WEEKLY - fake reprieves, weak bases

why there's more turmoil ahead, and what could restore trust

Hello everyone, I hope you’re all doing well! Crazy, exhausting and yet important times.

You’re reading the free weekly Crypto is Macro Now, where I reshare/update a couple of posts from the week, offer some interesting links I came across in my weekly reading, and include something from outside the crypto/macro sphere that is currently inspiring me (it’s a fascinating world out there).

If you’re not a subscriber to the premium daily, I do hope you’ll consider becoming one! For $12/month, you’ll get ~daily commentary on how crypto is impacting the macro landscape, and vice versa. I talk about adoption, regulation, tokenization, stablecoins, CBDCs, market infrastructure shifts and more, as well as the economy and investment narratives.

Feel free to share this with friends and colleagues, and if you like this newsletter, do please hit the ❤ button at the bottom – I’m told it feeds the almighty algorithm.

Production note: next week is the Easter holiday, I’ll be taking Thursday-Monday off (inclusive), and so this newsletter will be skipping publication next Saturday.

In this newsletter:

The reprieve that isn’t really

Why the tariffs will be temporary

Some of the topics discussed in this week’s premium dailies:

Why the tariffs will be temporary

Podcast notes: Scott Bessent on Tucker Carlson

Macro-Crypto Bits: markets, recession predictions, macro data, China’s reaction

Two wolves: trade is bad, high yields are bad

Macro-Crypto Bits: markets, China, Japan, Germany

Coming up: CPI, PPI, vibes and more

Between the cracks, the bigger picture emerges

Macro-Crypto Bits: Tariffs, Markets

The reprieve that isn’t really

Macro-Crypto Bits: markets, CPI, Russia, Iran and more

Traditional safe havens go haywire while de-dollarization gains momentum

Macro-Crypto Bits: PPI, tariffs, realignment, activity slowing and more

The reprieve that isn’t really

After some alarming moves in the US treasury market earlier this week, President Trump changed his mind on the tariffs that went into effect at just past midnight on Wednesday.

In a somewhat furious post on Truth Social later that same day, he announced that tariffs on China would be increased to 125%. But the application of tariff rates above 10% would be delayed by 90 days.

Markets celebrated. The S&P jumped 9.5% on Wednesday, in a move that feels largely driven by short covering, delivering the largest swing since 2008. The Nasdaq soared by over 12%, its best day since 2001.

(chart via Bloomberg)

Yet, as we saw, that turned out to be no more than a relief rally largely driven by short-covering, rather than the much hoped-for change of direction.

The vulnerability

To understand why, we have to look at what led to the sudden pivot. According to reports and common sense, President Trump got spooked by Tuesday’s surge in yields and credit spreads. President Trump even admitted as much when speaking to the press, although Treasury Secretary Bessent took the more diplomatic and strategic stance of insisting the bond market had nothing to do with the decision.

Trump’s honesty here is more refreshing. But the signal leaves open a big weakness for antagonists and trading partners to exploit.

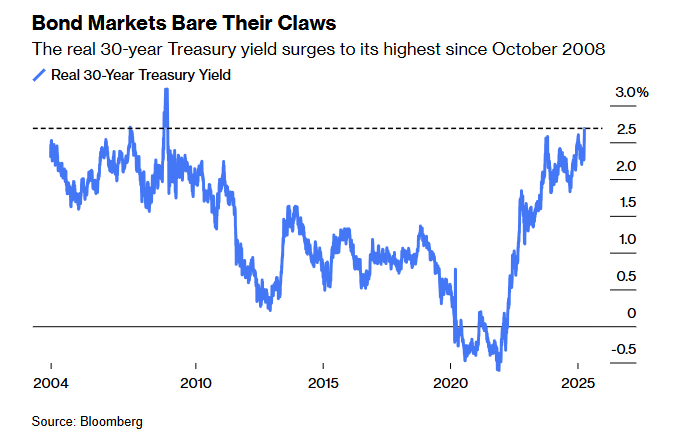

The loud message is that the President has an Achilles heel: stability in US treasuries. And the past week has shown that the world’s “safe asset” can become unstable fast.

