WEEKLY, Sept 21, 2024

what happened at the FOMC, BTC does not follow just one narrative, landscape awards

Hi everyone, I hope you’re all well! I for one am so relieved the FOMC suspense is over. Whatever happens at the next meeting, cut again or skip, the important shift is that the easing has started, and now it’s a question of how much and at what pace – opinions on that will shift as data comes in, but US rates are now, finally, on their way down. More on this below.

You’re reading the free weekly version of Crypto is Macro Now, where I reshare/update a couple of articles from the week.

If you’re not a premium subscriber, I hope you’ll consider becoming one! It’s the price of a couple of New York coffees a month, and you get ~daily commentary on crypto, macro and the space in between. Plus some cool links, a smattering of charts, and a daily music link because why not. AND you get access to a premium subscriber chat over on substack.com or on the app! And audio most days!

In this newsletter:

So it begins

What was said?

BTC does not follow just one narrative

Some of the topics discussed the past week:

Real rates are not high and credit has not tightened

Gaslighting, or a confused SEC?

The BTC cycle: where are we?

The Sony blockchain has momentum

Who decides what “safe” is?

Europe’s tokenization trials: window dressing, for now

Countdown time

The bigger deal

BTC does not follow just one narrative

SEC spotlight

So it begins

What was said?

Stablecoin use

Tokenization roundup!

SWIFT: Messaging as connectivity

Project Agorá gets bigger

Euroclear’s digital hybrid

What are institutions doing in tokenization?

Commerzbank and crypto trading

Feel free to share this with friends and family, and if you like this newsletter, do please hit the ❤ button at the bottom – I’m told it feeds the almighty algorithm.

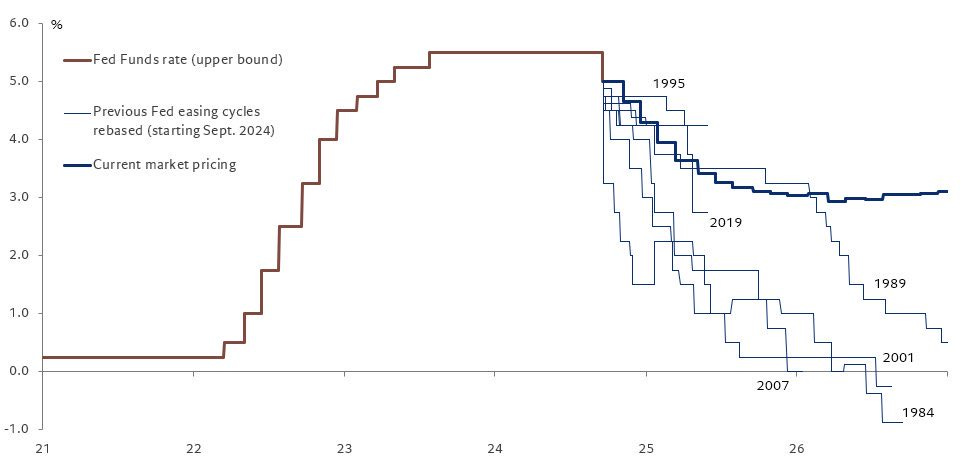

So it begins

Well, hunh, 50bp. This FOMC statement was an ideal example of something that was a surprise and also not a surprise, in a somewhat nonsensical contradiction. Regular readers will know that I didn’t think 50bp was warranted – but it became a strong possibility after informed (wink) mainstream media reporting last Friday flipped the market expectations.

Heading into the event, my feed was divided between those insisting a 50bp would be disastrous for the market, and those convinced it would send assets including BTC and stocks soaring. The former saw a message that the Fed is more worried than we realize; the latter were focusing on the additional monetary liquidity about to pour in to support prices.

Both were wrong, go figure. Prices jumped then fell, then started climbing again, and the S&P 500 reached yet another all-time highs on Thursday. “Safe haven” gold went up by even more, which highlights how split narratives are.

