WEEKLY - OUSD, crypto + AI + democracy

plus: congratulations, Cape Verde, for making the World Cup magical

Hello everyone! I hope you’re all doing well, and getting ready for a fulfilling summer…

HAPPY FOURTH OF JULY to all my American readers!!! And happy 250th birthday, America.

You’re reading the free weekly send of the premium daily Crypto is Macro Now, where I re-share a couple of the week’s posts and some non-crypto and non-macro links since it’s the weekend. 🌼

PUBLISHED IN PARTNERSHIP WITH: ✨ ALLIUM ✨

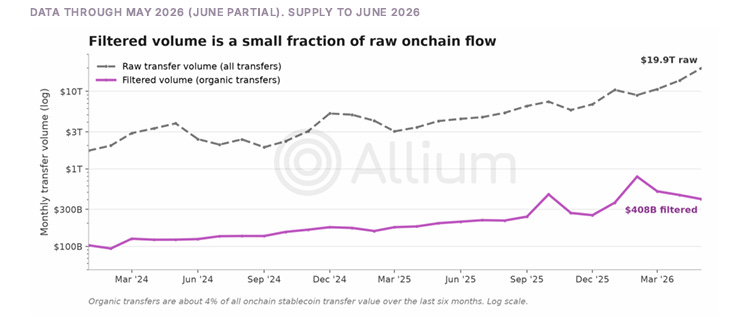

A large share of onchain stablecoin movement is automated or internal: market-maker rebalancing, exchange sweeps, looping through smart contracts, and wallets shuffling funds between their own addresses. Counting all of it overstates how much real sending and spending happens.

Would you like to know how much of stablecoin volume is real?

→ Book a demo: https://www.allium.so/

In this newsletter:

OUSD: the promise and peril of scale

AI, crypto and democracy in the rear-view mirror

Weekend: Congratulations, Cape Verde

Crypto is Macro Now offers ~daily commentary and updates on the overlap between the crypto and macro landscapes. Plus links and more.

If you’re a premium subscriber, thank you!! ❤

Podcasts: upcoming streams

✨ Monetary Forces: next Tuesday, Izabella Kaminska and I pick at the key headlines that paint the picture of how technology is changing finance, and Izabella will dive into the entrails of a paper illustrating an overlooked aspect of the transformation.

Tuesday, July 7 @ 4pm CEST / 3pm BST / 10am EST – livestream link: https://open.substack.com/live-stream/262758

✨ Press Publish: next Thursday, I’ll be talking to Marvin Barth about his Seriously, Marvin?! and Thematics Markets newsletters as well as his excellent podcast – we’ll get some insight into how he produces so much quality content, how he navigates the information firehose, how he deals with obstacles, what he thinks of different formats, and more.

Thursday, July 9 @ 4pm CEST / 3pm BST / 10am EST – livestream link: https://open.substack.com/live-stream/261155

Some of the topics discussed in this week’s premium dailies:

Coming up this week: central banks, US jobs

Monday mood: AI, crypto and democracy in the rear-view mirror

Podcast episode recommendations

Japanese stablecoins warming up?

Predictions update – how did I do?

Term of the day: El Niño

OUSD: the promise and peril of scale

Macro: Jobs warming up?

Markets: bleak BTC vibe

The moneyness of stablecoins

Macro: a simmer or a boil?

OUSD: the promise and peril of scale

In the unfolding drama that is monetary innovation, a new cast member has entered stage left. He exudes plenty of main-character energy: well-dressed, with heft and aura. You could almost hear the collective gasp from the audience.

But a few minutes in, it became clear this new personality didn’t have much of a script. We find out his name and we gather he means to be important, but his lines are as yet unformed, his motivation unclear, and his outline lacks structure. Suspense can be thrilling, though, and we can assume character development will come later, along with some plot twists. Still, there’s a feeling of deflation, of unmet expectations and of a missed opportunity.

Ok, perhaps that’s too theatrical a metaphor for what is ultimately an announcement about stablecoin infrastructure. But you’ll see what I mean.