The yield on the US 10-year treasury saw its steepest weekly jump since 2001. The yield on the 30-year treasury has seen its steepest weekly climb since the 1980s, reaching levels not seen since the Great Financial Crisis.

(chart via Bloomberg)

And intraday volatility has spiked across the tenors.

(chart via Bloomberg)

This is not supposed to happen in what is considered to be the world’s “safe collateral”.

And if US government bonds can’t be considered safe, borrowing costs go up, collateralized markets go haywire, and finance pretty much stops functioning.

So, seeing the volatility in the Treasury market, Trump flinched.

This opens up a vulnerability.

China

Who is the second largest foreign holder of US treasuries? China.

The 125% tariff was bumped yesterday to 145%, and China retaliated by increasing its tariff on US imports to 125%, but the actual level no longer matters since at such high rates there is effectively a trade embargo between the two countries.

The fallout for supply chains is as yet unknown, but it will be significant and will impact not just retailers and manufacturers waiting for Chinese goods and parts, but also ports, warehouses and more. A member of my family works for a digital commerce platform which has already started layoffs.

US officials, including Bessent, continue to insist that China will have to negotiate, that they’re “waiting for the call”. They will probably be waiting for a long time.

Just as Trump does not want to appear to lose face or concede anything (other than to the bond market, I guess), nor does President Xi. Politically, he can’t afford to. What he can afford to do is wait – he doesn’t have politics or midterms to worry about. And the Chinese have more experience enduring economic hardship than do Americans.

What’s more, it won’t be hard in this media environment for Chinese authorities to blame any growth setback on the US. Painting it as the “bad guy”, the aggressor, could enhance the impression of cohesion and the message of national unity.

Inflation and uncertainty

And, let’s not forget that there is still a 10% tariff on everyone, with 25% on steel, aluminium and autos. There is no way this doesn’t feed through to inflation.

Plus, the chasm of uncertainty has been widened even further by Trump’s continued flip-flops. The biggest damage to GDP will come not from rising prices and broken supply chains, but from frozen investment as businesses wait to see where things settle. Even foreign businesses enticed to set up factories in the US so as to avoid tariffs could choose to wait a couple of years in the hopes that Congress wrests Trump’s tariff power away from him after the midterms.

Speaking of which…

Why the tariffs will be temporary

In the ranking of words that are liberally overused, “temporary” has to be way up there. It’s a vague term – in the long run, almost everything is temporary, as in “not permanent”. In the arc of history, entire civilizations have proven to be no more than constructive phases of human evolution. In politics, systems come and go. In economics, timeframes shorten even more.

Unfortunately for our anxiety levels, the modern fire hose of information and our collective addiction to the adrenaline rush of hard-hitting news has shrunk our attention spans and given “temporary” a much tighter remit. This becomes particularly relevant in social media presidencies that thrive on incendiary rhetoric and quick wins.

So, “temporary” has come to mean days, weeks or perhaps, at a push, months. It’s a more comforting application as we search for quick solutions. But it doesn’t preclude stepping back, taking a breath and thinking past what we see on our screens. And it is in that spirit I can say with confidence that the current US drama is temporary, at least in the flexible interpretation of the term.

We can be 100% certain the Trump tariffs won’t last “long”, another overused vague word. We’re underestimating the internal pressure, not necessarily from the President’s inner circle, but from the US political system.

Put differently, politics will mitigate the potential destruction. Some of it, anyway.

It’s an emergency

First, let’s examine why a handful of people with a sketchy grasp of history has the power to do so much damage to the world economy.