(chart via TradingView)

BTC, for a change, managed to outperform both, climbing more than 5.3% since the FOMC statement (vs gold’s 2.0% and the S&P’s 1.5%). This seems to be a case of pick-your-narrative: BTC could be riding risk asset sentiment, now that we have been given signs of stronger-than-expected monetary easing. Or, it could be echoing the message sent by gold, which is largely concern over currency debasement as well as conflict escalation. (I talk more about narrative choice below.)

(BTC chart via TradingView)

Bigger picture, we can finally step back and proclaim the easing cycle has started and liquidity will push prices higher. This should be bullish.

We can also continue to feel uncomfortably confident that “nothing stops this train”, and bringing down rates won’t unfortunately help the US deficit situation much – some, for sure, but not enough to change the outlook. In the absence of astonishing growth, that suggests more currency debasement (the deficit has to be covered somehow, and the only obvious path is currency dilution). Lower rates further encourage this. This is good for hard assets.

Only, I still think the 50bp cut, despite Powell’s protestations to the contrary, signals concern about a weakening economy. Put differently, I’m still left wondering about the messaging of a big cut when things are supposedly “fine”. The last two times the Fed started an easing cycle with a 50bp cut were in 2001 and 2007. Traders/investors who remember those periods are going to be uneasy, however “different” this cycle may seem.

(chart by Frederik Ducrozet, @fwred)

Meanwhile, tailwinds continue to build for BTC, as both a liquidity play and a breakdown hedge. Going forward, more liquidity combined with continued growth? Good for risk assets. Or, a re-ignition of inflation, economic chaos and political uncertainty? Good for longer-term safe havens.

Looking outside the US, the 50bp move should trigger a wave of further cuts elsewhere, as many central banks were reluctant to get too far ahead of the US cycle for fear of what that could do to their currencies. The easing ahead will be global, with the exception of Japan. This should also favour BTC and gold relative to equities.

What was said?

Some key takeaways from the FOMC announcement and Powell’s press conference:

The updated economic projections indicate expectations of two more cuts before the end of the year. This could mean a skip in November’s FOMC meeting (which starts the day after the US election) and then two in December, which should give them some flexibility to adjust if necessary while avoiding accusations of political bias (whoever wins). Or, it could mean a cautious 25bp in each of the remaining two sessions. Powell insisted in his press conference that it would “depend on the data”.

(table via the Federal Reserve)

The 50bp decision triggered the first dissent from a Fed governor (Michelle Bowman) since 2005. Even so, all 19 voting members pencilled in multiple rate cuts this year, a big departure from the June FOMC meeting in which the majority signalled 0-1 cuts.

When asked what was behind the decision to cut by 50bp, Powell singled out last month’s >800,000 downward revision to payrolls from the Quarterly Census of Employment and Wages, and anecdotal accounts from the Beige Book (a summary of economic conditions in the local economies of the regional Federal Reserves).

Interest rates are not going back to where they were. When asked about the level of the new neutral rate (the rate that neither constricts nor encourages economic growth), Powell said: “It feels to me that the neutral rate is significantly higher than it was back then”, referring to the pre-pandemic era. He used the word “significantly” which is, um, significant.

A new phrase has been introduced into my economic lexicon: “we only know it by its works”. Powell uttered these words at least a couple of times in his press conference, when asked about specific rate levels. I take it to mean: don’t know, but we’ll know it when we see it.

Intriguingly, the dispersion for the 2025 dot plot has narrowed, suggesting greater consensus about what’s ahead. Back in June, one FOMC member thought rates would still be at last week’s levels in December of next year (no cuts for a year and a half!). Now, most expect the fed funds to be in the low 3s, although – as Powell reminded us – there’s not necessarily a lot of individual conviction around these dots.

(charts via the Financial Times)

According to Powell, the labour market is “solid, and we intend to keep it there”. So, this 50bp move was pre-emptive, not a reaction to economic concerns. He stressed that the increase in the unemployment rate was largely due to an increase in the labour force.

And yet, going back to what I said above, starting off strong when – according to Powell’s prepared statement – the unemployment rate is still low and inflation “remains somewhat elevated” sends a confusing message. Moving to head off further deterioration with a strong move while recognizing lags sounds smart, but it’s a brave move from a Fed that has been consistently cautious since the pandemic.

That said, it’s a huge relief to get this key decision out of the way, and going strong this week does give the Fed margin to stay put at the next FOMC meeting, which starts the day after the US election. This should set up the path for another 50bp cut in December, along with more reminders to not expect this size to become the norm – unless, of course, the numbers have started to look alarming and/or the electoral result signals chaos ahead.

BTC does not follow just one narrative

I really don’t mean to pick a fight with BlackRock, but I heard something this week that irritated the heck out of me.

It was in this Bankless episode featuring Robbie Mitchnick, Head of Digital Assets at BlackRock. He chats to hosts David Hoffman and Ryan Sean Adams about the asset manager’s strategy and philosophy around crypto.

Mitchnick hammers home one point I strongly disagree with: that commentators are responsible for the harmful confusion around bitcoin’s narrative. As if there was a “correct” one. He even implies that some are doing this so as to be able to squeeze more profit from trading (something BlackRock has surely never done).

This view overlooks that bitcoin is many things to many people. No-one gets to imbue it with just one narrative.

It also underscores the institutional attitude that an asset has to fall into an easily defined bucket. And that large institutions decide what that is.

If we’re going to imply profit-seeking motives, we could suggest that the “one bucket” approach makes it much easier to sell products. Simple stories work better, so let’s make sure everyone comes around to that view, it would be so much more convenient, right? (I’m not saying that is what has shaped their narrative, I think they do believe what they’re saying – it’s the stones and glass houses mistake that’s disappointing.)

But bitcoin doesn’t care about institutional convenience, and a significant cohort of the people who trade it don’t, either.

Personally, I subscribe to the safety narrative, that’s why I hold BTC. I believe it is a good long-term hedge against currency volatility and debasement, and against the risk that global financial plumbing is creaking as geopolitical pressure and social strain collide with economic orthodoxy. Longer-term, bitcoin is not vulnerable to the monetary policy decisions of any one nation, or production changes, or corporate corruption, or predatory competition. It is the only truly hard-cap commodity traded on liquid markets, and like many commodities, there are many reasons for holding it.

I may see bitcoin as a defensive play, but I reject the idea that bitcoin should only be that. I should not get to decide, the market should. And BlackRock should not be scoffing at those that see bitcoin differently.

BTC is in many ways a risk asset, even though I prefer to not treat it as such. It has high volatility, no dividends to anchor value, no future cash flows to discount. Its future value is based on expected demand, which runs on narratives and events, both of which have a high degree of unpredictability. And if short-term investors treat it as a risk asset, that’s how it will behave, especially since traders tend to set the short-term price.

Putting my bristling aside, Mitchnick did have a refreshing take on the tokenization trend: it’s not contradictory to the focus on ETFs. Sure, one takes crypto assets and puts them in a traditional wrapper, and the other takes traditional assets and puts them in a crypto wrapper. Mitchnick sees both as appealing to different sets of clients for now, but they will eventually converge.

And I do have to take my figurative hat off to BlackRock’s role in facilitating a mainstream onramp for an admittedly hard-to-understand asset. Bitcoin should be about choice and access. BlackRock’s role in educating the public about bitcoin’s features is also to be commended (their latest report is pretty good), and I have no problem at all with them talking about just the hedge story, it’s one I believe in. My objection is the assumption that there is only one story to tell, and the inference that BlackRock gets to decide what that is.

HAVE A GREAT WEEKEND!

It’s that breath-taking time of year again – I’m talking about the Natural Landscape Photography Awards, that emphasize low-tech (as in, no AI or deceptive editing) glimpses of how magnificent this planet can be.

There’s too many stunning images to share here, even if I only limit myself to my favourites, so I recommend a visit to the website (especially moving if you have a large screen). But here are three that jumped out:

Thomas Spinner

Andrew Mielzynski

Peter Meyer

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade.