Stablecoins and mission creep

Plus: what’s ahead this week, US consumer sentiment, Singapore and more

“Communications tools don’t get socially interesting until they get technologically boring.” – Clay Shirky ||

Hello everyone! Those of you who enjoyed a long weekend for the memorial day holiday, I hope it was a great one, whatever the weather. I took advantage of the break to put away the winter clothes and pull out the t-shirts, and I am now so ready for summer. Got the mint water chilling in the fridge, watermelon on the countertop, and a new mug for my iced coffee. Bring it on. 🌞

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

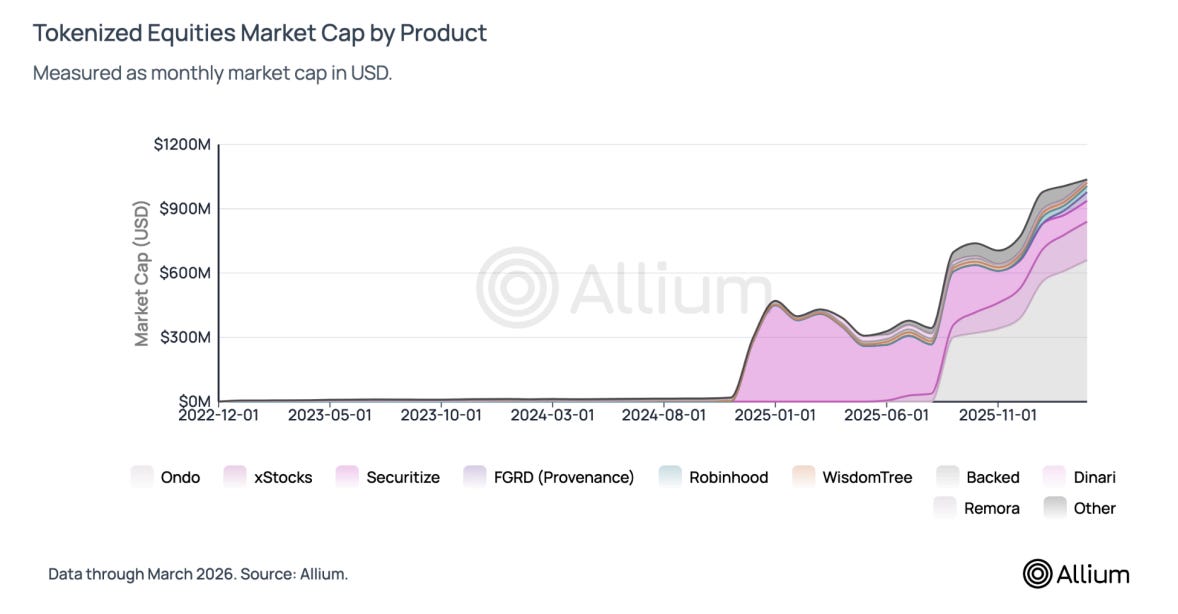

Tokenized equities hit ~$1B in supply since launching in mid 2025. The market structure is more interesting than the milestone.

Allium’s latest research covers where liquidity actually lives, how tokenized prices compare to traditional equities, overnight price discovery, and why ~90% of volume is outside the US.

For fintech platforms, exchanges, institutional investors, and builders evaluating the tokenized equities opportunity.

→ Read the report: https://www.allium.so/reports/allium-tokenized-equities-report-q1-2026

IN THIS NEWSLETTER

Coming up this week: PCE, defence

Stablecoins and mission creep

Macro: US consumer sentiment

Term of the day: Shangri-La Dialogue

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you so much!! ❤

WHAT I’M WATCHING:

Coming up this week: PCE, defence

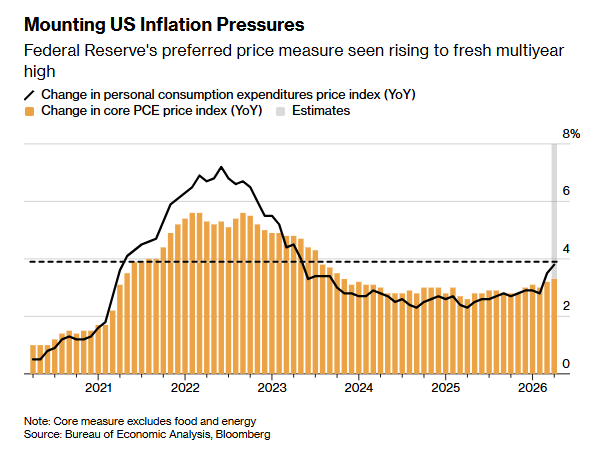

The big deal this week is the April Personal Consumption Expenditure (PCE) data, which should confirm the uptick in US inflation. We also get a ton of speeches from Fed officials, not that interesting really since we know what they’ll be saying. There could be some diplomatic sparks over the weekend in Singapore.

Today (Tuesday), the US Conference Board releases its consumer confidence report for May.

On Thursday, we get the April read of the US Personal Consumption Expenditure (PCE) index. The core index, ex-energy and food, was former Fed Chair Jerome Powell’s preferred inflation gauge. Current Chair Kevin Warsh seems to favour the trimmed mean, but he will struggle to get us all to divert our attention from the PCE – muscle memory is strong.

Anyway, the consensus forecast for the headline PCE year-on-year growth in April is for 3.8%, an acceleration from March’s 3.5% and a full percentage point higher than just two months ago – this would mark the steepest two-month acceleration since late 2021. As with the CPI, much of that is due to higher food and energy costs – strip those out, and the core index is forecast to have increased by 3.3%, the highest since November 2023.

(chart via Bloomberg)

We also get data on US personal spending and income, which should give a hint as to whether the decline in consumer sentiment (see below) is seeping through to economic activity.

And we get the second estimate of US GDP for Q1 – the first estimate, released almost a month ago, showed growth accelerating to 2.0%, from 0.5% annualized in Q4. We’ll also get the revised quarterly core PCE growth for Q1, which covers only one month of the Iran conflict – the first estimate showed an acceleration to 4.3% from 2.7%.

Friday sees the kickoff of this year’s Shangri-La Dialogue, Asia’s most significant defence and security conference – see below for more detail.

Stablecoins and mission creep

They’re not even pretending anymore: the European Central Bank (ECB) doesn’t like the idea of stablecoins.

There has been some lip service to the concept over the years, some mumbling about supporting commercial bank initiatives to modernize payment rails. Even the central bank’s digital euro project was initially presented as a reluctant alternative to ineffective private solutions – the implication was that a euro stablecoin would be great if only it were possible, but since it looks like it isn’t (or so we’re told), here we are with a beautifully centralized alternative.

But innovation is a natural force (yes, even sometimes in Europe), and last week produced a handful of headlines that must have ruffled many ECB feathers.

First, there’s the surge in the number of commercial banks joining the Amsterdam-based Qivalis stablecoin consortium, with 25 new entrants pushing the total up to 37. I’ve never seen a consortium in any industry, but especially not in finance, grow so fast.

Also, last week the European Commission (EC) published two public comment consultations on the MiCA crypto framework, including questions such as whether users should be able to earn interest on balances, whether redemptions should be charged fees, whether tokenized securities should be brought into the framework, and so on. The vibe is one of wanting to adapt to the US GENIUS Act by giving private euro stablecoins some breathing room in order to lift their volumes from insignificant levels in the face of continued global growth of stablecoin adoption.

And on Tuesday, President Trump signed an Executive Order requesting that US financial regulators look into how to give stablecoin issuers (and other fintechs) access to central bank liquidity.

That idea is rearing its head in Europe, too. Last week, Brussels think tank Bruegel put out a policy brief advocating for stronger euro stablecoin support as, rather than protect the euro-area financial system from digital asset risks, the EU’s restrictive approach is likely to do the opposite. Tokenization is picking up in global markets, the authors argue, and the absence of a liquid euro stablecoin ecosystem means more users will choose dollar-based alternatives.

The brief recommends that policy makers, among other measures:

Introduce measures to increase the liquidity of euro stablecoins on secondary markets;

Encourage interoperability between stablecoins and deposit tokens while establishing standards and oversight for bridges and connectors;

Change the MiCA rules on capital requirements and reserve allocation that penalize large issuers;

Remove the requirement that stablecoin issuers hold a large portion of reserves in bank deposits that pay little to no interest (this rule does nothing for financial stability nor credit formation, and disincentivizes euro stablecoin creation);

Allow issuers to pass on some of their earned income to incentivize adoption, keeping yields below the standard deposit rate and that on ECB reserves;

Accelerate the integration of central bank money and DLT platforms;

Allow regulated euro stablecoin issuers access to central bank reserves, effectively making euro stablecoins fully-backed programmable central bank money – this would remove the risk of banking sector stress spilling over into stablecoins.

The ECB immediately pushed back with the usual nonsensical rhetoric about stablecoins weakening bank lending and introducing structural risk. The suggestion the central bank seemed most triggered by was the suggestion of access to central bank liquidity, even though the US is heading in that direction.

That won’t be enough to sway the vocal opposition from ECB chief Christine Lagarde, who earlier this month said:

“Our task is not to replicate instruments developed elsewhere, but to build the foundations and the infrastructure that serve our own objectives.”

In that same speech, she also said:

“…the case for promoting euro-denominated stablecoins is far weaker than it appears”.

What no one is asking is why she is giving speeches on new technology applications in the first place? Sure, the way value moves around an economy can have an impact on the smooth functioning of payment systems – but it’s not clear that would matter much for price stability, the ECB’s main mandate.

It’s also not clear how introducing a digital euro to compete with the digital appeal of stablecoins has anything to do with price stability. The stated aim is to prevent mass adoption of dollar stablecoins – but it’s not clear why a central bank solution is essential, nor why the central bank itself should be trusted to make that call.

Come to think of it, a lot of what Lagarde herself has been promoting over the past few years does not have much to do with her institution’s mandate. From belittling some new technologies while promoting others, to pushing a certain climate agenda and meddling in fiscal matters, we are looking at a clear example of mission creep, and no influential European leader is daring to question her power grab.

The blatant mission creep started almost immediately after Lagarde took office in 2019.

In May 2020, the ECB published a guide on environmental risks – why?

Oh, right:

“The ECB is of the view that institutions should take a strategic, forward-looking and comprehensive approach to considering climate-related and environmental risks.”

In 2021, the ECB announced that it would take a corporation’s ESG footprint into consideration when deciding which bonds to buy – this was at a time when the central bank was resorting to corporate bond purchases in an attempt to stimulate economic activity as its government bond purchase capacity had reached its practical limit. Essentially, the central bank was choosing to favour some companies over others within the same credit quality for ideological reasons.

In 2022, the ECB started requiring banks to assess and disclose climate-related risks in their lending portfolios, effectively influencing private company decisions by linking capital requirements to environmental considerations – for instance, banks that have a high exposure to the oil and gas industry could face a higher capital requirement than banks with a high exposure to private equity funds or risky startups.

And despite supposed central bank independence, Lagarde has frequently meddled in fiscal policy, giving several speeches over the past few years advocating for certain government spending strategies.

Now, the ECB wants a direct line into consumer activity by managing digital wallets. If the “activist” mentality continues even after Lagarde steps down next year, it’s not a stretch to imagine the digital euro wallet disincentivizing certain types of purchases for being not environmentally friendly enough, or for weakening a certain policy objective.

All of the above seems to forget that the ECB’s mandate is price stability. Supporting the economy is also a mandate, but secondary to price stability. It is arguably not the ECB’s job to recommend certain non-monetary policies, nor is it the ECB’s job to favour one type of technology application over another based on risk assumptions that reveal a limited understanding of the technology.

The digital euro project has been painted by many (myself included) as an inappropriate power grab from an institution that wants to expand its relevance at the expense of greater opportunity for financial institutions and greater convenience for consumers.

What many of us are missing is that it is just one symptom of the mission creep that seems to have accelerated under Lagarde’s leadership. That makes it harder to push back on, as even if the current plan does not go through in the form she wants, we can expect other similar initiatives.

Or, perhaps pushback against the digital euro could, finally, trigger stronger questions about the ECB’s role in the European economy.

Then again, if there is only muted pushback and the European Parliament passes the draft law at the hearing tentatively scheduled for next month, we could see an emboldened ECB continue to march into new policy areas, further enhancing the economic and social power of an unelected institution.

Put differently, the digital euro fight is not just about CBDCs or stablecoins. No, it’s really about checks and balances on centralized power that always, instinctively, reaches for more.

See also:

ECB: stablecoins bad, CBDCs good (May 2026)

EU tokenization and wholesale CBDC (March 2026)

Digital euro politics (Feb 2026)

Macro: US consumer sentiment

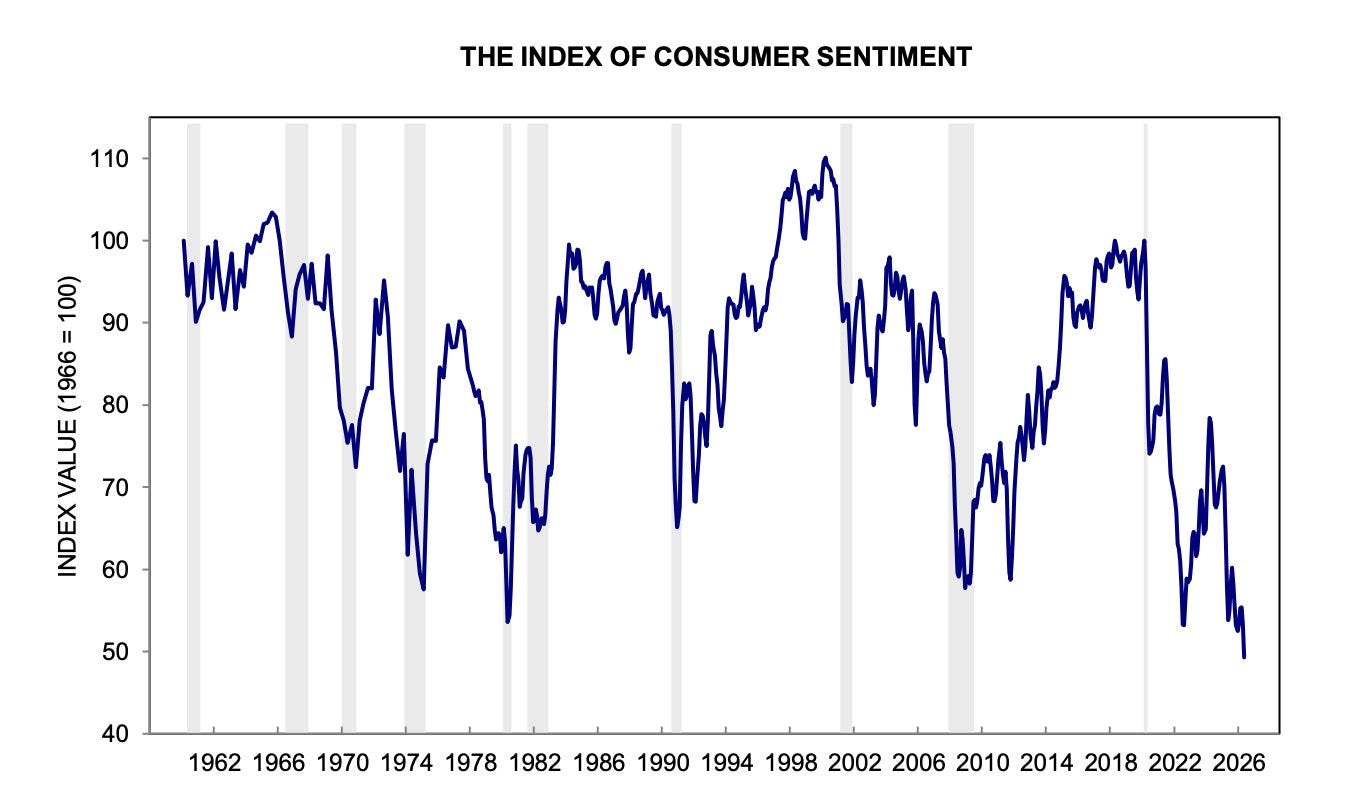

I know, this is getting repetitive, but the revised May report from the University of Michigan Consumer Survey showed that sentiment fell to another record low. This means that consumer sentiment is worse than during the pandemic, worse than during the 2008 financial crisis, worse than during the energy crisis of the 1970s, worse than during any recession since the survey started in 1946.

(chart via @SamRo)

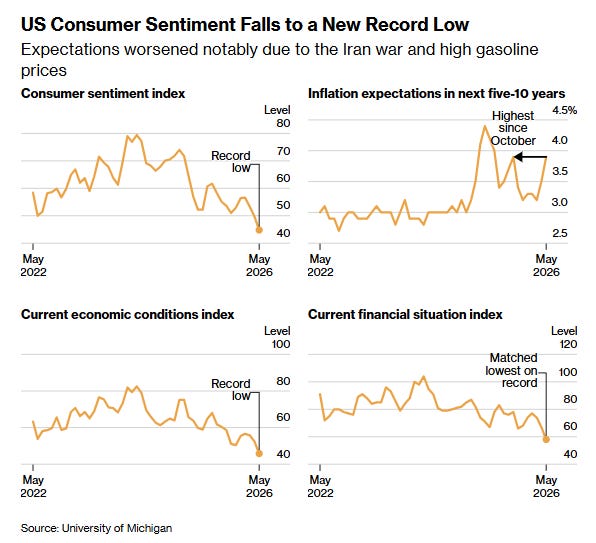

Not at all great, but not a surprise, with almost 60% mentioning the climbing cost of living, up from 50% last month.

(chart via Bloomberg)

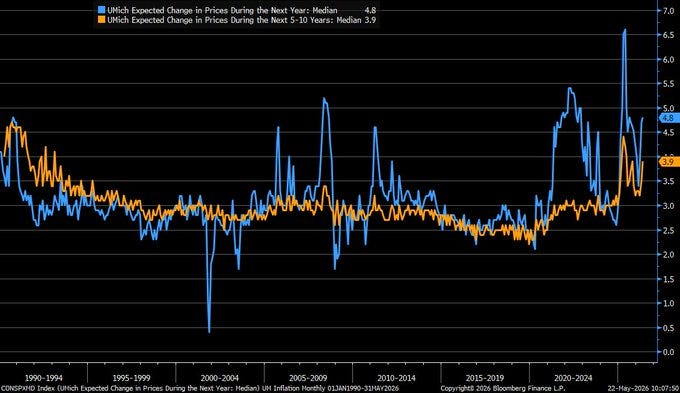

This is also apparent in the inflation expectations revision – this is a metric we know the Federal Reserve pays attention to, as when expectations climb, consumer behaviour changes.

And they’re climbing. The initial read showed that the median expectation of inflation one year out was 4.5%, slightly lower than April’s eye-watering 4.7% – the revised report shows that it was really 4.8%. Just three months ago it was at 3.4%.

The preliminary read for inflation expectations five to 10 years out was 3.4% - this has been revised up to 3.9%, higher than April’s 3.5%. The 5- to 10-year metric represents consumer expectations of the “natural, long-term rate of inflation. Both reads are starting to rhyme with “unanchored”.

(chart via @LizAnnSonders)

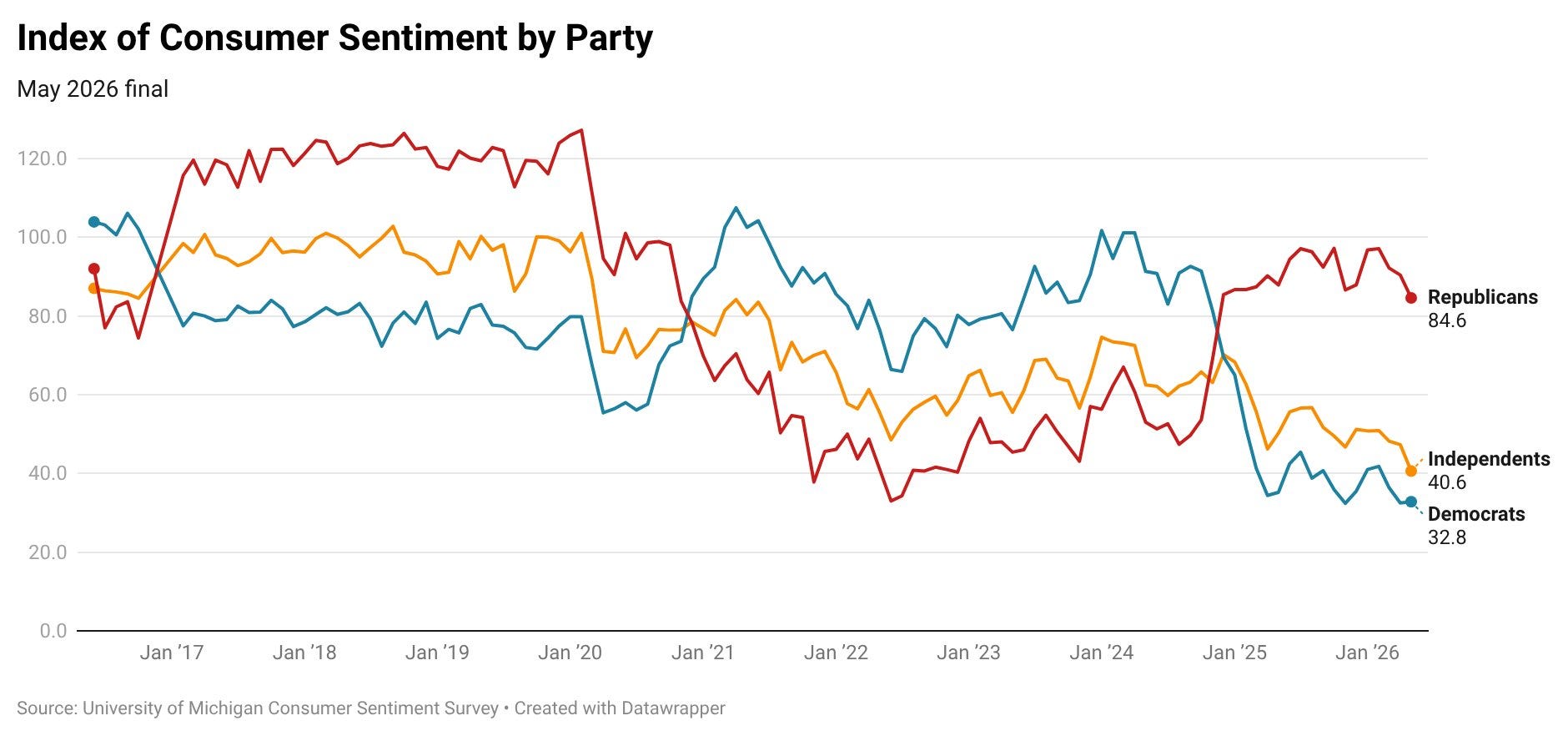

And before you huff and puff that the survey is useless because it is partisan – Republicans and Democrats respond as if they are living in different worlds – the University of Michigan did some digging for you.

To start with, sentiment is even declining for Republican voters.

(chart via @horvick)

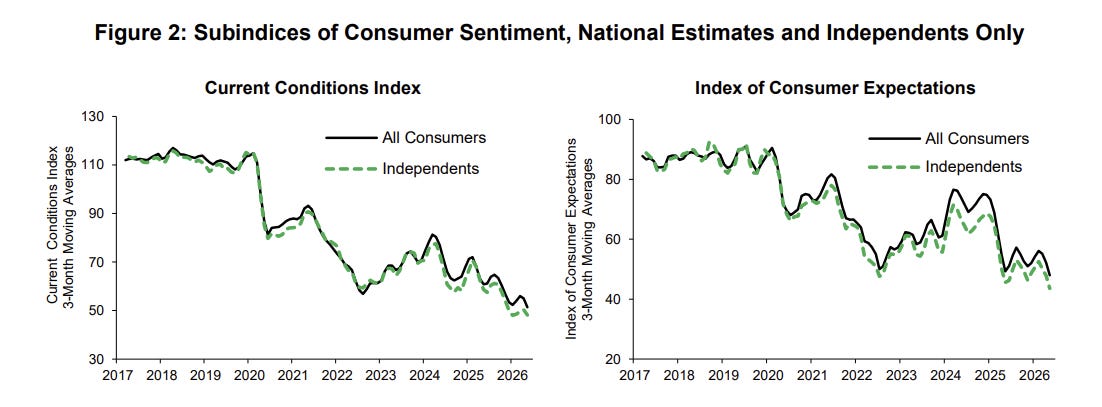

And, according to a report published last week by the survey organization, the responses from self-declared independent voters – now a record 45% of the population – closely track the survey average. Go figure.

(chart via the University of Michigan)

So, partisan, sure, but still relevant.