In 1962, Congress passed the Trade Expansion Act, which contained a statute (Section 232) that gave the president broad authority to act unilaterally on trade matters if national security was at stake. Trump used this for his 2018 tariffs on steel and aluminium, arguing that reliance on foreign suppliers weakened US defence capabilities.

In 1974, Congress passed the Trade Act, which contained a statute (Section 301) that gave the president discretion to apply trade-related measures such as tariffs in retaliation for unfair trade practices. This was the justification for Trump’s 2018 tariffs on China in retaliation for IP theft and unfair licensing rules.

But the latest tariffs were not pushed through using those powers. Rather, they were implemented under the 1977 International Emergency Economic Powers Act (IEEPA), which gives the president authority to create new economic rules during a national emergency, which can be declared in response to an “unusual and extraordinary threat” originating outside the US.

These powers were a frequent feature of Trump’s first term, such as when he declared a national emergency at the US-Mexico border to allocate funding for the wall and threaten tariffs on Mexico, and when he declared a threat to US information and telecommunication technology, banning transactions with Huawei, TikTok and WeChat.

Last Wednesday, Trump declared that “foreign trade and economic practices have created a national emergency”. The White House Fact Sheet went on:

“President Trump is invoking his authority under the International Emergency Economic Powers Act of 1977 (IEEPA) to address the national emergency posed by the large and persistent trade deficit that is driven by the absence of reciprocity in our trade relationships.”

Now, it can be argued that the large and persistent deficit is not a “national emergency” but rather a structural consequence of issuing the world’s reserve currency. The question is how many elected representatives will be willing to take that on. Congress has never before overturned a presidential national emergency declaration, but there has never been as much cause to.

It's not just that this is the first time the IEEPA has been used to punish all trading partners for having “unfair trading practices” that are not actually unfair (in some cases, sure, but not all). Nor is it just that this is the first time that the IEEPA has been used to execute broad economic policy. And it’s not just that this move is an astonishing power grab by the executive branch, even by this Administration’s standards.

It’s also that the potential damage to the US economy is likely to damage the Republican Party’s prospects in the upcoming mid-terms, and many representatives would like to head that off if possible.

A glimpse of resistance

There is some movement on this.

Last Wednesday, just hours after Trump announced his global tariffs, the US Senate passed legislation that would remove the new tariffs on Canada by ending the “national emergency” used as justification, with four Republicans voting with the Democrats. The bill now goes to the House of Representatives.

Last Thursday, Senator Chuck Grassley (R-Iowa) together with Senator Maria Cantwell (D-Wash) introduced a bill that would require congressional approval for new tariffs. On Friday, seven other Republican senators joined as co-sponsors (Lisa Murkowski of Alaska, Mitch McConnell of Kentucky, Jerry Moran of Kansas, Thom Tillis of North Carolina, Todd Young of Indiana, Susan Collins of Maine and Amy Klobuchar of Minnesota).

And over the weekend, Don Bacon (R-Neb) said he will introduce a bill to restrict Trump’s tariffs.

For now, these all seem like a long shot. Even if the Senate bill is passed, and even if it then gets admitted for a vote in the House (Speaker Johnson is likely to do what he can to block this), and even if it passes that, Trump could veto. That could be overturned but would need a two-thirds majority which will be much harder to muster.

But, the mid-terms are getting closer every day, and as the economic realities of the trade war start to bite, votes could change the balance of power. Deep Republican states are unlikely to elect Democrats, but there are enough seats up for re-election in swing states currently represented by Republicans for a possible loss of both the House and the Senate. Again, any bill that passes both chambers could be vetoed, but an override would become less of an unsurmountable obstacle.

I expect, however, that it won’t come to that. We’ll see political pressure start to do its thing before the end of this year. Losing both the House and the Senate next year would be more than just a defeat, not least because we can expect Democrats to move fast on impeachment proceedings.

Plus, there’s possible recourse via the courts. Again, a long shot and at best slow, but not out of the question – after all, the Supreme Court did overturn Biden’s student loan cancellation.