On Tuesday, we heard for the first time from Open Standard, a new stablecoin initiative led by Zach Abrams, co-founder and CEO of Bridge, the stablecoin platform acquired by Stripe last year for around $1 billion.

Open Standard is launching a stablecoin OUSD, and it has over 140 partners already signed up to use it.

The list is a who’s who of tech and finance: Stripe, Visa, Mastercard, Amex, Google, Shopify, BNY, BlackRock, Standard Chartered, Mercado Libre, DoorDash, Aave, Coinbase and I could go on and on. The distribution power imbedded in this list is massive.

Only, it turns out that the triumphant press release was precipitate – several of the Korean names on the list have denied signing any partnership agreement.

Whether an internal communication issue or a change of heart from some participants, the project’s credibility has been hit.

And we could in coming weeks see further denials or defections. The list includes some hefty European payments companies (Adyen, Klarna and others) – this will no doubt send chills through the halls of the European Central Bank, already panicked about the potential demand for dollar stablecoins. Do the respective CEOs refuse to take a phone call from the ECB?

Beyond the inflated collection of names, we’re not told much more. Indeed, the partner list takes up more word-count than information about the project itself.

We are, however, given vague hints at three “design principles”. I’ll list them and highlight the frustrating lack of detail – but then I’ll suppress my irritation at what Omid Malekan calls “Proof of Press Release” and speculate on why this initiative could change the shape of the industry, as well as how it could fail.

1) Collaborative governance: Open Standard will be the independent operator, with a board made up of Open USD’s partners. What, all of them?? Many are competitors in a competitive market. Several stand to make a lot of money on free mint/burns and low-cost transfers, others will see their business model up-ended (which is always expensive) – and they’re expected to share decisions?

2) Seamless conversion: no cost for minting and redemption. For all users, or just partners? Can you be a user without being a partner?

3) Revenue sharing: All partners earn a share in the earnings from Open USD’s reserves. How will this be calculated and rebalanced? Will it depend on user balances and where they’re held? How will these be incentivized if they can’t pay interest? How much of a fee will Open Standard collect for management, and how often will this be changed?

Another unaddressed question is on what chains OUSD will run. Included in the list of partners are Solana, Coinbase, Stellar, Aptos, Tempo and other blockchain operators – does that mean OUSD will run on all their chains? How will interoperability work?

On to what the design principles imply:

The removal of mint and redemption fees is more significant than it may sound – it’s not just about cost for users, it’s about friction. Making conversion seamless will go some way towards further erasing the boundaries between onchain and offchain payments. Circle and Tether offer rebates to large users, which brings down cost but adds layers of informational friction – if users can stop wondering about the cost of entering or exiting a stablecoin position, the tokens become more “money-like”.

What most intrigues me, though, is the distribution of revenue – it never made sense that the passive income accrue to the stablecoin issuer rather than those doing the heavy yet crucial lift of distribution. Circle shares revenue with Coinbase and a handful of other distributors, but the circle (sorry) is small which limits the potential growth, especially as competition was always going to come hard for an increasingly commoditized business. Scale can be expensive to defend.

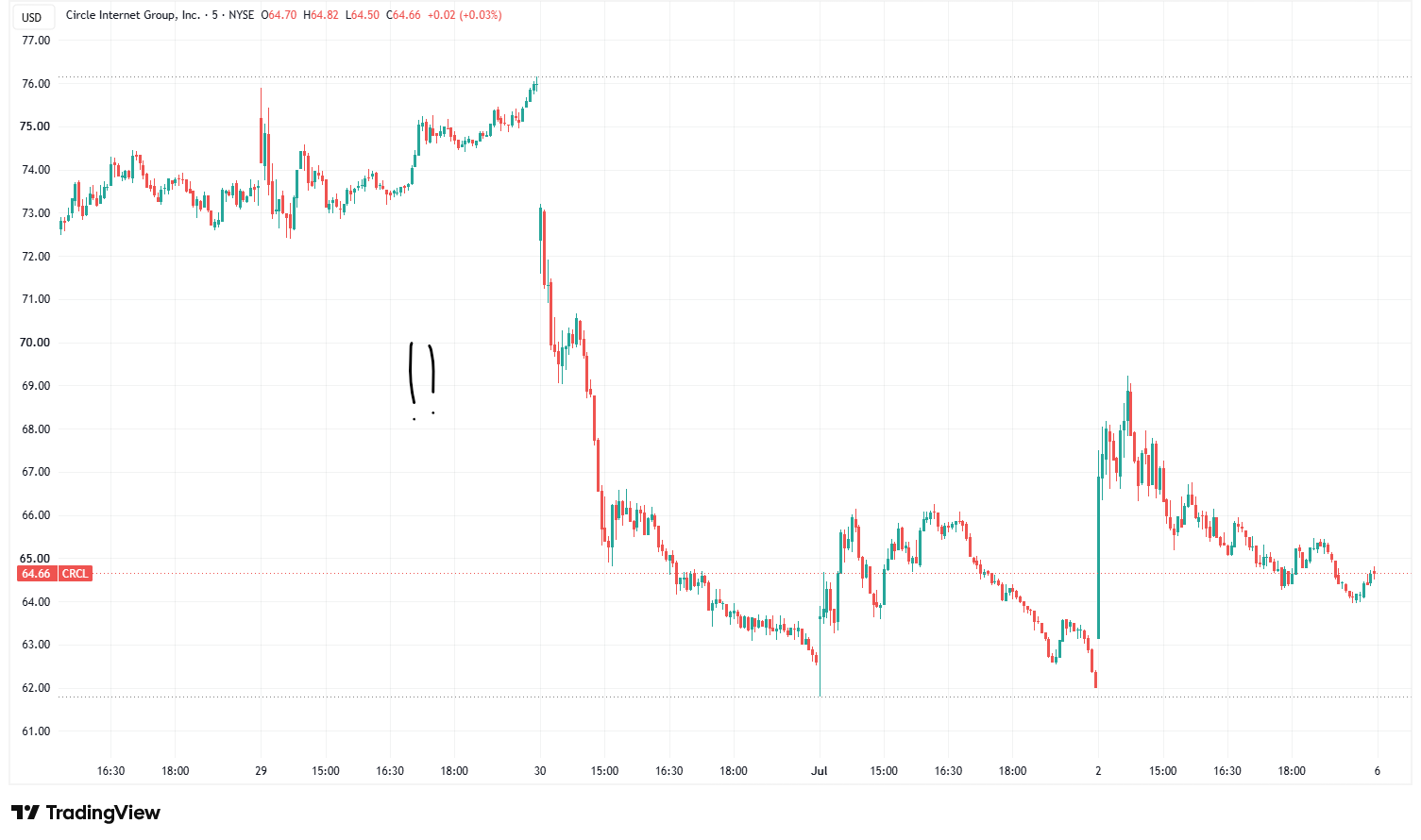

Indeed, the OUSD announcement is bad news for Circle – it’s share price was down almost 18% the day of the announcement, and it has not bounced.

(CRCL, chart via TradingView)

It’s not so much bad news for Tether, as USDT does not have a meaningful presence in what looks like the main target market for OUSD: corporate transfers between predominantly Western institutions.

Tether CEO Paolo Ardoino masterfully conveyed this in a post that simultaneously diminished Circle’s relevance (Player 2, really?? ouch):

Circle CEO Jeremy Allaire responded to the OUSD announcement with a long comment that understandably bristled with a defensive tone. But he does make a valid point: consortium governance hardly ever works well.

This brings me to my biggest question: how will the governance work? Any “cooperative” will tell you that shared decision-making is hard, even among small groups – just how much harder will it be in a group of more than 100? In principle, a consortium can be healthier for scale and transparency, and “neutral infrastructure” sounds amazing – but the “tyranny of consensus”, especially with such a wide range of priorities and moats, tends to lead to mediocre models and slow adaptation. It would be such a shame if the scale of the initiative’s ambition ends up deflated because, who knew, a large group with only a tenuous unifying thread struggles to agree on key issues.

But that aside, here’s what I think OUSD will end up becoming: an interchange layer. We’re not used to thinking of separate tokens as connectivity – but the absence of mint/burn fees and the scale of participants could make OUSD an efficient vehicle through which to access a broader network, while still retaining branding and customization.

After all, several partners already have stablecoins of their own (SoFi, Western Union, MoneyGram, Fiserv) – they won’t be giving up their initiatives, but could see OUSD as a “base layer” that could end up broadening utility and potential market size as stablecoin volumes grow.

Meanwhile, though, all we have is a vague and inaccurate press release. Open Standard expects the project to go live later this year, and unlike its big-name predecessor Libra (which also showed up with a hefty list of partners under its arm, many of whom defected early on), it is unlikely to face regulatory headwinds in its base domicile.

Elsewhere could be a different story, especially in jurisdictions threatened by dollarization. Perhaps we’ll also see Open Standard contemplate other currencies, at least to appease fearful monetary authorities?

One big shift that will become increasingly obvious, however, is the evolving narrative. Stablecoins started out as an onchain product (USDT, USDC, etc.). As regulatory support solidified, stablecoins-as-a-service became a thing, with a scramble for white-label issuance capability and a stack of related support features. Now OUSD, with many details still lacking, looks to be firing the starting gun on the stablecoin-as-infrastructure space.

AI, crypto and democracy in the rear-view mirror

The backlash against AI seems to be getting louder.

This will come as a surprise to many, since our social media bubbles can be strong – my X feed is frothing with excitement about the sheer power of the latest models.

But step back and sniff the air: the froth increasingly feels like a spending race, competition is emerging in overlooked corners, and the impact/valuation fear is becoming almost tangible.

What’s more, our two key sources for sentiment indicators – markets and surveys – are both telling us that AI scepticism is kicking in.

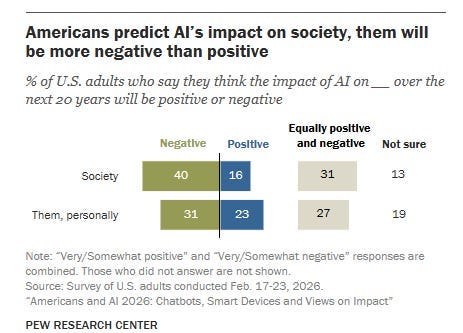

A Pew Research survey published earlier this month showed that more Americans believe AI will make society and them personally worse off, than those who see the positive effects outweighing the negative.

(chart via Pew Research)

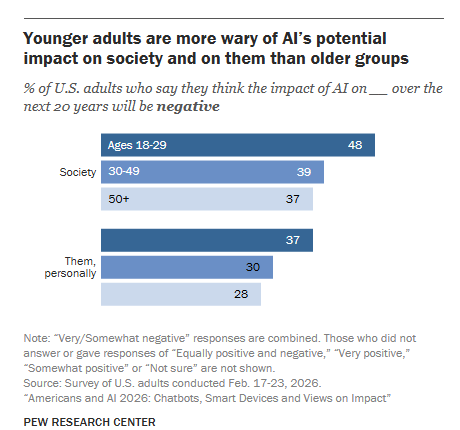

And, strangely – given how young people are typically more tech-friendly than their elders – the distrust is more pronounced among the young.

(chart via Pew Research)

Plus, the hardware build-out is hitting blocks. Politico reported last weekend that more than 20 counties and municipalities in Florida have passed or discussed moratoriums on data centres. According to an article last week in the Economist, local pushback led to the cancellation of at least 20 data centre projects worth $42 billion in the first three months of 2026.

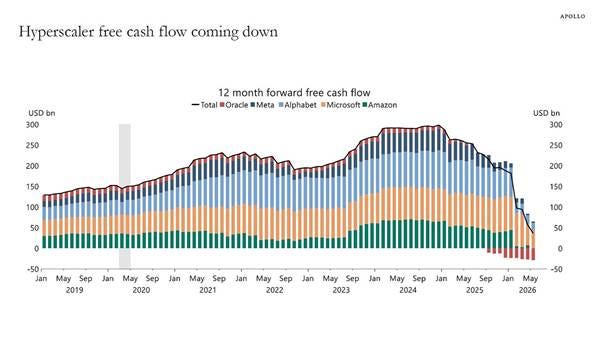

And hyperscaler free cash flow is dropping fast.

(chart via Apollo Academy)

AI-related expansion can continue via additional leverage, but with debt servicing costs likely to be higher for longer, it would make sense for the valuations to be questioned. Oh wait, they are:

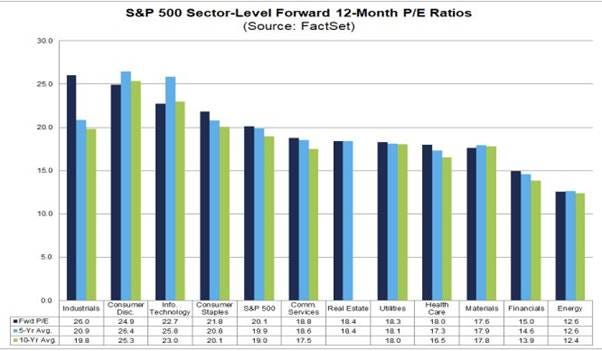

The forward p/e ratio for the US tech sector is below both its 5- and 10-year averages.

(chart via FactSet)

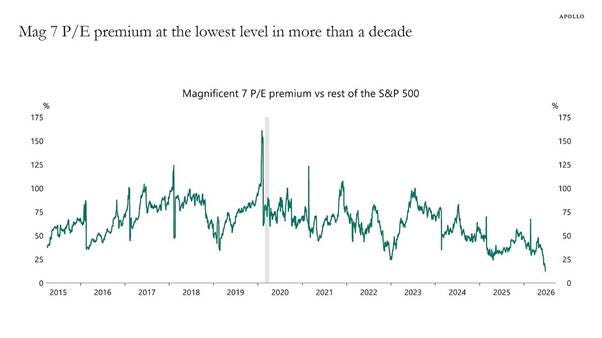

And the premium of the Mag 7 stocks’ p/e ratio to that of the rest of the market is at its lowest level in more than a decade.

(chart via Apollo Academy)

True, the hyperscalers are not semiconductor manufacturers, which have been on a tear – but they are semiconductor purchasers. Can the semiconductor market leaders met the priced-in expectations of demand? What are the odds that demand is over-estimated? Apple is asking the US government for clearance to buy chips from China to ease price pressures.

In sum, market and survey sentiment indicators are flashing that the colossal productivity gains pundits are promising may disappoint.

This comes at a time the US government is moving in for control – talking about taking stakes, insisting certain models be gated, limiting export of chips to “friendly” countries.

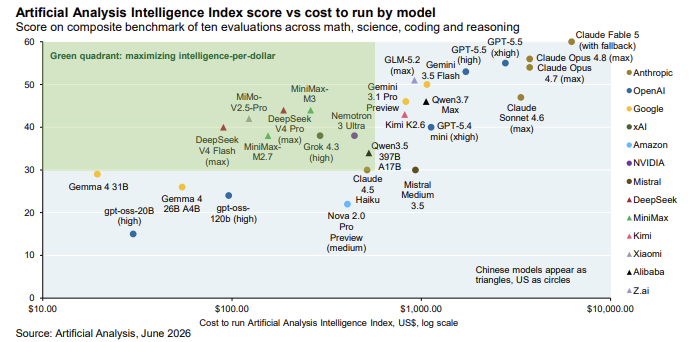

Meanwhile, China is repeating a strategy that has worked for them before – undercut on price, get people hooked on supply and go for scale. Last week, Western media started reporting that Zhipu AI’s new GLM-5.2 model is competitive with leading US models at roughly a fifth of the cost – and it is open-source. The US may have the most powerful models, but it does not win on “intelligence per dollar”.

(chart by JPMorgan)

Tie this in to the sweeping geopolitical initiatives from both the US with Pax Silica and China with its Global Governance Initiative, and you can see the tectonic plates realigning.

The US is saying “don’t trade with China and we’ll let you buy our cool hardware”.

China is saying “we respect your tech sovereignty, feel free to use our AI models, and we’ll sell you the supporting infrastructure at a lower price”.

True, these simplifications gloss over complex trade and financing strategies of the two superpowers as well as patchy track records on the diplomacy and human rights fronts from both.

But it’s not hard to see which superpower is winning the messaging war.

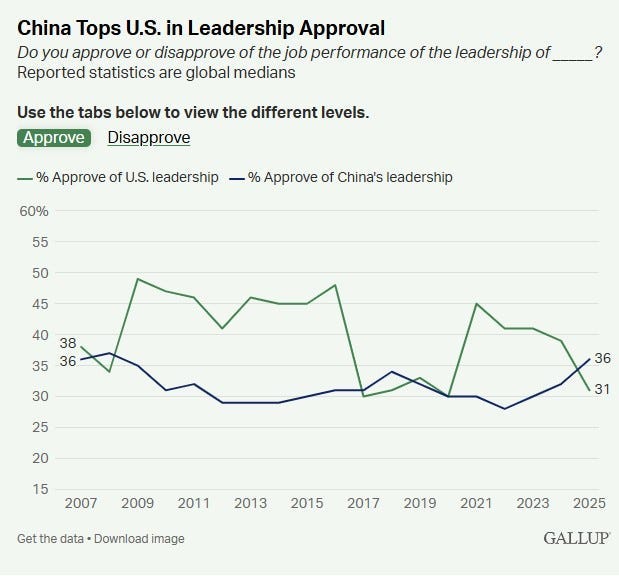

A recent survey by Gallup showed that global approval ratings of Chinese leadership were higher than that for US leadership.

(chart by Gallup)

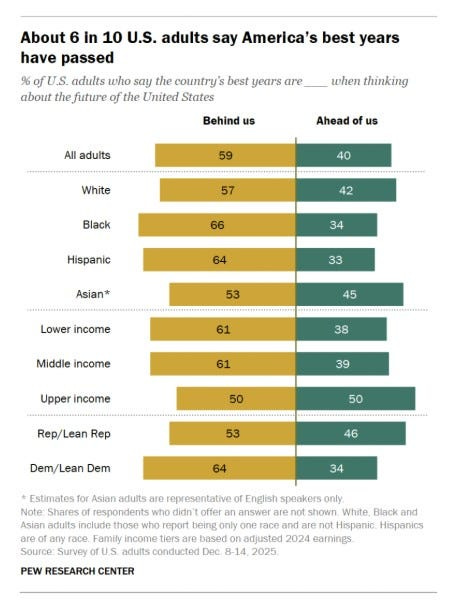

And Americans are feeling bleak about their country’s outlook, with a Pew Research survey published last month showing that almost 60% think the best years are behind them.

(chart by Pew Research)

In sum, we’re told by economists and politicians and markets that there is a lot riding on the US dominating AI – but global competition is advancing, voters are recoiling and this could show up in the voting booth and also in a market reset.

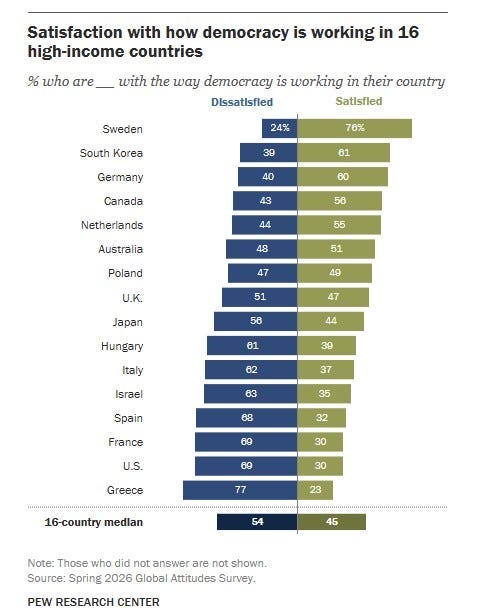

Meanwhile, another Pew Research survey published earlier this month shows that almost 70% of Americans are not happy with how democracy is working in their country, putting the US near the bottom of the list of high-income countries.

(chart by Pew Research)

I don’t want to sound like Chicken Little warning that the sky is falling in – I don’t think it is. And I’m as sceptical of surveys as anyone (I have a degree in Applied Mathematics, so I have reason to be). But the sheer volume of heavy hints that the “standard” narratives are complacent is getting too hard to ignore.

Focusing only on short-term market moves and US tech progress blinds us to the bigger shifts affecting people and their decisions. History tells us that overlooking mood changes does not end well.

History also tells us that power does whatever it needs to in order to hold on – we’re already seeing an erosion of liberties we once took for granted, such as freedom of speech and public information access. The recent mandate that all UK social media users have to identify themselves to prove they’re over 16 is chilling, especially given the prevailing assumption that speech critical of the “social consensus” is harmful. Politico reported last week that the Council of the EU plans to invite social media influencers to cover leaders’ summits in Brussels and certain ministerial meetings, but only if they “share EU values”. The list of similar examples is tragically long.

Meanwhile, clinging to power is expensive, which means fiscal spending will continue to erode trust in government-issued “safe assets”. Social realignment is rarely peaceful. And political unrest is almost always met with more repression, so we can expect more censorship, increasingly exercised via financial access.

All this brings me to an egregiously overlooked Bitcoin narrative: insurance.

Of course, we all hate insurance assets because they represent bad times.

And, yes, BTC is largely seen as a speculative asset whose price is likely to remain muted for a while given the tightening global liquidity regime.

Plus, the “institutionalization” of crypto does dull the “alternative”, off-system patina that Bitcoin enjoyed in its early days.

But nothing changes that Bitcoin and gold are the only assets traded on liquid markets that serve as hedges against a world struggling to find its footing on rapidly shifting plates.

That is not to say the asset is a strong buy just yet – given the global tightening phase we have to get through first, we have time.

My bigger point is that most of the prevailing narratives we are fed – US tech dominance, the resilience of democratic forces and financial access, the speculative nature of unbacked assets – are comforting yet also misleading.

Marshall McLuhan had a great phrase for this:

“We look at the present through a rear-view mirror. We march backwards into the future.”

Regular readers will have read my rants about complacency risk, and will know that one of the reasons I write this newsletter is to explore how crypto technology fits into the changes afoot and ahead. I do believe it is an important tool, and that conviction fuels my longer-term optimism.

Us humans have repeatedly shown we can adapt. Sometimes we thrive. In the interim, we end up questioning assumptions and ideologies, incorporating the new landscape and the new tools into our personal and community maps. Even more important, enough of us are steeped in the liberal tradition to successfully, eventually, push for the type of opportunity we think society should have.

See also:

Geopolitics: an axis shift and the impact on crypto (Oct 2025)

Pax Silica widens the wedge (June 2026)

HAVE A GREAT WEEKEND!

(in this section, I share stuff that has NOTHING to do with macro or crypto, ‘cos it’s the weekend and life is interesting)

Amazing. Just amazing. If you’ve been paying any attention at all to football, by now Cape Verde has no doubt captured your heart.

In its first World Cup, it drew with Spain, drew with Uruguay, and last night played a tight and tough game against Argentina, scoring what many commentators (including my husband) are calling the “goal of the tournament”. This under-exposed team from a country with a population of roughly 530,000 showed the world what courage and grit and skill can do. And they leave us with a solid bank of inspiration and marvel that will make every match going forward even more magical, while not quite reaching the thrill of this one.

The best way we can show our respect for what the team achieved is by learning a bit more about a country most had not even heard of before the tournament began.

DISCLAIMER: I never give trading ideas, and NOTHING I say is investment advice! I hold some BTC, ETH and a tiny amount of some smaller tokens, but they’re all long-term holdings – I don’t trade. Also, I often use AI for research instead of Google, but never for writing.