sentiment. On Thursday, I wrote about the latest S&P Global survey of institutional investors which showed that risk aversion was at its highest since May 2023.

Uncertainty changes, though. The current set will ease, to be replaced by others (geopolitical stress, currency debasement) that are likely to encourage BTC accumulation.

And I still believe that, whoever wins the US election in November, the regulatory hostility will ease – to varying degrees, yes, but the direction is not in doubt.

Meanwhile, gold is not tarnished (ha) by these uncertainties to the same degree: no regulatory confusion, and low macro correlation. In the “hedge against chaos” play, BTC is likely to take a back seat to its shinier alternative until the clouds disperse – unless, of course, relative price movements change the equation.

HAVE A GREAT WEEKEND!

By now, most of you probably know that I live in Madrid. I love it – the sky, the architecture, the people, the trees, the streets, the foods, the fountains, the museums, the shops, and even the public transport.

Speaking of which, our Ministry of Transport has created this divine and probably inadvertently hilarious video encouraging the use of public transport. It’s faster, more economical, better for the environment (all of which are actually true, at least in Madrid). And now, apparently, it’s even better than a Lamborghini. Love it.

(It’s just out, so I don’t think English subtitles are out yet, but hopefully soon. But you’ll get the gist anyway. Keep an eye on Lambo guy.)

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade.

Good morning. Hope all is well. I want to thank you for your recommendation of "The Twilight Before The Storm". I received it Friday and I am already on chapter 3. It reminds me of Neil Howe's book "The Fourth Turning Is Here", which he references in the Prologue. It has been a great read so far!