Last Friday, the New Civil Liberties Alliance (NCLA) filed a lawsuit challenging Trump’s tariff on China that makes some excellent points. It argues that the IEEPA was meant to be used as a facilitator for targeted actions, not as an excuse for broad economic policy. It also points out that the law says the measure has to be “necessary” to resolve the “national emergency”, and that there is no direct relationship between tariffs and the fentanyl crisis (the reason given for the initial 20% tariffs on imports from China). And, more broadly, tariffs are a tax on imports and therefore can only be imposed by Congress per the Constitution. It won’t be hard to extend these arguments to cover the “Liberation Day” tariffs, as basic trade economics can show that deficits and surpluses are based on much more than import costs.

But, court rulings are hard to predict, and the lawsuit has been assigned to a Florida district court judge appointed by Trump. Whatever the decision, appeals could send this all the way to the Supreme Court, but even then, it’s not clear whether the bench would want to push back on what Trump is presenting as a “national security” issue.

So, all eyes will be on the hard data, as economic reports combined with approval ratings of the party are likely to be the only factors that could influence Trump’s position.

Meanwhile, political resistance will continue to build – not fast enough to stem the outflow from markets, but enough to mitigate the longer-term damage. And when Trump’s moves are walked back (and they will be), the relief recovery will not dull the pain of what has happened over the past few days, but it will bring new narratives.

ASSORTED LINKS

Introducing a new section where I share, you guessed it, assorted links that I found interesting over the past few days on topics beyond just macro and crypto. There’s a high risk this ends up getting too long as I read a lot and most of it is jaw-dropping, brow-furrowing, view-changing or just plain inspiring, but I’ll do my best to keep this list varied and relatively concise.

Matthew Klein delivers what will become the textbook version of why Trump’s tariff approach more destructive than ineffective. (The Overshoot, How to Think About the Tariffs)

A good thread from Izabella Kaminska on how Trump’s unpredictability could be his most important asset in the negotiations – Xi can’t do “crazy” like Trump can, which could be a disadvantage in the “mutually assured economic destruction” stakes. An interesting take, but I still think “inscrutable” wins longer term. (@izakaminska)

The Economist shares a list of six films about financial chaos and a blurb on each: The Big Short, Margin Call, The Wolf of Wall Street, The Grapes of Wrath, Enron: The Smartest Guys in the Room, and Too Big to Fail. (The Economist, The six best films about financial turmoil, paywall)

For all you number nerds, Aeon has a fascinating essay written by Benjy Barnett on the concept of zero, how not all societies perceive it the same way, what it teaches us about how our brain works and why this is relevant to other forms of scientific exploration. (Aeon, Why nothing matters)

In writing about the friendship and rivalry between national security advisers Zbigniew Brzezinski and Henry Kissinger, Henry Luce describes an era when statecraft implied craft, and ideology was more focused on common goals. (Financial Times, The last grand strategists: what Brzezinski and Kissinger could teach Trump, paywall)

I grew up a fan of the Moomins, and it warms my fuzzy heart that my daughter is too. So, judging by the available merchandise these days, are millions of young people around the world. However, few know the origin story, born in war and written atop a theme of homelessness and searching. Sad, perhaps, but a healthy reminder that the most enduring childhood fables are about confronting darkness. (The New Statesman, The dark side of the Moomins)

Short and compelling thoughts from Ted Gioia on how communication is changing, from the hieroglyphs of emojis to dialogue vs chatter. A sample: why ban books when you can instead get people to voluntarily abandon literacy? And: talking to no-one used to be called crazy, now it’s called “tech”. (The Honest Broker, 40 Observations on Public Discourse, paywall)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

This is Estonia’s entry for this year’s Eurovision Song Contest. If Tommy Cash doesn’t win the trophy and/or immediately get Italian citizenship, I will lose faith in the karmic system.

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade.